USD: Dollar derailed: shutdown stalls momentum

Not a great start for the US dollar this month. The government shutdown is set to delay the release of the NFP report, disrupting the upbeat momentum sparked by the upward revision to GDP the other week, and capping further dollar upside for now.

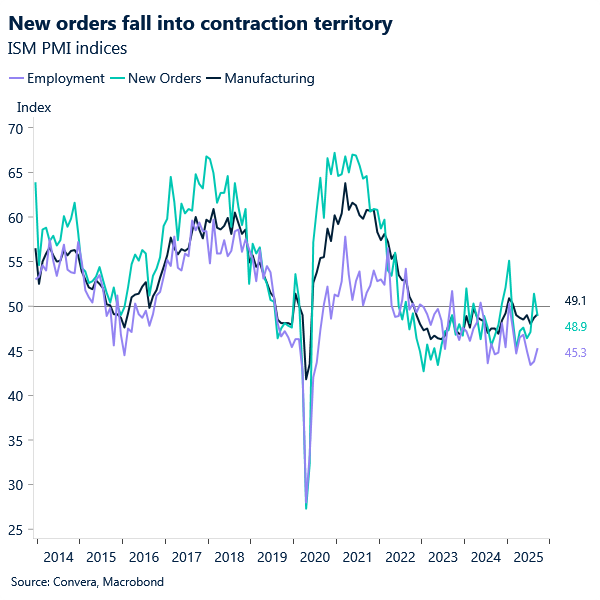

Private-sector payrolls declined by 32,000 in September (ADP report), due at least in part to issues with data analysis. US factory activity also contracted for the seventh consecutive month, with the orders component slipping from 51.4 to 48.9. Overall, the manufacturing index edged up 0.4 points to 49.1 from 48.7, but remains in contraction territory.

The dollar dipped following the release, though not as sharply as expected, given the heavier weight these second-tier indicators carry when top-tier data (like NFP) is unlikely to be published this Friday.

In the absence of key data, we expect the dollar’s price action to remain subdued – weighed down by an uncertain economic outlook and lingering shutdown-related risks – until upcoming macroeconomic releases provide fresh impetus.

EUR: Breakout on hold, patience on trial

Eurozone inflation came in right on target, wrapping up the latest batch of member-state prints and reinforcing an overall benign price pressure environment. The results were particularly telling, especially after ECB President Christine Lagarde had just pointed to room for further rate cuts in the euro area, stressing that policymakers’ stance is not “fixed.”

While EUR/USD remains supported amid uncertainty surrounding the U.S. government shutdown, the impasse is simultaneously depriving the euro of more durable upside drivers – chiefly, clarity on the U.S. macro backdrop, with the labour market in particular under scrutiny.

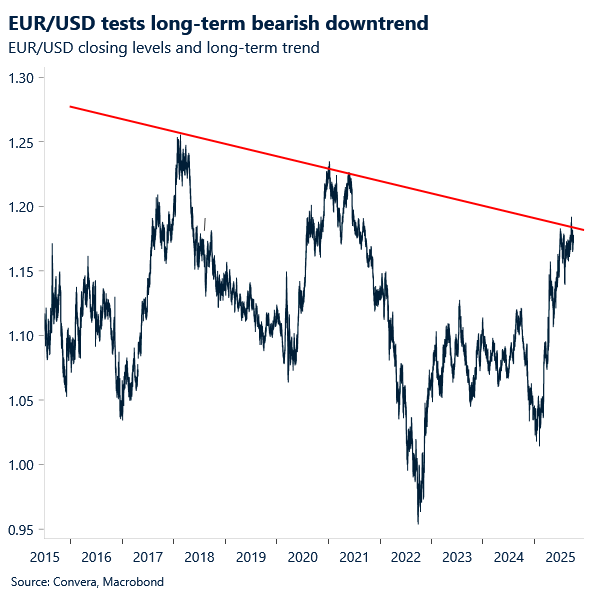

The euro urgently needs fresh catalysts – soft U.S. data and a dovish Fed – but the slowdown is instead prolonging the wait for a breakout above $1.18. Over the longer term, EUR/USD has repeatedly rejected a descending trendline. The stalled momentum seen over recent months may coincide with this periodic failure, and it would take better-than-expected macro releases to shift the signal toward a more meaningful bearish pullback.

GBP: Receding political risk supports sterling

Sterling opened the final quarter as one of the strongest performers in G10 FX, buoyed by market relief following the Labour Party’s annual conference. Concerns that the event might signal a shift toward aggressive fiscal expansion proved unfounded, removing a key political risk from the near-term outlook.

With month-end positioning flows now behind us, attention has turned to broader market dynamics. The FTSE 100 continues to outperform global benchmarks, supported by the widening global equity rally and record-high valuations.

