More proof needed, central banks in focus

Risk-on momentum following the US–Iran peace deal announcement appears to have steadied in today’s session, as markets refocus on a busy run of central bank meetings this week, with the RBA and BoJ in focus. Some caution remains, however, with investors keen to dissect the finer details of the memorandum. The two sides are preparing to formalise an interim agreement this Friday in Switzerland.

Elsewhere, the BoJ hiked rates by 25 bps to 1% while the RBA left policy unchanged at 4.35%. The BoJ’s intention to move toward rate normalisation is well understood by markets, and the yen has shown little reaction to the widely anticipated move, holding steady near 160.2. The BoJ also indicated that from April 2027 it will stop reducing its monthly purchases of Japanese government bonds, stabilising purchases at around ¥2 trillion per month. This guidance is instructive, as it underscores a tightening bias that extends beyond rate normalisation to include balance sheet adjustment. Attention now turns to the BoJ press conference, where markets will look for signals on the pace and extent of further tightening, particularly against the backdrop of an economic slowdown linked to the fallout from the Iran conflict.

Turning to geopolitics, uncertainty around the US–Iran peace deal persists. Key questions centre on the agreement’s detail, the pace at which oil flows could normalise after Friday’s signing, and Israel’s stance given its opposition and record of disrupting diplomatic progress through its parallel conflict with Hezbollah in Lebanon. For the softer tone in the dollar to extend, Friday will be pivotal. The memorandum’s details are expected to be released after signing, alongside steps to lift mutual blockades.

Looking ahead, sustained risk appetite will depend less on the immediate resumption of shipping volumes and more on whether this sequence of de-escalation measures unfolds smoothly. If the process progresses as expected and the US and Iran commit to renewed nuclear talks shortly after Friday, the market is likely to gradually fade the conflict narrative. There are already signs that investors are becoming more indifferent to incremental peace developments. Last week’s muted reaction in both oil and the dollar, despite renewed violence, helps illustrate this shift.

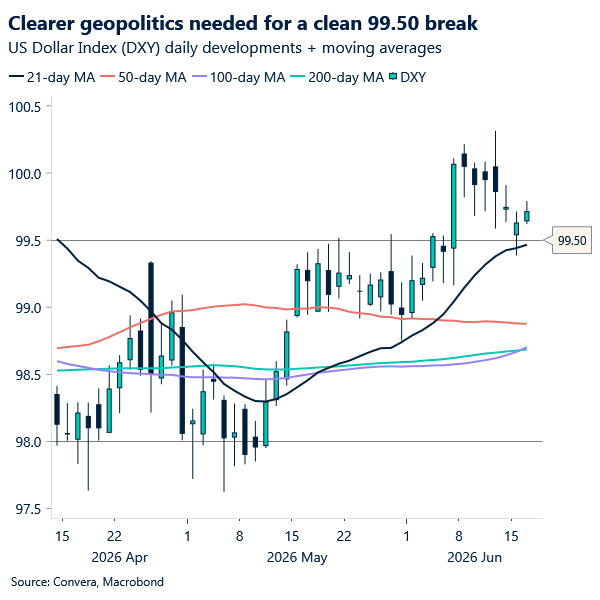

The dollar index held just above the 99.50 level yesterday, which coincides with its 21-day moving average. This suggests that dollar sellers remain cautious about peace prospects, and may require further confirmation before adopting more conviction in positioning. Once through it, the next support level in line becomes 99.250.

