Written by George Vessey & Boris Kovacevic

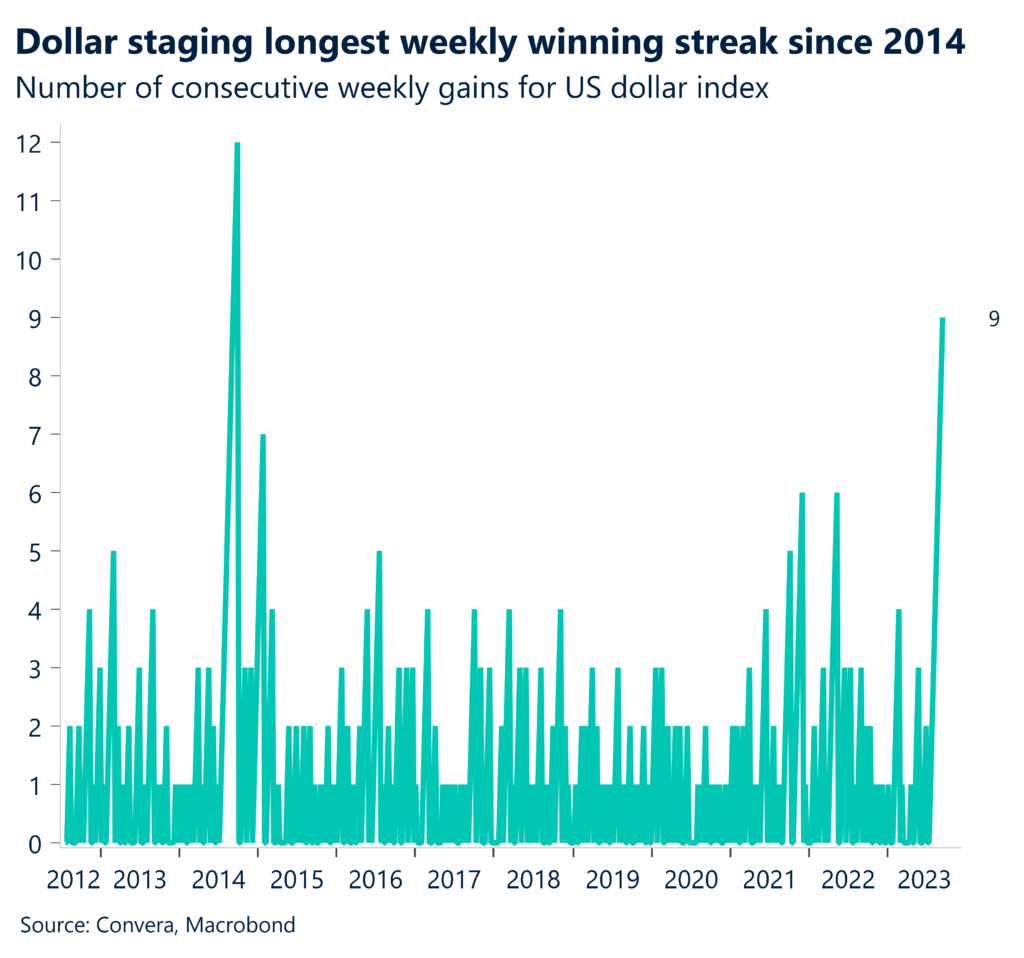

Best run since 2014

The US dollar index is poised to record its 10th back-to-back weekly rise, which would mark its longest weekly winning streak since 2014. Demand for the US currency remains buoyant as US interest rates continue to grind higher, with the 10-year Treasury yield climbing to 4.50% – the highest since 2007.

The US dollar has rebounded around 6% against a basket of major currencies since hitting a 15-month low in July. Although the Federal Reserve (Fed) kept the target range for the fund’s rate at 5.25%-5.5% in September, it signalled another hike may be on the table amid inflationary risks and stronger economic activity. Projections released in the dot-plot showed the likelihood of one more increase this year, then only two cuts in 2024, down from four cuts previously projected. This grind higher in US yields has weighed heavily on riskier assets like equities, which is also supportive news for the dollar, as capital rotation into cash will mostly end up in the liquid dollar that pays 5.30% overnight rates. Moreover, with US yields firm and US rate volatility sinking again, the dollar could build on gains against the low-yielding Japanese yen more than other currency peers, especially given the dovish Bank of Japan in the early hours of today.

We’ll have to see softer US economic data if we’re to witness the dollar’s strength subside, but for now US resilience dominates. Yesterday’s release of the lowest weekly jobless claims since January, suggests the robust US labour market is still a far cry from cooling. If we see another string of weak European purchasing manager indices (PMIs) today, the dollar could build on recent gains and stay strong through October.

