Dollar struggles after soft US data

Global equities rose for a fourth straight day and the US dollar index fell to a one week yesterday, weighed down by softer-than-expected US economic data, which bolstered bets that the Federal Reserve (Fed) will refrain from raising interest rates further. The yield on the 10-year US Treasury note sank to its lowest in three weeks, extending its decline from its recent 15-year high.

The US data dump included downward revisions of second quarter GDP growth and core PCE prices. However, the 2.1% GDP growth is still extremely healthy for the world’s biggest economy that continues to prove resilient in the face of higher borrowing costs. Labour market strength has been a key reason the economy has grown faster than expected in 2023, but questions about its robustness are surfacing. Ahead of non-farm payrolls on Friday, we’ve seen weak second-tier jobs data such as job openings as well yesterday’s ADP figures, which revealed job creation slowed more than expected in August. This comes on the heels of data showing that consumer sentiment in the US fell by the most in two years in August, amid higher borrowing costs and persistent inflation.

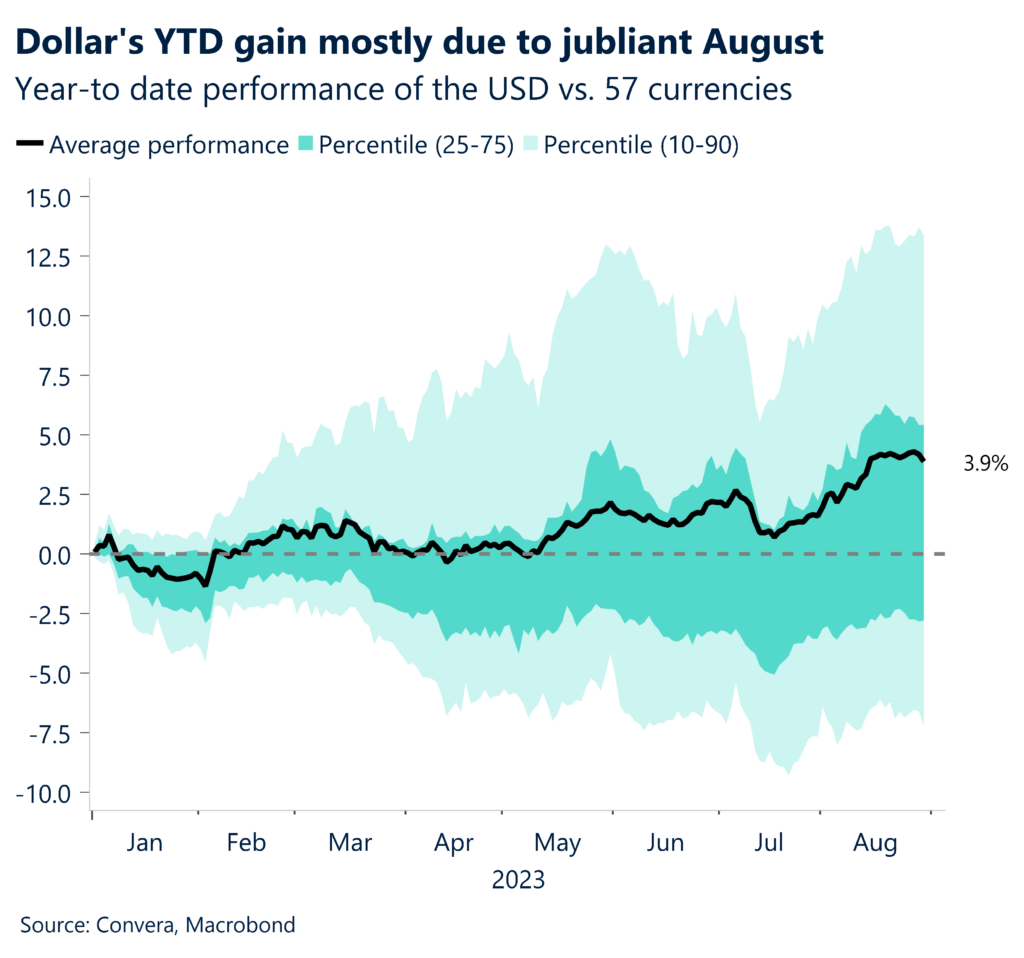

Falling job vacancies suggest demand for labour is falling, which in turn suggests the upward pressure on wages might continue to fade. For the Fed, this eases the pressure to hike rates further, hence the fall in US yields and the dollar. However, the US currency is still on track to secure its biggest monthly gain in three and is, on average, almost 4% up against a basket of 57 currencies globally.

