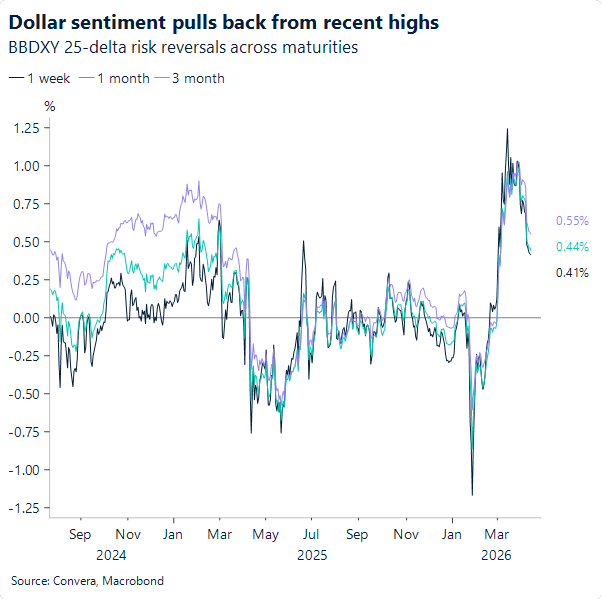

USD: Blockade without fire keeps markets steady

The US dollar was jolted yesterday as risk sentiment shifted. Early trading saw the dollar gain as sentiment deteriorated on concerns around a US naval blockade. However, as the day progressed, markets began to interpret the naval action as a negotiating tactic, with both sides expected to discuss another round of talks before the ceasefire ends next week.

Despite the still-high degree of uncertainty, military re-escalation is now viewed as a last-resort option, while the diplomatic route – though masked by a militaristic façade – appears to remain intact. There is, in fact, a growing sense of cautious optimism that the worst may be over, weighing on the dollar’s bullish case. The DXY pared its gains through the session, ultimately closing 0.7% lower. Oil dipped below $100 a barrel, while equities rebounded.

The DXY also broke decisively below the 99 level, which it had hovered around indecisively since the ceasefire was announced. The increasingly confident de-escalation trade has gained traction, helping to justify the move lower, with the index now below its 200-day moving average near 98.500. This long-term momentum gauge had not been breached to the downside since the conflict began, and spot’s recent position relative to it suggests that dollar bulls may be losing conviction in the greenback’s upside narrative.

Away from geopolitics, today brings the PPI Final Demand release, expected to show a sizeable 1.1% m/m jump, echoing last week’s meaningful rise in consumer inflation. Q1 corporate earnings also begin to trickle in, with the big banks in focus this week. Expectations are for solid momentum, which may be quietly helping buffer sentiment against conflict‑driven anxiety.

On more concrete signs that both sides are willing to negotiate, the 98 level becomes a clear downside target.

EUR: The euro’s quiet comeback

EUR/USD pared back early‑day losses tied to news that US–Iran talks failed over the weekend. Risk‑off sentiment has so far stopped short of deteriorating further as markets continue to lean toward the de-escalation bias.

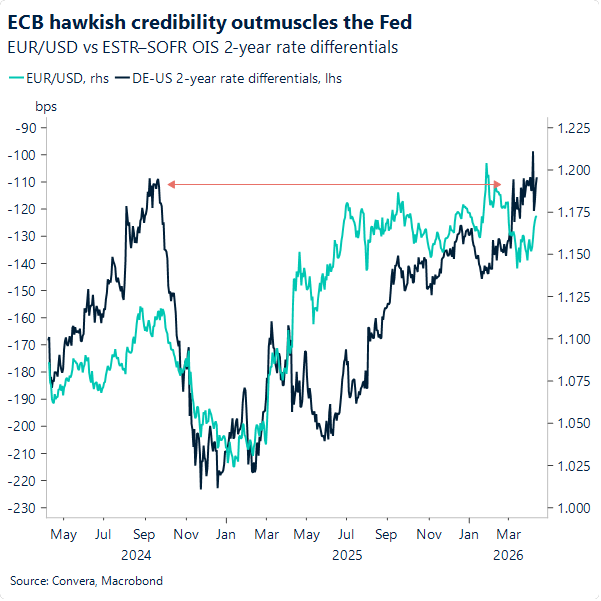

The pair rose 0.6% yesterday, exploring the 1.17 area more confidently away from the 200‑day moving average near 1.1670. We see this long‑term gauge – and spot’s posture relative to it – as instructive: spot fell aggressively below it when the conflict began and has only recently managed to stabilise above it. We interpret this as euro buyers showing their strongest conviction in the currency’s trajectory since the conflict started, pointing to a tendency to keep a long‑term bullish bias intact for now.

