Written by Steven Dooley, head of Market Insights

Global overview

US shares started the new week strongly with the Dow Jones index up 1.6% overnight. The Aussie was the best performer after a stronger than expected retail sales number made an RBA rate hike more likely next week. Today, China PMI are due, but all the focus will be on the Bank of Japan. Will the BoJ make a small step to tighten policy?

US shares rebound in line with recent “Monday effect”

Global markets bounced on Monday – in fact, US shares have gained on 16 of the last 17 Mondays as per Bloomberg – as fears of a full-blown escalation in tensions in the Middle East eased.

The US’s S&P 500 gained 1.2% – in the index’s best day in two months – while the Nasdaq gained 1.1%. The US ten-year bond yield was broadly unchanged at 4.859%.

In FX, most risk sensitive currencies were higher, led by the AUD/USD, up 0.6%, after a stronger than expected retail sales number.

September retail sales were up a whopping 0.9% and the result makes a rate hike from the Reserve Bank of Australia more likely. The market sees a 60% chance of a hike according to Refinitiv.

In other markets, the EUR/USD gained 0.5% while the GBP/USD gained 0.4%.

The NZD/USD climbed 0.5%. The USD/SGD fell 0.5% while the USD/CNH lost 0.1%.

China PMIs due

The early focus today is China’s official PMI numbers.The official PMI for non-manufacturing is expected to decline from 51.7 in September to 51.5 in October due to the services sector’s probable loss of momentum after the Golden Week break.

Since May, the services sector’s new orders sub-index has been in contractionary territory for five months running. This is a strong indication that the formerly strong demand for travel and social events is quickly waning.

In the meanwhile, October’s PMI for the construction industry is probably going to remain high as Beijing works push for the completion of pre-sold houses and reduce the dangers connected with local governments’ growing hidden debt.

The manufacturing number is expected to hold on to its recent recovery above the boom-bust level of 50.

BoJ to be closely watched

The highlight today will likely be the Bank of Japan decision due sometime after midday (there is no fixed time for the announcement).

