USD: Inflation in focus

The dollar pared back losses during early London trading hours on Friday, as Trump admitted threatened tariff rates against China would not be sustainable. National Economic Council Director Kevin Hassett added that he had “high confidence” Trump and others would be able to meet with Chinese officials and bring the situation “back to a place that’s good for both countries.” These headlines were hard to digest (although not entirely surprising), given that just a week earlier Trump had threatened a 100% tariff on Chinese goods by November 1 and floated the idea of canceling the planned meeting with Xi, scheduled for later this month. Yet another textbook TACO setup.

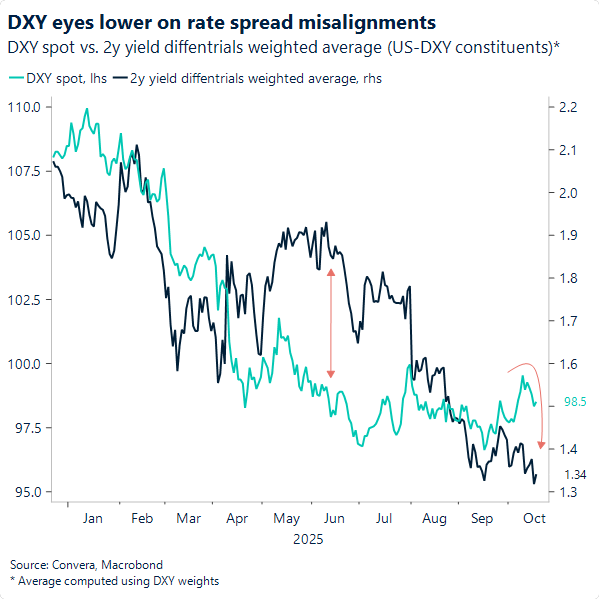

The event itself exerted moderate bearish pressure on the dollar from the outset, although the shutdown continues to amplify outsized reactions – both bearish and bullish – to headlines. Behind these sentiment-driven moves lies the dollar’s true bearish driver: the Fed’s dovish lean, which capped Friday’s rebound. With the Fed’s dovish path now more settled, the dollar index’s current level – relative to where it “should” be trading based on rate differentials with its constituents (see chart below) – suggests the currency remains poised to edge slightly lower this week as it completes its re-alignment with fundamentals.

All eyes are on Friday’s inflation report – due Friday – the first major hard data release since the shutdown began. The BLS has pushed ahead to compile the data regardless, aiming to provide a pulse on US price pressures ahead of the October meeting. Meanwhile, the Fed has entered its blackout period.

EUR: Realignment, not breakout

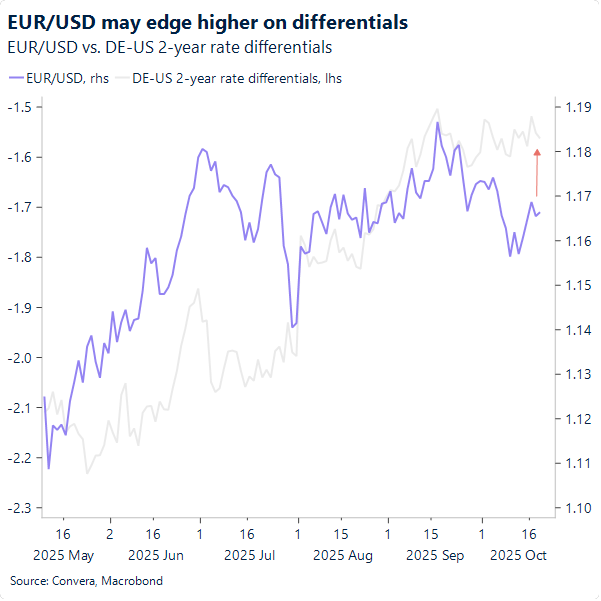

The euro closed the week 0.7% higher against the dollar, after paring back gains and failing to break resistance at 1.1720, as the greenback benefited from an end-of-week sentiment boost.

The week also ended with remarks from ECB President Christine Lagarde, who noted that while the outlook for euro-area inflation remains uncertain, as the still-volatile global trade environment continues to pose both upside and downside risks, the range of risks on both sides has narrowed. While the comments were directionless and unlikely to move price action on their own, one could infer that with a cleaner canvas to work from, the next upside or downside surprise may carry greater weight in shaping ECB expectations.

To start, the final eurozone core inflation year-on-year print was revised up to 2.4% from 2.3%, while other releases came in line with expectations on Friday. The data reinforces the consensus around a comfortable rate setting for now.

All else equal, we maintain a bias for EUR/USD to edge higher this week – as the pair continues to benefit from the Fed’s dovish lean relative to a firm ECB, as calmer sentiment conditions allow rate differentials to exert greater influence. That said, short-term price action suggests anything above 1.1750 seems hard to achieve for now.

GBP: Sticky inflation, stuck policy

Investors are eagerly awaiting Wednesday’s UK inflation report – recall that inflation remains the BoE’s key headache. While officials have signalled a willingness to cut, citing a softening labour market in recent interviews, persistently high price pressures – driven in part by elevated wage growth – continue to restrain that dovish pivot.

UK CPI is expected to hit 4%, mainly due to fuel prices, while services inflation is forecast to remain unchanged. Although supply-driven shocks are typically less sticky than demand-driven ones, the current setup points to more pressure from the former. Still, markets are likely to take the headline print at face value – high inflation is high inflation – injecting some bullish fuel into sterling regardless of the underlying drivers.

