Global overview

Global sharemarkets extended last week’s rally with hopes for an end to Federal Reserve rate hikes driving sentiment. However, the USD staged a recovery, with the greenback mostly higher, but notably weaker in Asia. Today, all eyes are on the Reserve Bank of Australia, with its monthly rate decision due at 2.30pm AEDT.

Global shares extend rally, but USD recovers somewhat

Financial markets started the new week cautiously positive with US shares higher after last week’s monster rally.

US shares surged last week on hopes the US Federal Reserve was near the end of its rate hiking cycle.

The US sharemarket continued the gains on Monday with the S&P 500 up 0.2% and the Nasdaq up 0.4%.

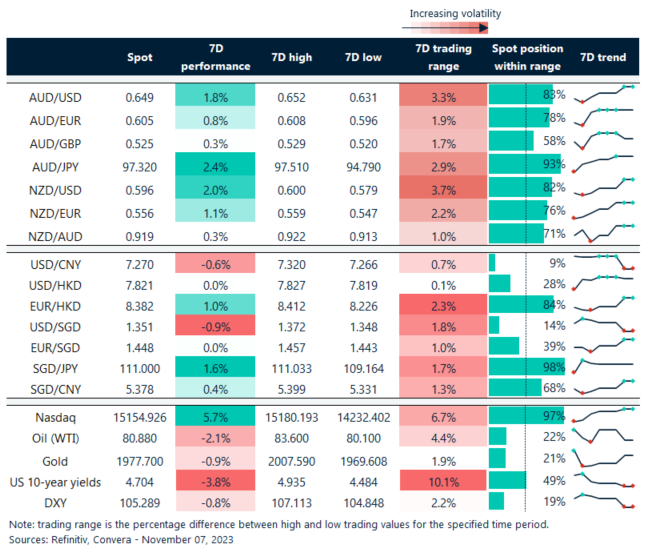

However, the US dollar mostly rebounded, thanks to a recovery in US bond yields. The US ten-year bond yield jumped from a six-week low of 4.48% seen on Friday to end at 4.57% overnight. The US ten-year yield hit a 16-year high of 5.02% on 23 October.

The EUR/USD fell 0.1%, GBP/USD lost 0.3% while the USD/JPY gained 0.5%.

In Asia, however, the US dollar remained pressured, with the USD/SGD down 0.3% and the USD/CNY down 0.4%.

Aussie weaker ahead of RBA

The AUD/USD fell 0.4% ahead of today’s key Reserve Bank of Australia decision. The RBA looks likely to lift interest rates after a four-month hiatus with the market pricing a 60% probability of a 25-basis point increase to 4.35% according to Refinitiv.

A Reuters poll found 34 of 39 economists expect a hike

The RBA is likely to be driven by three big considerations. First, the labour market is still strong, with the unemployment rate (3.6%) remaining lower than the Non-Accelerating Inflation Rate of Unemployment (around 4.25%).

Second, the unsatisfactory third-quarter inflation statistics, which revealed wider-ranging price increases—including those in services—and more robust-than-anticipated price increases.

Lastly, the outlook for Australian now looks better, and we might see updates to the RBA’s projections, which should indicate somewhat better GDP growth, somewhat lower unemployment, and a little higher CPI profile. The RBA’s end-point projections for CPI inflation, however, should not exceed 3.0%.

The policy guidance will likely stay essentially the same, signaling a little tighter stance and repeating that more tightening could be necessary depending on new information and how risks develop.

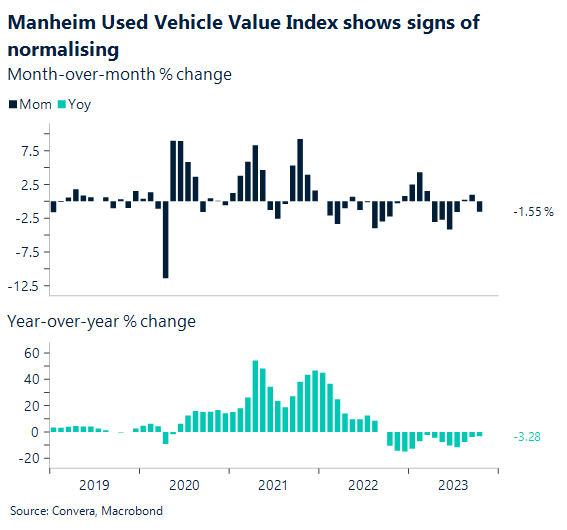

US used cars key for inflation – and USD

The US’s super-hot inflation readings in 2021 and 2022 were partly driven by higher under car prices. But what’s happening now? Tonight, we’ll see the US Manheim used vehicle index.

After rising for two months in a row, the preliminary October Manheim wholesale used car price index started to fall in early October. The UAW strike, in our opinion, had little effect on the supply of automobiles, and as credit requirements for auto loans tightened more, used car prices are expected to fall.

The Manheim figures from October are key to the CPI reports for November and December – weaker CPI result could drive further losses in the USD.

USD extends losses in Asia

Table: seven-day rolling currency trends and trading ranges

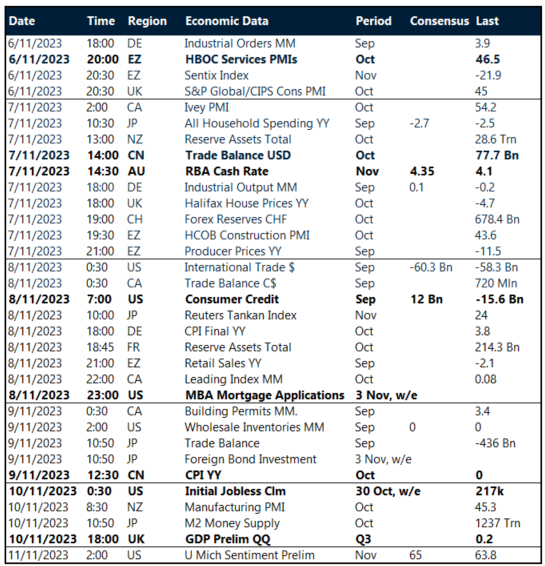

Key global risk events

Calendar: 6 – 11 November

All times AEDT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.