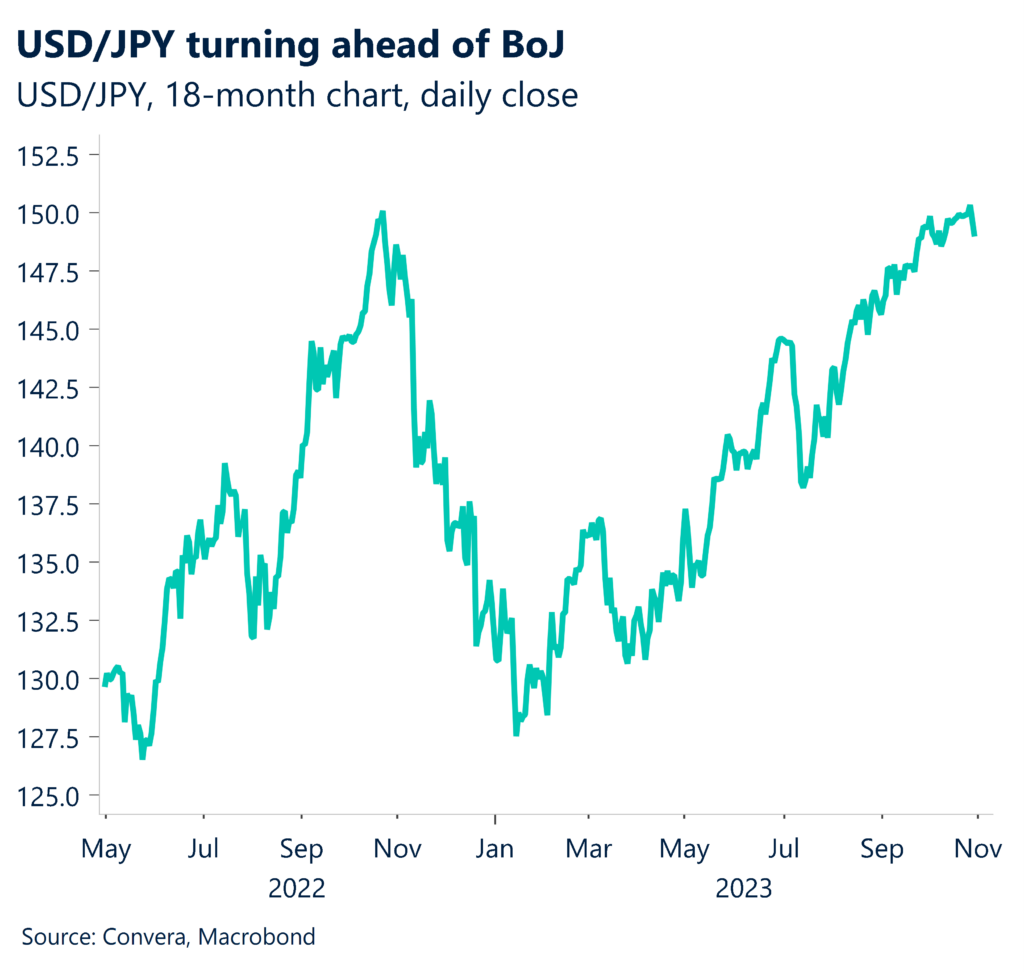

After last week’s higher than expected Tokyo CPI reading, there is more reason for the BoJ to make a small move to tighten policy, which could boost the Japanese yen. The USD/JPY fell 0.4% overnight.

Tonight, from the US, August’s Case-Shiller house price index is likely to only see mild gains after July’s 0.9% month-over-month gain.

Following two months of 0.4% increases, the CoreLogic HPA index rose by 0.3% in August. High mortgage rates are both weighing on demand and restricting supplies, with homeowners hesitant to give up their low-rate fixed-rate loans.

Aussie reaches two-week highs

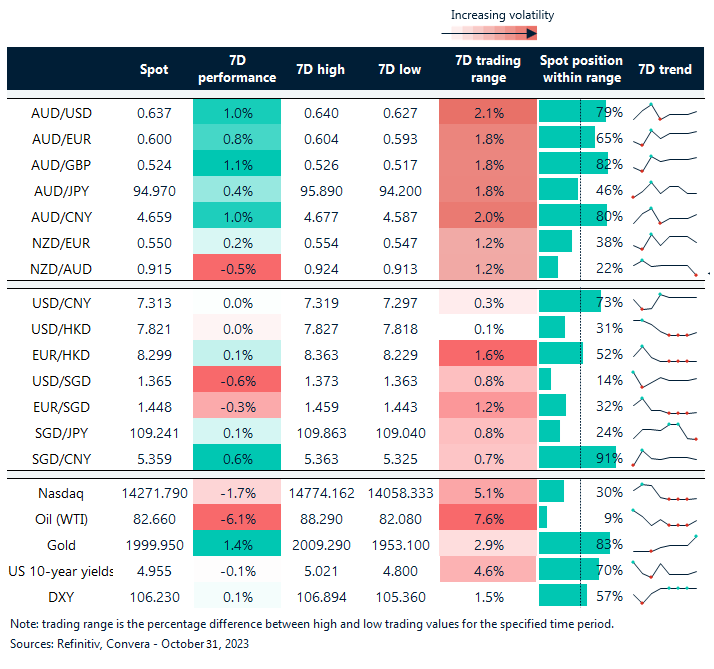

Table: seven-day rolling currency trends and trading ranges

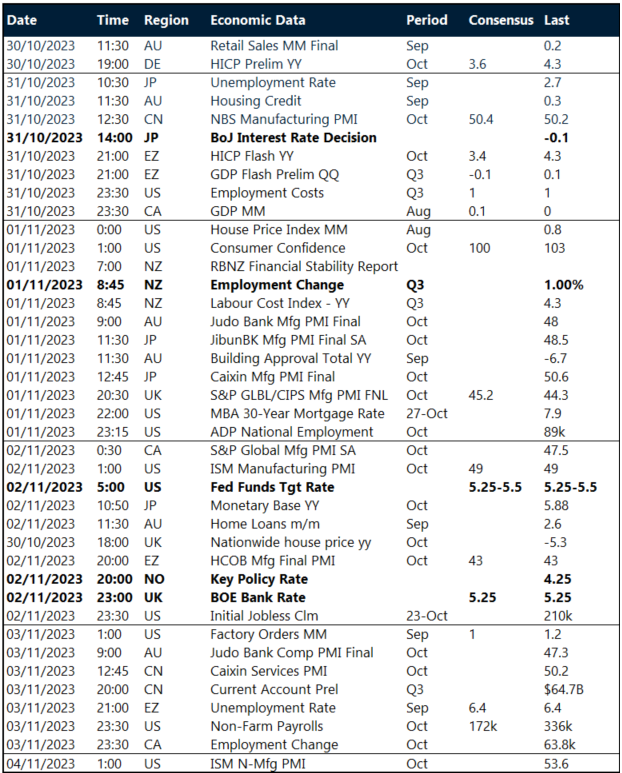

Key global risk events

Calendar: 3 October – 4 November

All times AEDT

Have a question?[email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.