Written by Steven Dooley and Shier Lee Lim

BoJ hikes ahead of key Fed decision

A massive week for monetary policy kicked-off with the Bank of Japan finally joining the rest of the developed world’s central banks and lifting rates while the Reserve Bank of Australia headed in the other direction as it pivoted to “neutral.”

The Bank of Japan lifted official interest rates for the first time since February 2007 – a time before the global financial crisis and even the iPhone.

The BoJ raised rates from -0.10% to a range of 0.0% to 0.1% and also ended its yield curve control, quantitative easing and forward guidance programs.

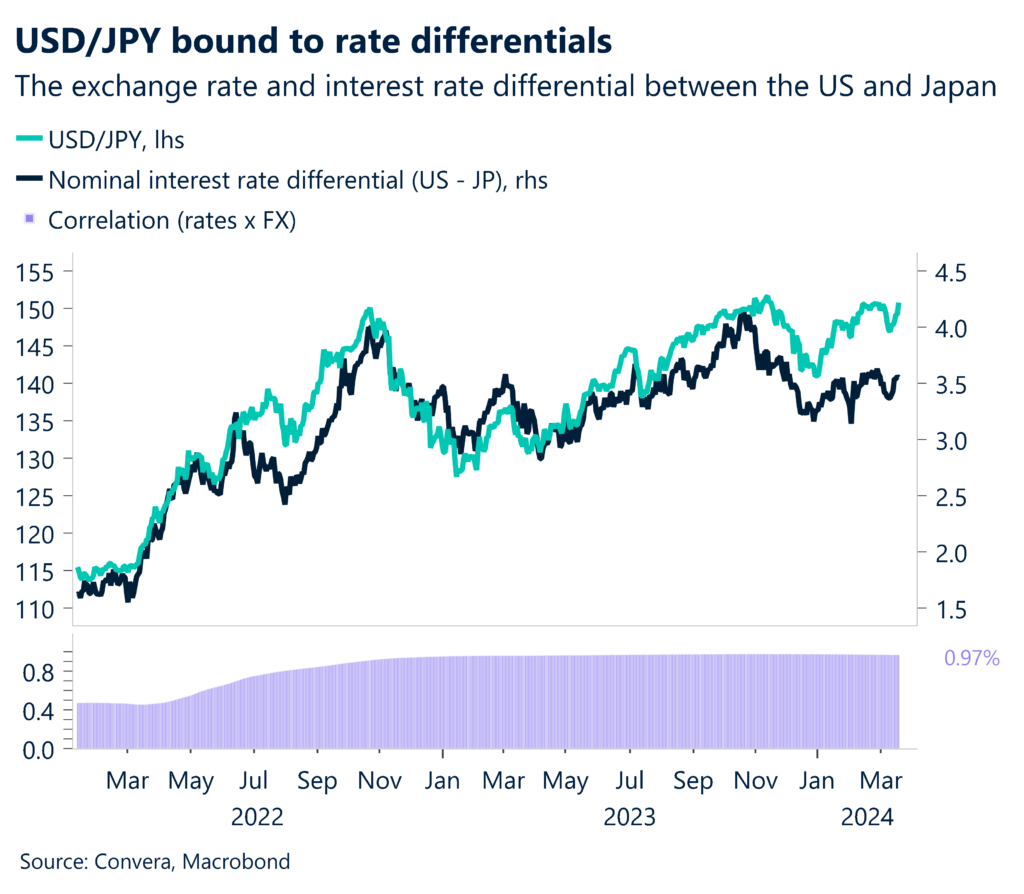

However, with the market largely expecting the move, the USD/JPY bucked any move lower from the yen’s increased rate regime and instead jumped to four-month highs. Additionally, a recent move higher in USD rates has also supported the greenback.

The BoJ move overshadowed a significant move from Reserve Bank of Australia yesterday, which pivoted to neutral, as it said it was unwilling to rule out a move either higher or lower. Previously, the RBA was focused on its next move as likely higher.

Tonight, the focus shifts to the US Federal Reserve. The Fed is expected to take a tougher stand on policy as higher than expected inflation and a stronger jobs market keeps the pressure on the US central bank to keep interest rates elevated.