Pound erases last week’s losses

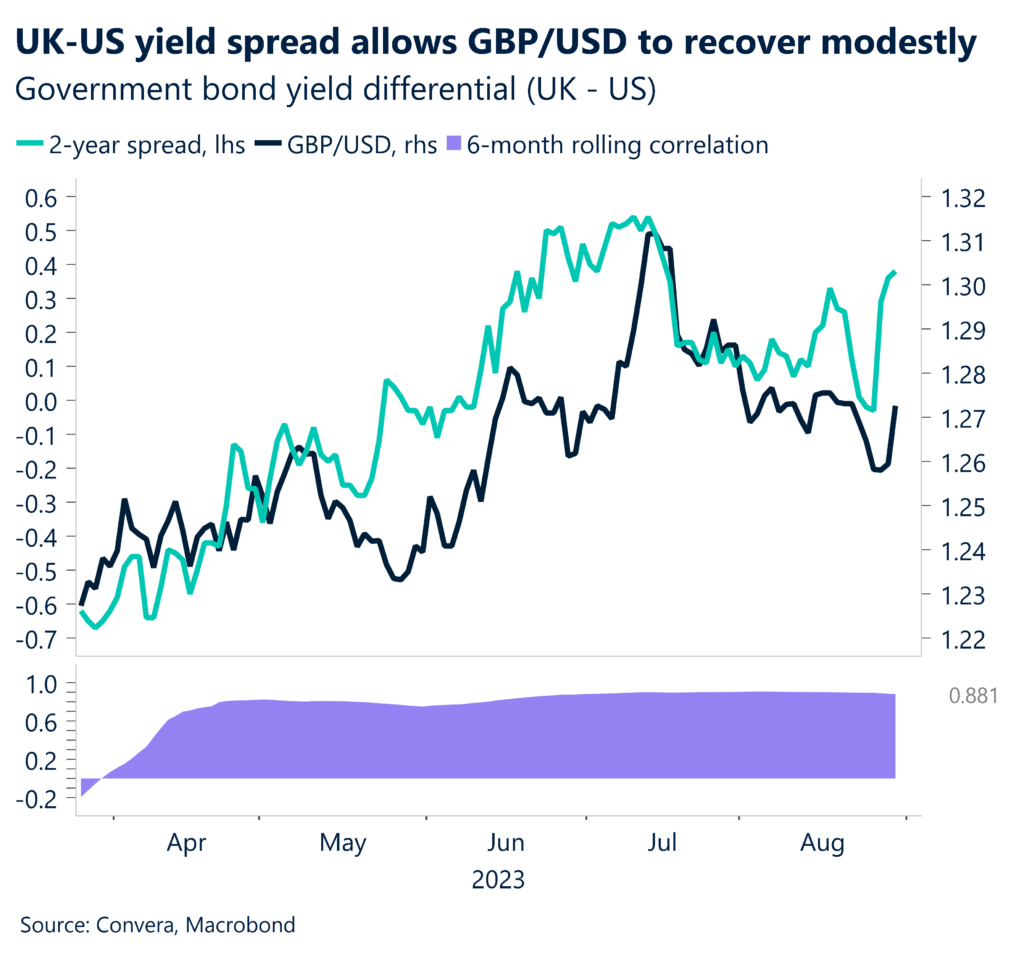

Despite a string of underwhelming domestic UK data, the pound climbed across the board yesterday, boosted mainly by improved global risk appetite and falling US Treasury yields. GBP/USD has reclaimed $1.27, erasing last week’s losses, but backpedalled from its 10-week moving average, which it’s been trapped below for four weeks now.