EUR: Oil in the driver’s seat for ECB outlook

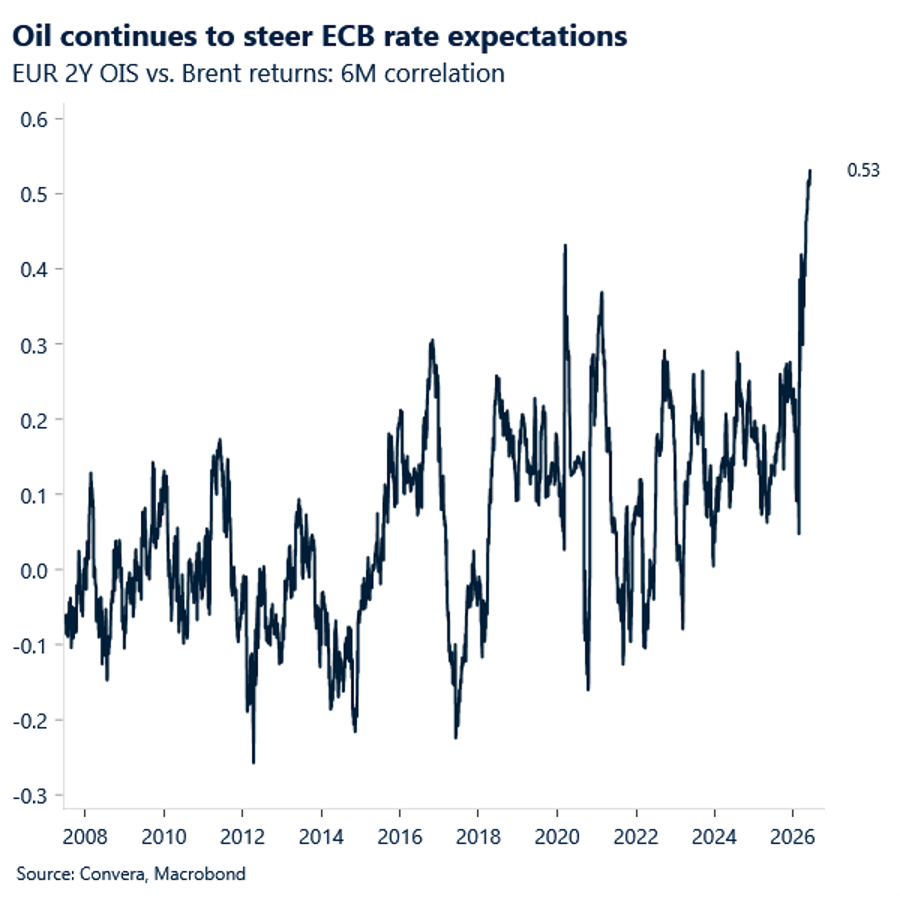

Hawkish messaging from last week’s ECB meeting continues to reverberate, with President Lagarde reiterating yesterday that higher energy prices are increasingly feeding into broader inflation dynamics. While she acknowledged de-escalation around Hormuz, developments remain far too premature to justify stepping away from a hawkish policy stance.

Energy prices continue to anchor shifts in rate expectations. Despite Lagarde’s firm tone, September pricing has softened notably. As recently as last Thursday, markets were weighing the possibility of two hikes; that has now eased to around an 80% probability of a single move, following Sunday’s peace deal announcement. With the inflation shock still largely supply-driven, any sustained easing in tensions driving oil lower, could trigger a further unwinding of the market’s hawkish bias – especially around the September decision.

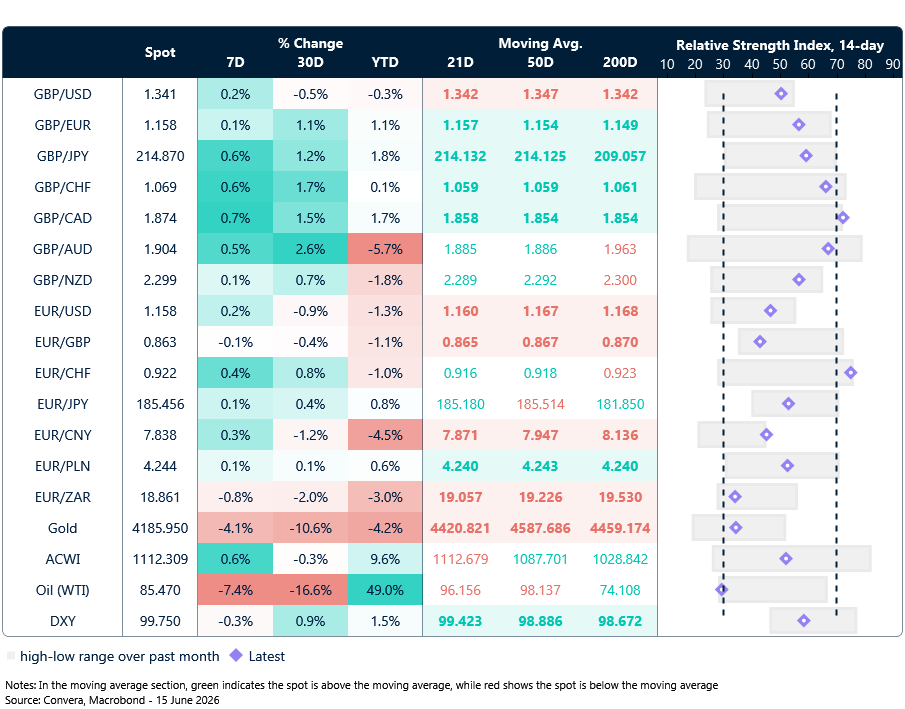

EUR/USD failed to close above its 21-day moving average near 1.16 yesterday, signalling a lack of conviction among euro bulls as uncertainty persists around the durability of any prospective peace agreement. The eurozone calendar is relatively light today. Elsewhere, policy meetings in Australia and Japan may draw more attention.

Market snapshot

Table: Currency trends, trading ranges & technical indicators

Key global risk events

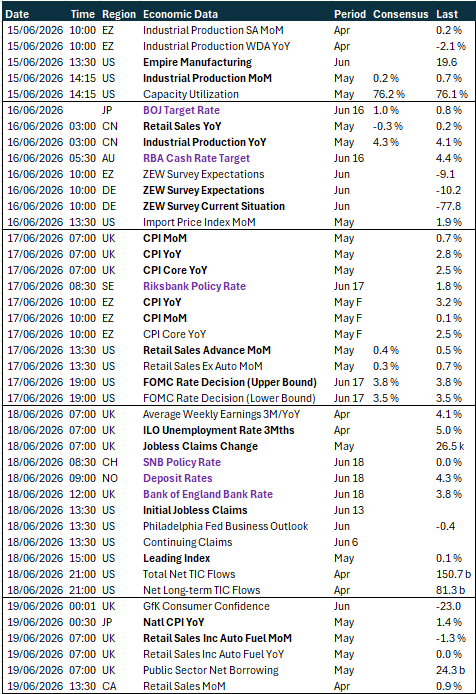

Calendar: June 15-19

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.