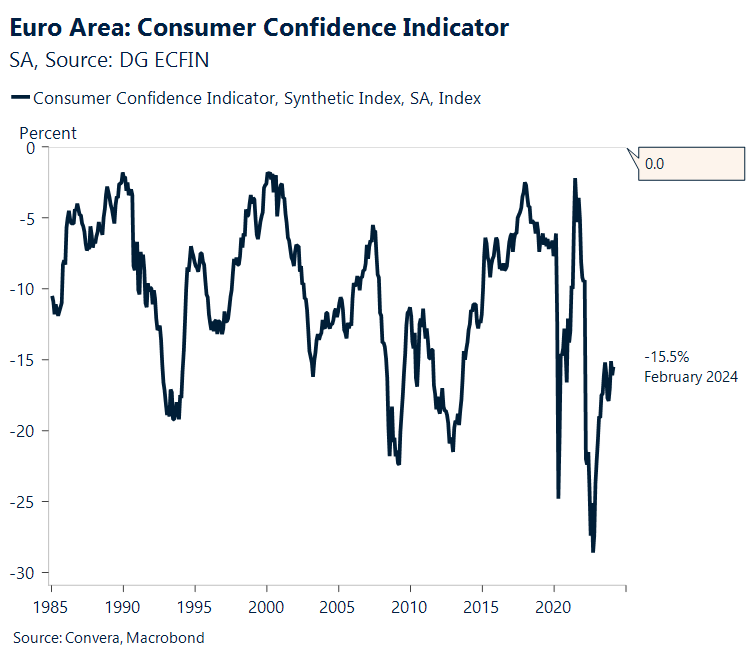

Euro stronger as consumer confidence improves

Otherwise, key data today includes Eurozone consumer confidence, which looks likely to increase from -15.5 to -15.0 as it continues a slow improvement since the lows seen in mid-2022 after the Russian invasion of Ukraine.

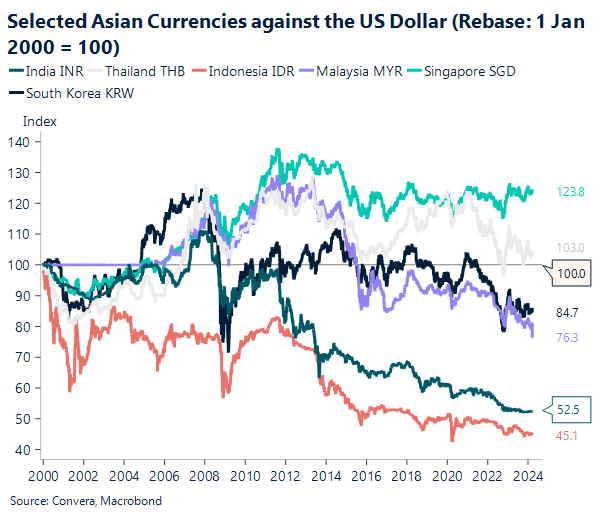

The EUR/USD has staged a mini-comeback over the past month (although it eased over the last few days).

This comeback has seen the euro strengthen versus other key currencies with the single currency at two-month highs versus the Singapore dollar and four-month highs versus the Australian dollar.

Bank of Indonesia decision due

Away from the major central banks, the Bank Indonesia (BI) looks likely to retain its 6% policy rate and the same cautious stance in its announcement, highlighting BI’s continued vigilance in the face of increased external concerns.

Specifically, BI will likely continue to indicate that it will follow the US’s example and is unlikely to begin cutting before the Fed.

Furthermore, the current account deficit was larger in Q4 than anticipated, and we believe that balance of payments pressures will continue because of the expanding current account deficit and probable decline in foreign direct investment inflows as a result of uncertainties surrounding the political change.

In February, headline inflation also jumped to 2.8%, and there have been further recent increases in upside risks, especially in relation to food inflation.

USD/JPY surges after BoJ hike

Table: seven-day rolling currency trends and trading ranges

Key global risk events

Calendar: 18 – 22 March

All times AEDT

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.

Have a question? [email protected]

Take a deep dive into the trends shaping cross-border payments with our podcast, Converge.