On a path of gradual de‑escalation, the euro is set to encounter a more distinctly hawkish ECB, with markets pricing a ~36% chance of a hike as early as this month. While highly unlikely, this pricing tendency reflects a market perception that the ECB is far readier than the Fed to tighten further. EUR–USD 2‑year OIS differentials are now the narrowest since late 2024, and although further de‑escalation would unwind part of that move, the ECB’s “tough talk” is more likely to stick than the Fed’s.

This would give EUR/USD a more robust fundamental anchor, setting the stage for a swifter move higher as sentiment improves – with scope to challenge early‑2026 highs. But for now, should de-escalation momentum gain traction, we see late-February highs near 1.1830 as an appropriate target in sight.

GBP: Jumps back to pre-war highs

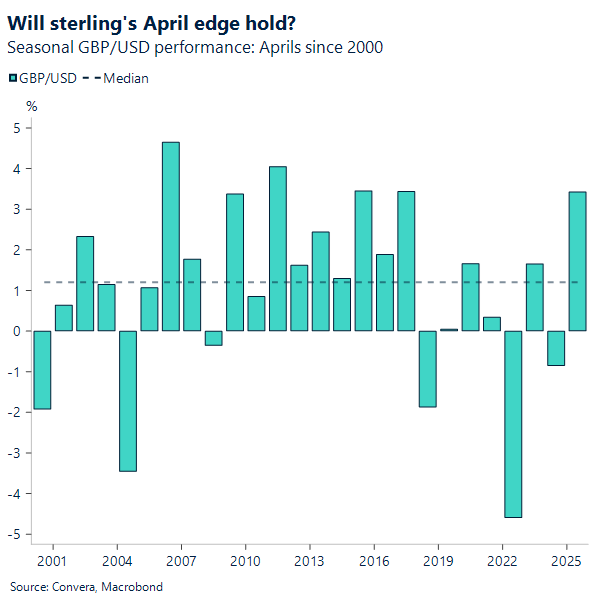

Hopes of a peace deal between the US and Iran have delivered a strong tailwind to GBP/USD, propelling the pair above 1.35 and to post-war highs, as oil prices erased most of their weekly gains and risk appetite improves. The pound is now sitting over 2% higher month-to-date, consistent with sterling’s April seasonality, which we highlighted at the start of the month.

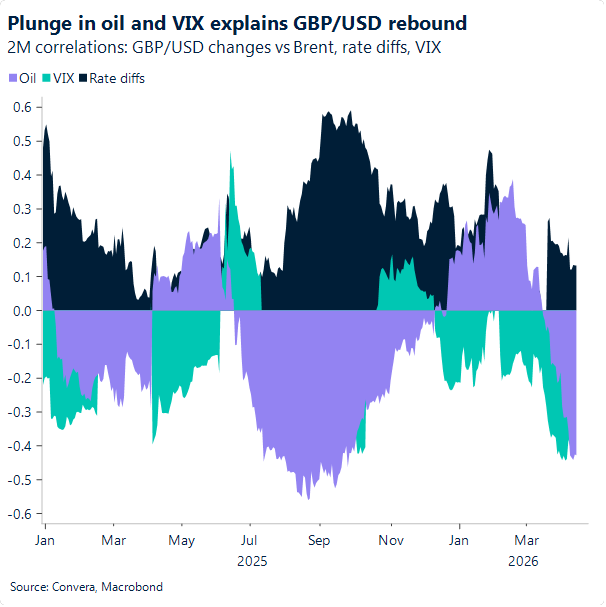

For the UK, a net energy importer with one of Europe’s highest exposures to gas fired power, the conflict had imposed a clear terms of trade drag. Elevated crude and gas prices fed directly into inflation expectations, pushing breakevens higher and forcing markets to price an aggressive BoE tightening cycle. That hawkish panic supported sterling on the yield channel, but it was fundamentally fragile, driven by stagflationary pressure, not stronger UK growth.

The prospect of a peace deal flips that dynamic. With oil retreating and supply shock risks easing, the inflation premium embedded in UK assets is being priced out rapidly. Markets have moved from expecting three BoE hikes to just one, which weakens the pound’s yield advantage, containing gains elsewhere across the G10, but the tailwind from lower energy prices and firmer global risk appetite have done the heavy lifting on GBP/USD.

Technically, we called out the bullish break last week as being significant, opening the door to more upside potential. GBP/USD is now trading above all major daily moving averages, signalling a re-established bullish trend. The peace deal narrative has also reduced volatility premiums, easing the pressure that had made GBP appear more vulnerable than the euro in recent weeks.