BoE pause bashes pound

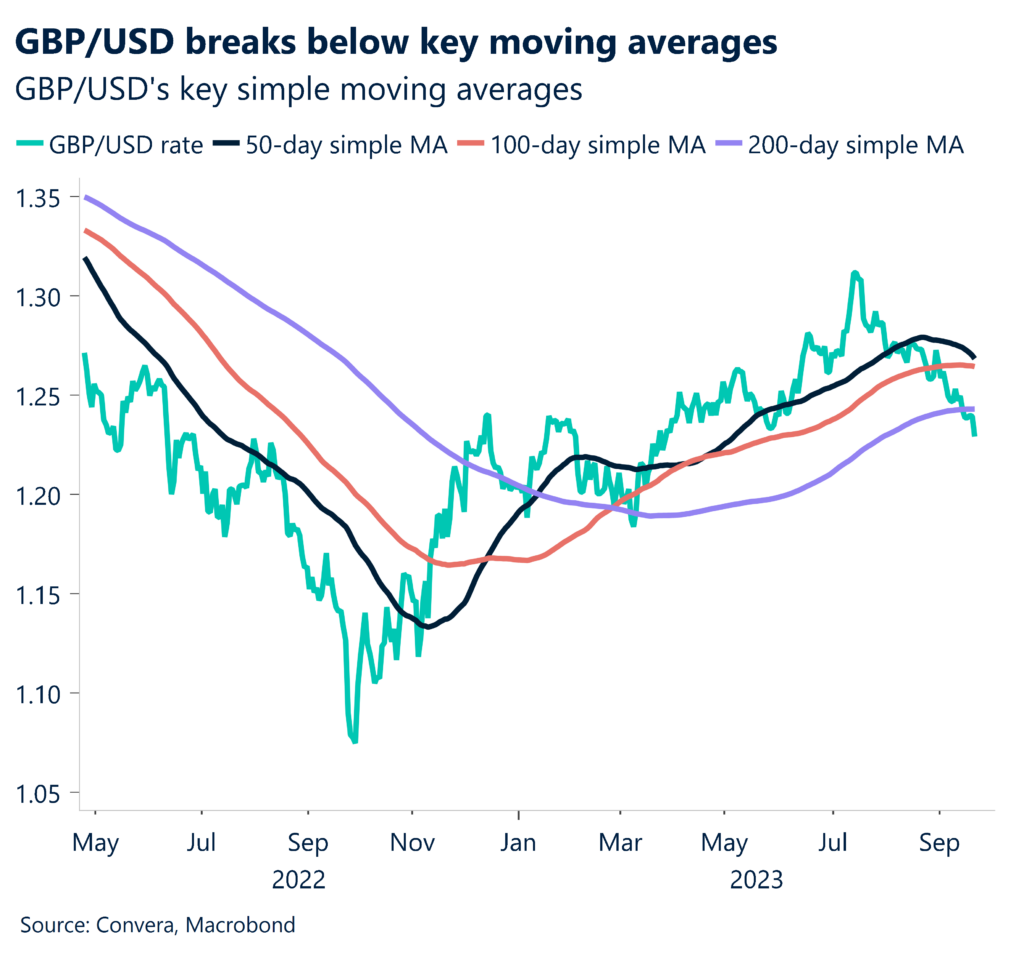

The British pound tumbled to a fresh 6-month low against the US dollar, just shy of $1.22, as the Bank of England (BoE) surprised by choosing to keep interest rates unchanged. Money markets were pricing an 80% chance of a hike at the start of the week, which changed to a 50-50 chance after the softer UK inflation report on Wednesday.

After 14 consecutive hikes, dating back to December 2021 and encompassing 515 basis points of tightening, the BoE decided not to hike at this September meeting. Following better than expected inflation data in August and citing increasing signs of the economy slowing, the bank’s Monetary Policy Committee (MPC) split five to four in favour of leaving rates unchanged at 5.25%. Different interpretations over the incoming economic data, particularly suspicions about the labour earnings numbers swayed the decision. But the BoE kept the door open to further hikes in the future reflecting the upside risks it perceives relative to its inflation outlook. This allowed the pound to recoup some losses after an initial knee-jerk reaction lower, but GBP/JPY suffered the most, ending yesterday 1% lower.

This morning, UK retail sales came in below expectations, rising 0.4% m/m versus 0.5% forecast. Should flash PMIs disappoint later this morning, sterling could re-test fresh 6-month lows nearer $1.22 against the dollar and GBP/EUR might slip under €1.15.

