Written by Steven Dooley, Head of Market Insights, and Shier Lee Lim, Lead FX and Macro Strategist

Check out our latest Converge | Podcast on Spotify covering the USD’s rise in Q1, the paring back of interest rate cuts for 2024, the surprise rate cut in Switzerland, the divergence between the Fed and ECB and the volatility puzzle in FX.

US jobs beat for fifth-straight month

The US dollar ended higher on Friday after a volatile session following another bumper US jobs report.

The US’s non-farm employment report beat forecasts for a fifth-consecutive month with 303k new jobs added and the unemployment rate falling from 3.9% to 3.8%.

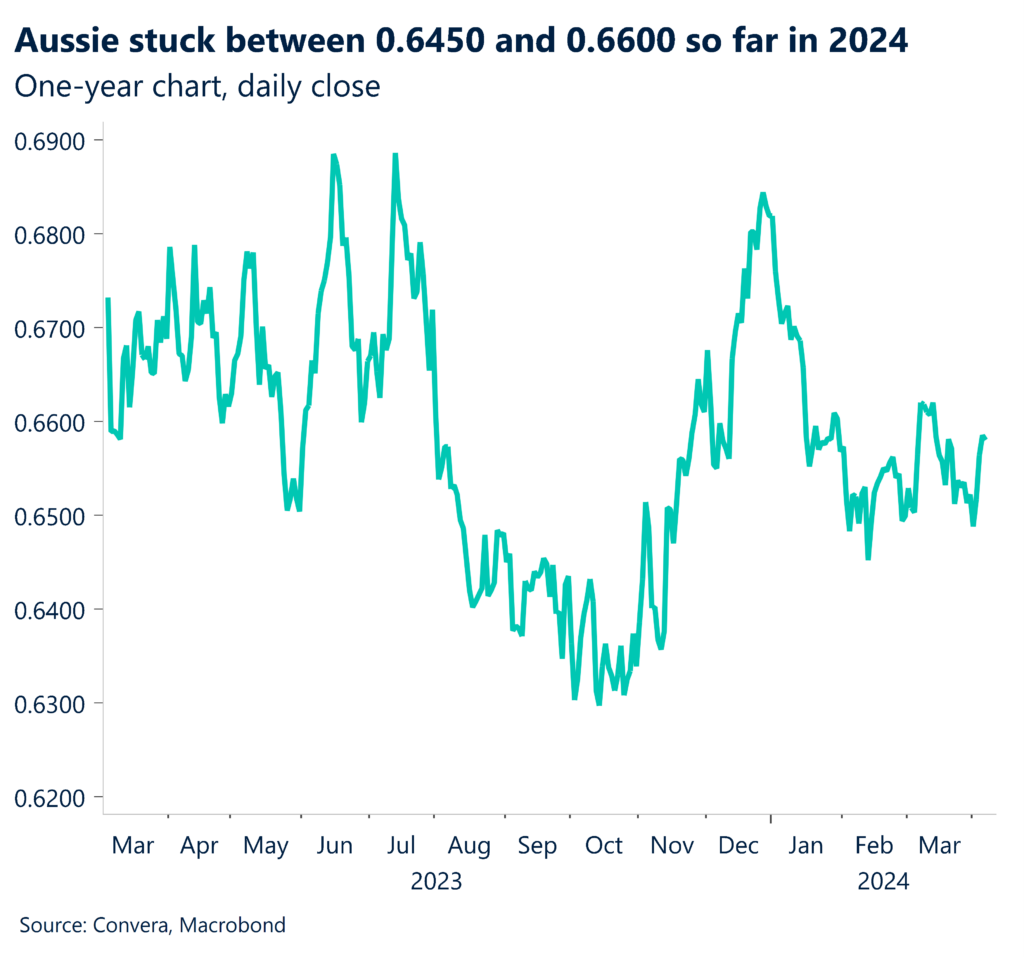

The stronger US dollar saw the AUD/USD and NZD/USD both reverse from the top of recent trading ranges with the AUD/USD down 0.1% and NZD/USD down 0.2%.

The euro, British pound and Japanese yen also fell against the USD dollar. The USD/SGD climbed 0.2% while the USD/CNH bucked the trend and fell 0.1%.

Looking to the week ahead, central banks will be the highlight, with the European Central Bank, Reserve Bank of New Zealand and Bank of Canada all due.

The Federal Reserve’s minutes from their most recent policy meeting are also released on Thursday morning. From an economic data perspective, the US CPI inflation release, due Wednesday night, is likely to be the main event.

Greenback to be driven by CPI, Fed

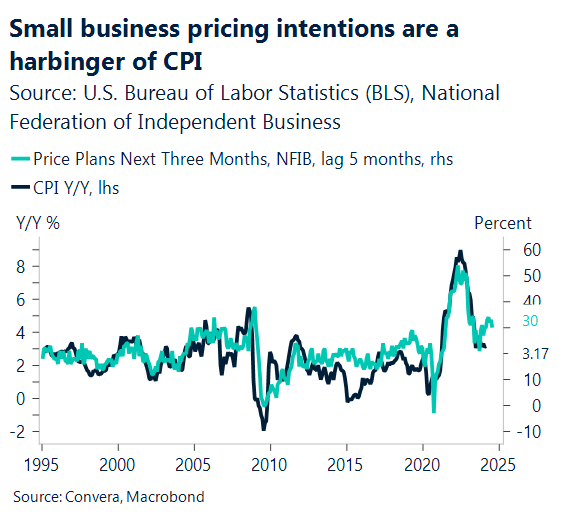

The ongoing strength of the US economy will likely be reflected in this week’s NFIB small business optimism index. We anticipate a little increase in the NFIB small business optimism index in March.

A rise in the proportion of businesses anticipating an improvement in the economy is probably due to expectations for rate cuts and loosening financial restrictions. Small firms continue to express worry about the quality of workforce.

According to the March Dallas Fed Banking Conditions Survey, tightening credit conditions and falling loan volumes probably had an effect on the net proportion of businesses anticipating credit conditions to loosen and preparing to undertake capital expenditures.

For the greenback, the tone this week will be set by US inflation and the Fed minutes. The USD’s positive growth and carry dynamics might continue to add support.

Eurozone bank lending survey

Ahead of the major European Central Bank meeting, this week, the Bank Lending Survey is likely to be less of a story because the ECB is happy with how the transmission process to credit conditions has gone thus far and the phase is almost finished.

But if lending demand is poor and credit standards are high, this might jeopardize the Eurozone’s growth profile and raise questions about whether the ECB overtightened.

After sustaining the 1.0694–1.0724 support layer, EUR/USD is currently trading around the center of the 2024 trading range.

The major resistance at 1.10 (see chart) represents a potential key resistance for EUR/USD.

Aussie, kiwi slip from recent highs

Table: seven-day rolling currency trends and trading ranges

Key global risk events

Calendar: 8 – 13 April

All times AEDT

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.

Have a question? [email protected]

Take a deep dive into the trends shaping cross-border payments with our podcast, Converge.