Overall, it seems like the bar for fresh FX volatility has risen as the constant to-and-fro of escalation and de-escalation is generating diminishing marginal impact. This doesn’t mean risks have vanished, far from it. It just might be that the market has become more desensitized to incremental geopolitical headlines. Watch out for a host of BoE speakers today though, likely giving guidance on what and when the next policy move is.

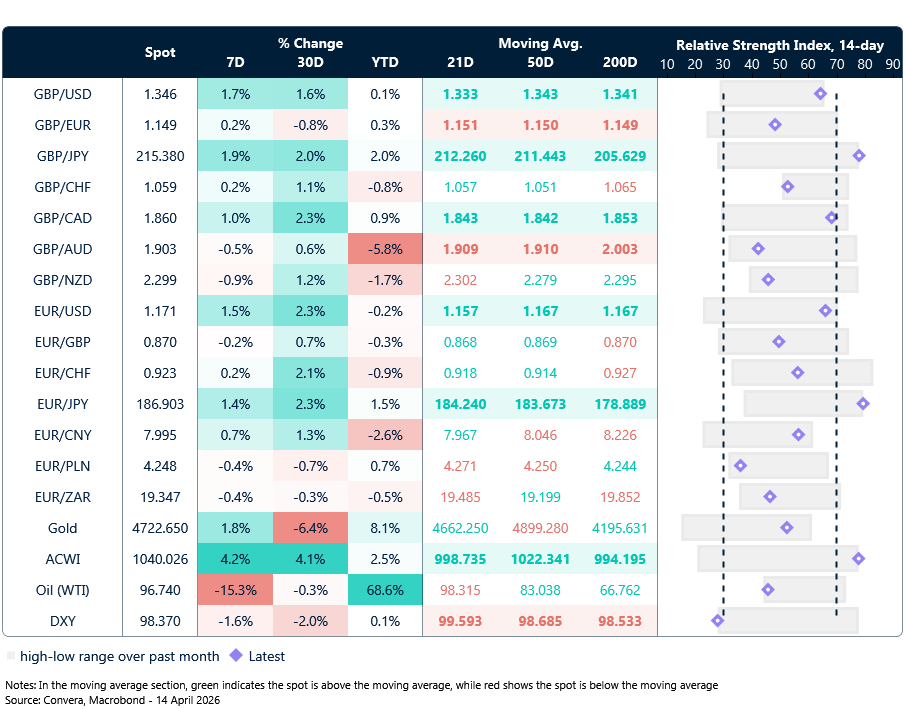

Market snapshot

Table: Currency trends, trading ranges & technical indicators

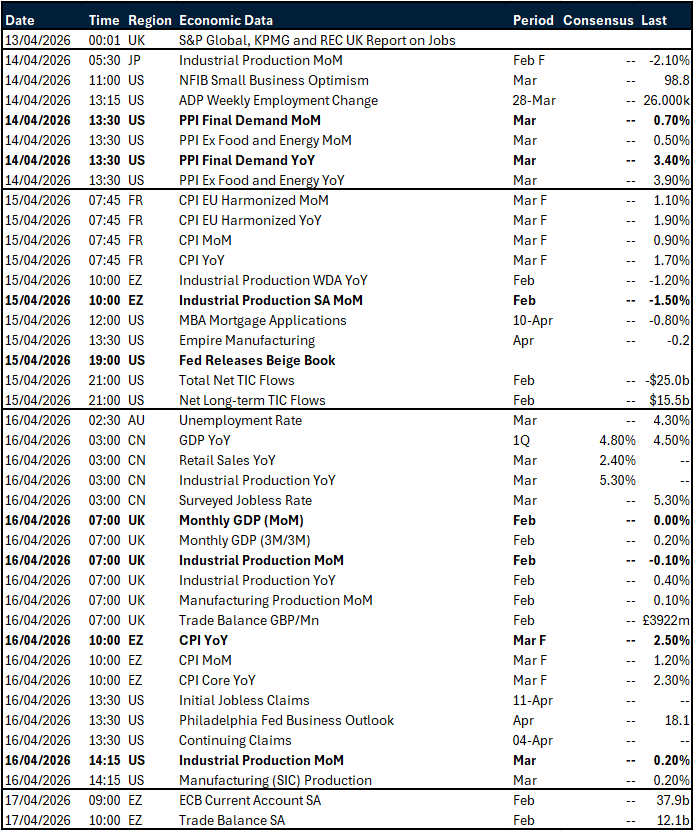

Key global risk events

Calendar: April 13-17

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.