ECB hitting the euro with dovish talk

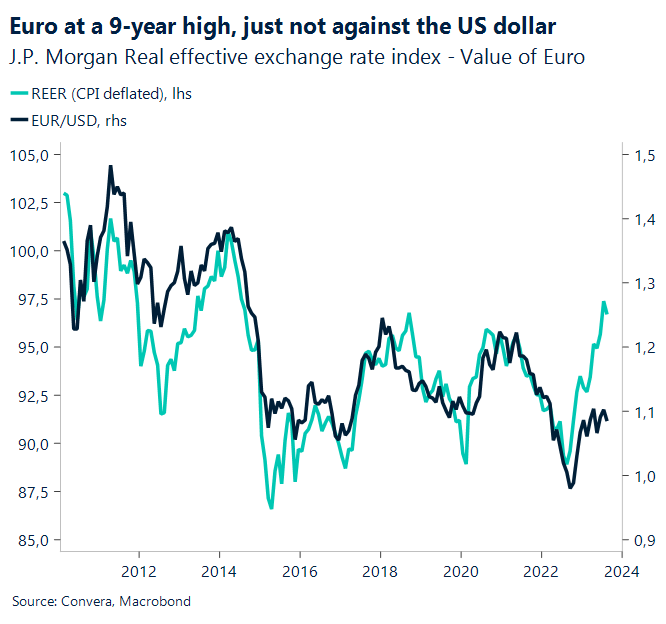

Higher bond yields across the world, dovish ECB speak, and weak economic data have introduced an unfriendly environment for risk sensitive assets like the euro. While the world reacted to the news of the US 10-year government bond yield hitting the 4.5% mark, European currencies tumbled on expectations that most of the continents central banks would be done raising interest rates.

The euro, Swiss franc, and British pound, of which the latter two have been hit by the unexpected rate pauses by their respective central banks, have all fallen against the dollar in recent weeks. EUR/USD has depreciated more than the trade-weighted euro, given that most of the Eurozone’s trading partners (Sweden, Norway, Japan, China) face the same consequences of lower global growth. The currency pair is struggling to free itself from the now 9-week long downtrend. The PMIs released later today for the Eurozone, UK and US will decide if the euro successfully records its first appreciation in ten weeks or if the burden of higher yields becomes too much for the euro to handle.

On the macro side, the European Consumer Confidence Index once again surprised the consensus to the downside, showing that a short-term rebound cannot be automatically equated to a sustained rebound. The recent economic weakness explains why policymakers have been more vocal about ending the tightening cycle with the number of members talking about potential cuts in 2024 rising. Just yesterday, Governing Council member Stournaras expressed his view that the next rate move will most likely be a cut, even though he did not mention a time frame for such a move. However, the current projection from the ECB sees inflation only returning to the 2% level at the end of 2025. We tend to disagree and see the potential for a short-term dovish repricing as inflation cools and the economy stagnates at lower levels.

Equities tumbles as bond yields surge

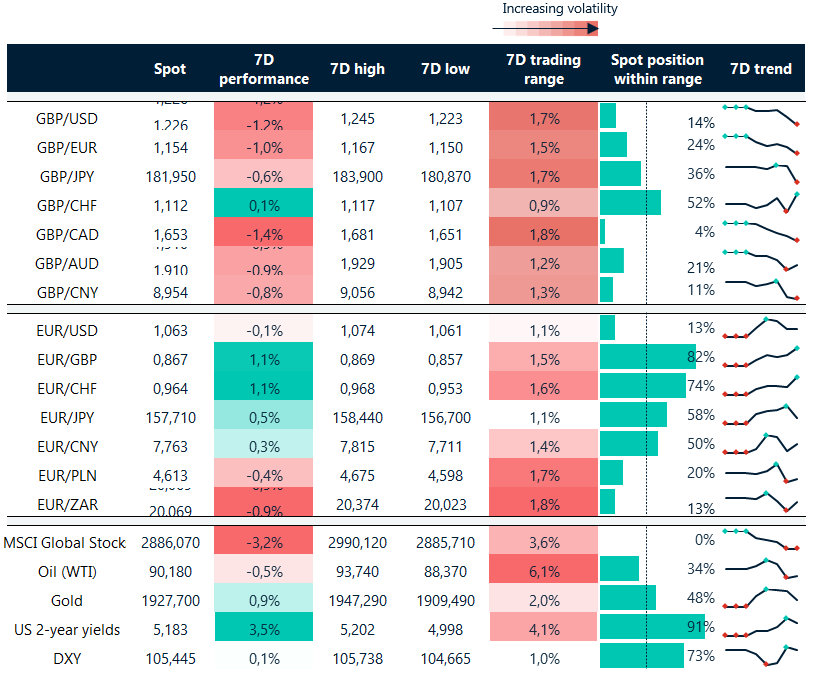

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: September 18-22

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.