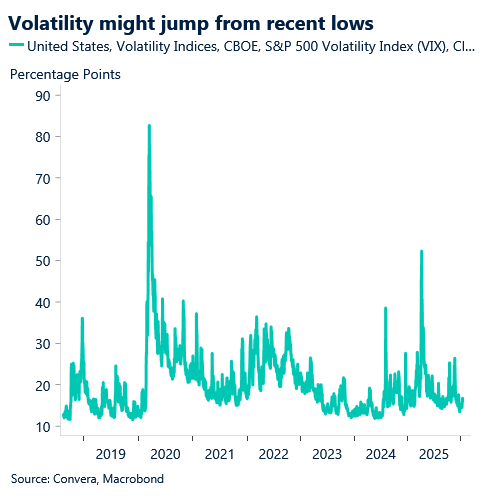

Greenland threat hits risk sentiment

Global markets opened Monday weaker after US President Donald Trump announced new tariffs on eight European countries over the weekend as he continues to push for “the complete and total purchase of Greenland.”

The euro and pound fell on the news, with the EUR/USD and GBP/USD both down 0.2%.

The AUD/USD was also one of the hardest‑hit markets, with the pair falling 0.2% to one‑month lows.

President Trump said he would introduce a 10% tariff on the UK, Germany, France, Denmark, Sweden, Norway, Finland, and the Netherlands starting 1 February, due to their support for Greenland. The tariffs will rise to 25% on 1 June.

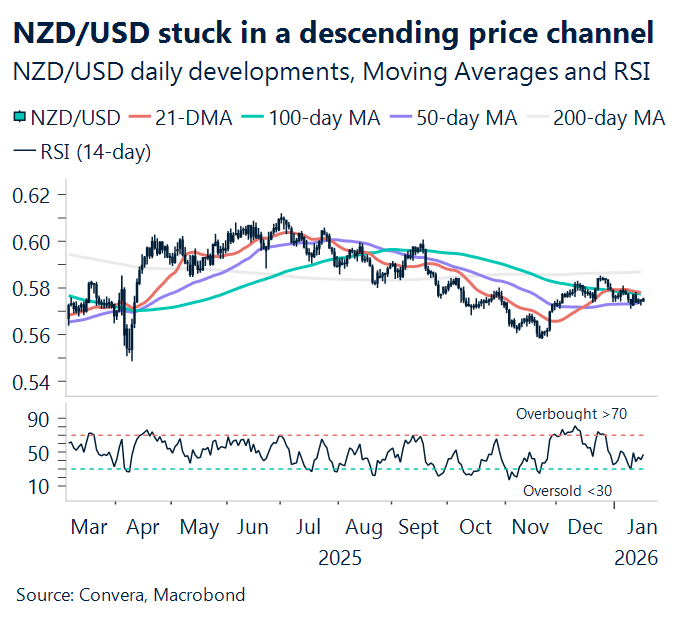

The NZD/USD fell 0.1%. In Asia, the USD/JPY fell 0.2%, while USD/SGD and USD/CNH were steady.

NZD/USD lifts as NZ manufacturing hits four‑year peak

Economic news in New Zealand showed further signs of improvement last week. New Zealand’s manufacturing sector surged in December, with the PMI climbing 4.4 points to 56.1 – its strongest reading since December 2021.

The neutral 50 mark separates expansion from contraction.

BNZ economists said the result shows momentum in a recovery already underway, pointing to stronger domestic demand, improved export activity, and renewed business confidence.

Government officials noted the sector is now outperforming major global economies, entering the new year with renewed strength and underscoring manufacturing’s central role in jobs, exports, and growth.

The kiwi dollar has edged higher, now 5% above its 9 April 2025 low of 0.5486. The pair faces resistance near 0.5783, the 100‑day moving average.