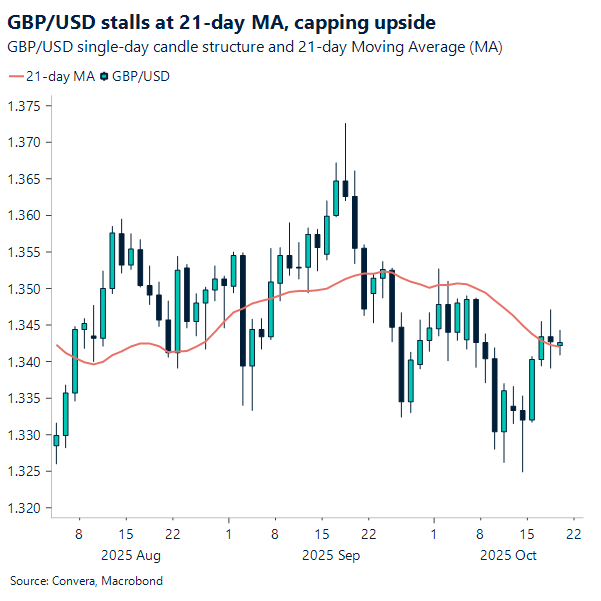

That said, with markets pricing in just over a 10% chance of a cut this month, the residual pricing out of those expectations may not be enough to push sterling through what appears to be a newly formed GBP/USD resistance level – namely, the 21-day moving average, in place since late September. This unbroken resistance streak keeps the pair anchored, reinforcing the case for a deeper short-term bearish trend.

EUR/CHF and GBP/CHF tests lower bound of RSI range

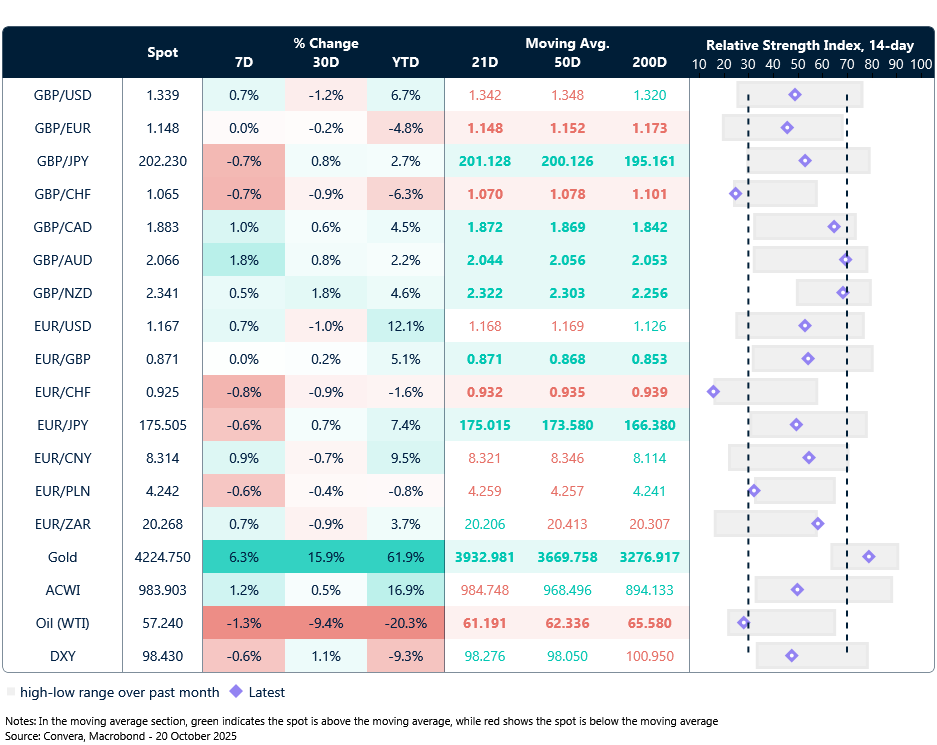

Table: Currency trends, trading ranges and technical indicators

Key global risk events

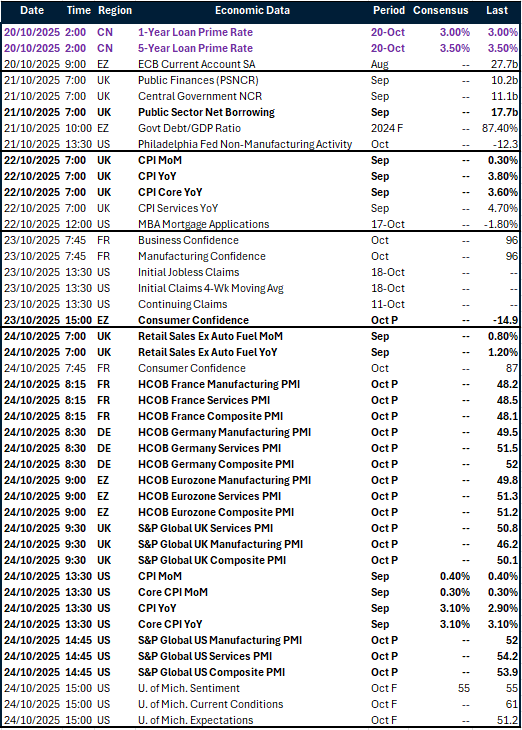

Calendar: October 20-24

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.