The pound has shrugged off some concerning housing market updates that showed UK mortgage approvals fell almost 10% in July as higher interest rates made it harder for Britons to afford a home. The figures followed forecasts from property website Zoopla that UK home sales are on track to plunge more than 20% this year to their lowest level since 2012. In addition, the pace of growth in UK consumer credit over the 12 months to July slowed to 7.3%, the smallest increase since December last year in a possible sign of caution among households as borrowing costs rise. The Bank of England (BoE) is expected to hike twice more by year-end, and with US Treasury yields slumping, the UK-US 2-year yield differential has jumped to its highest in over a month, supporting GBP/USD’s recent recovery. However, market pricing for UK interest rates is arguably far too aggressive on the hawkish front. In turn, this leaves sterling vulnerable to a dovish repricing should data weaken.

BoE Chief Economist Huw Pill will be speaking today and is likely to echo the hawkish comments made at by peers at Jackson Hole last week. But with UK stagflation risks on the rise, the pound may find it difficult to climb towards $1.30 in the medium term.

ECB hike back on the table

The euro has enjoyed a short-term recovery over recent trading sessions with weak US jobs data still being processed by markets. Meanwhile. stickier-than-expected inflation prints in Europe have pushed up the expectations of another rate hike by the European Central Bank (ECB) in September, helping further close the rate differential gap, lifting EUR/USD above $1.09.

First inflation numbers for August out of Europe have painted a complicated picture for the ECB. While consumer prices continue to come down, the pace of the disinflation has markedly slowed down. German inflation fell from 6.2% in July to 6.1% in August, beating expectations of a 6.0% print. Core inflation remained at 5.5%. Investors now turn to Eurozone CPI, which despite the upside bets in Germany and Spain, could turn lower. However, this will probably not be enough to take a rate hike in September off the table. Markets are currently pricing in a 50/50 chance of policymakers tightening again next month.

The euro has been helped by a slightly better than expected Chinese manufacturing PMI, highlighting the possibility of an economic bottoming of the second largest economy in the world. This would be good news for the pro-cyclical common currency, which has so far not been able to move beyond the $1.10 mark sustainably.

Euro bolstered by ECB rate expectations

Table: 7-day currency trends and trading ranges

Key global risk events

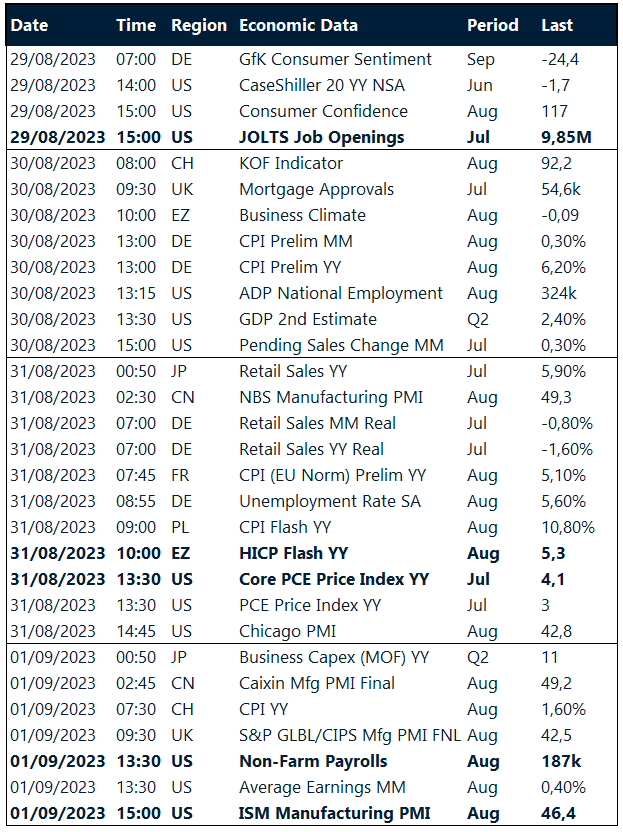

Calendar: August 28-Septemeber 01

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.