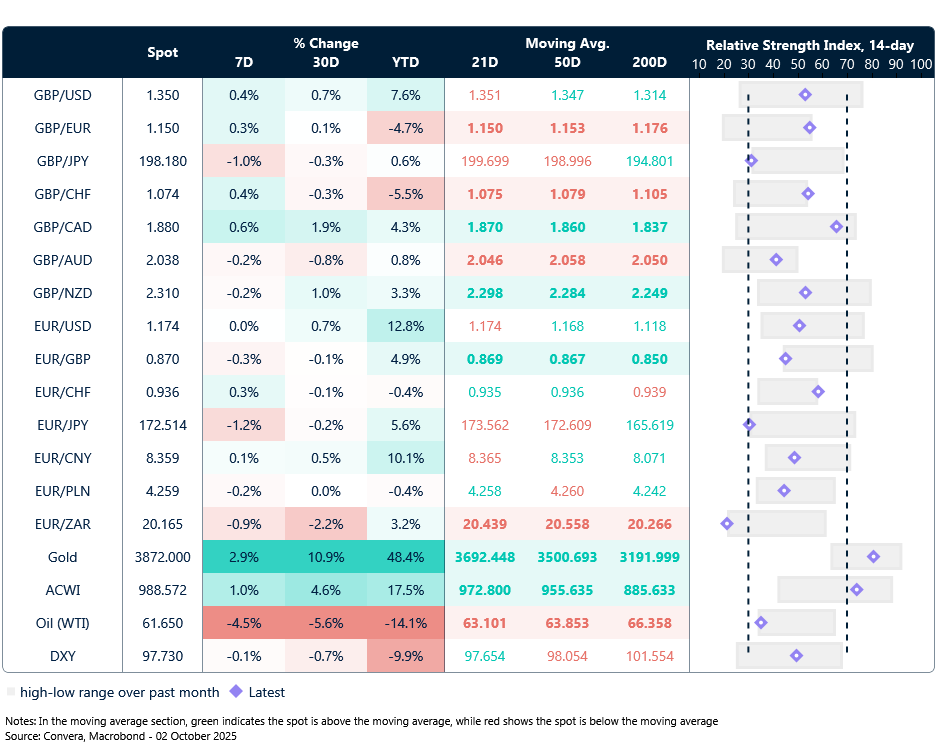

GBP/EUR briefly touched €1.15 before retracing to €1.1480 by Thursday morning. This marks a departure from the recent period of low volatility in the pair, with the latest moves favouring euro strength. GBP/USD followed a similar trajectory, rising to $1.3527 before slipping back to $1.3475. Comparable intraday reversals were observed across other major crosses, suggesting a broader pattern of fading strength.

While sterling closed the session higher, the inability to hold intraday highs points to limited follow-through. That said, technical conditions have improved meaningfully since the start of the week, and a more stable base now appears to be forming – potentially setting the stage for further recovery in the near term. That said, a cluster of moving averages are likely to act as resistance barriers for GBP/EUR, with the 21-day SMA at €1.15 the first hurdle to overcome.

GBP/EUR jumps out of oversold territory

Table: Currency trends, trading ranges and technical indicators

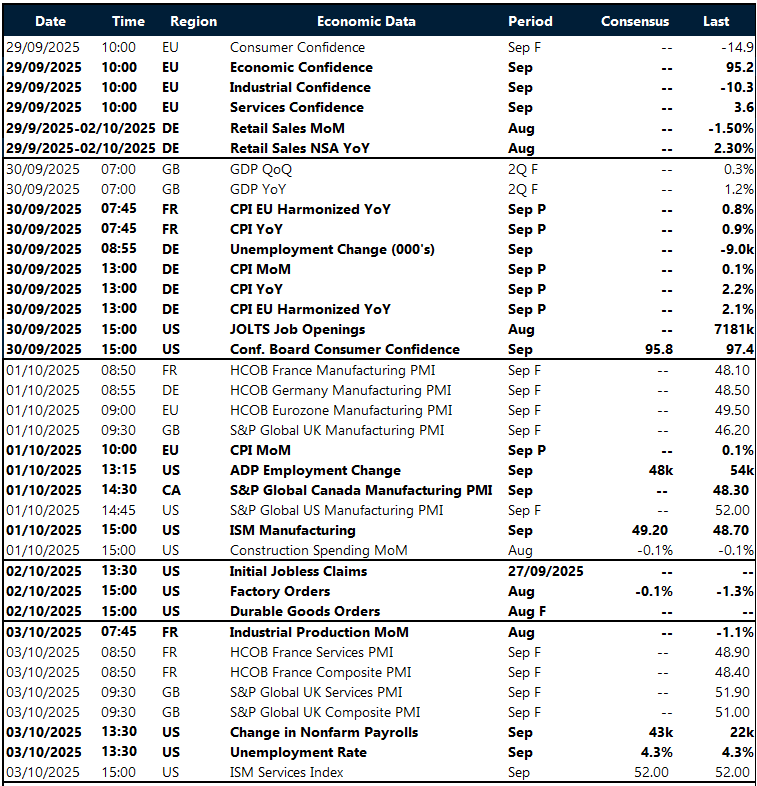

Key global risk events

Calendar: September 29- October 3

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.