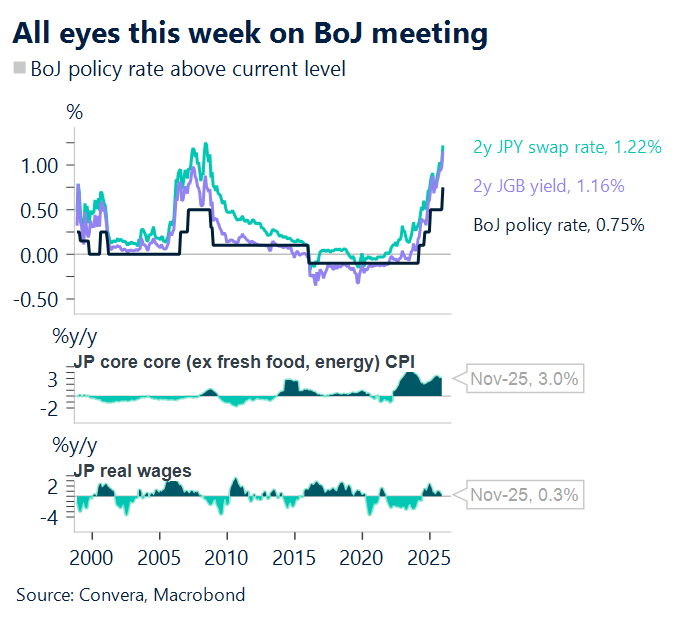

Markets eye BoJ decision as data rolls in

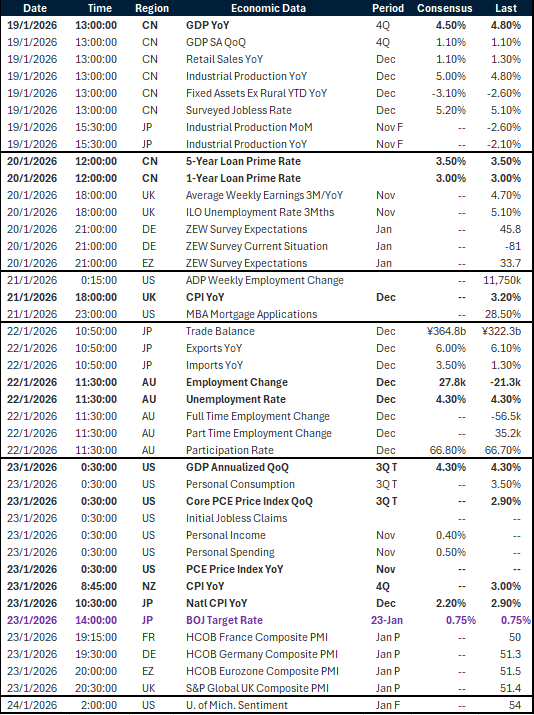

The week opens with China’s Q4 GDP (4.5% YoY consensus), retail sales, and industrial production on Monday, setting the tone for regional risk appetite. The PBOC’s loan prime rates are expected to remain unchanged Tuesday.

Wednesday sees UK December CPI, which is expected to stay elevated, reinforcing the Bank of England’s cautious stance.

On Thursday, Australia’s December employment report will be pivotal for the AUD, with consensus looking for a rebound in jobs (+27.8k) and unemployment steady at 4.3%. Japan’s December CPI (Friday) will be scrutinized for signs of persistent price pressures.

In Japan, attention turns to Friday’s Bank of Japan meeting, where the BOJ Target Rate is forecast to hold at 0.75%. Markets will watch for any hawkish signals as inflation remains above target and speculation of further tightening persists.

US Q3 GDP (Friday) is forecast at a robust 4.3% annualized, alongside core PCE inflation and jobless claims. These releases will be key for Fed rate expectations. Eurozone and UK PMI data (Friday) will provide fresh insight into growth momentum across major economies.

Central banks remain data‑dependent, and this week’s releases could drive FX volatility, especially if growth or inflation surprises. The dollar may find support if US data outperforms, while AUD, GBP, and JPY will be sensitive to domestic releases and central bank signals. Markets should brace for potential swings as policy outlooks are recalibrated in response to the latest data.

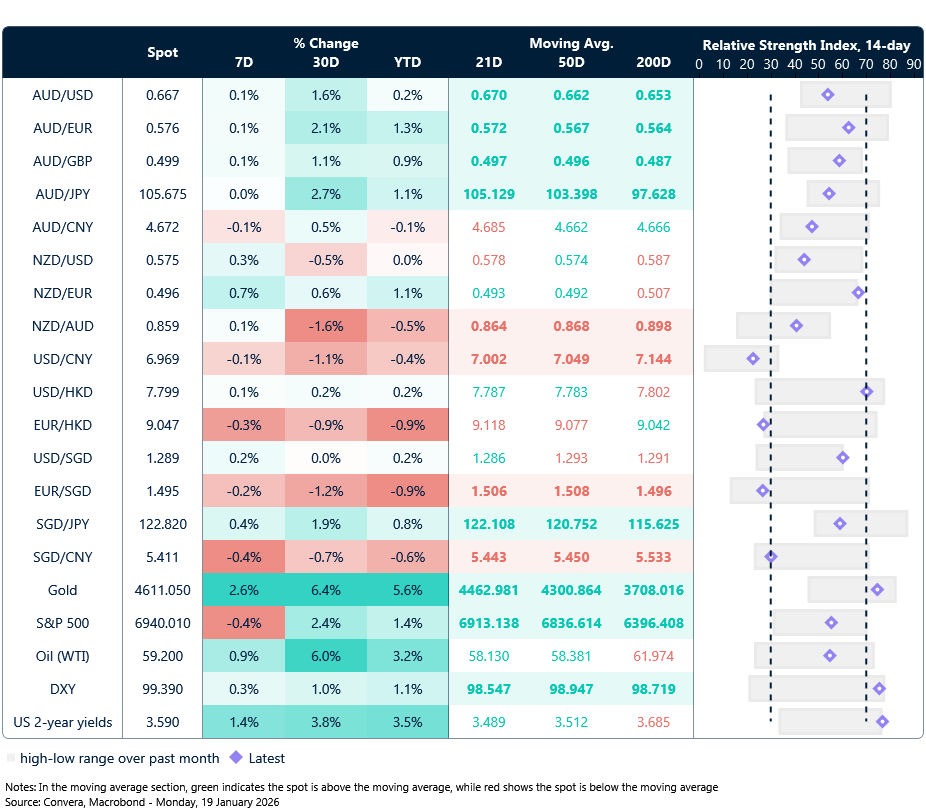

USD higher on Greenland worries

Table: seven-day rolling currency trends and trading ranges

Key global risk events

Calendar: 19 – 24 Jan

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.