Written by Convera’s Market Insights team

A sterling Q3 performance for the pound

George Vessey – Lead FX Strategist

With the US dollar strengthening on Fed Chair Powell’s comments yesterday, GBP/USD pulled back from $1.34 yet again. After pushing through this key level for the first time in over two years last week, the currency pair has breached it for five days in a row, before closing lower each time. Given this price action, we question whether $1.35 is too much of a stretch without a fresh positive catalyst for sterling.

Positive seasonal trends bode well for a strong end to the year though. For last five years, GBP/USD has risen, on average, 1.8% in October and over the last ten years, the fourth quarter has been its strongest quarter by far. But we can’t place too much weight on seasonality, as evidenced by the pound defying weak seasonal trends in Q3, appreciating by almost 6% against the dollar compared to its 10-year average performance of -2.4%. From a macro perspective, we had revised second quarter GDP figures released yesterday showing the UK economy grew more slowly than estimated, partly because the households savings rate climbed to the highest since 2021. Despite economic activity moderating and the prospect of higher taxes in the Budget on October 30 further hitting consumer spending, growth could hold up well if households dip into these savings that have been building since Q1 2023.

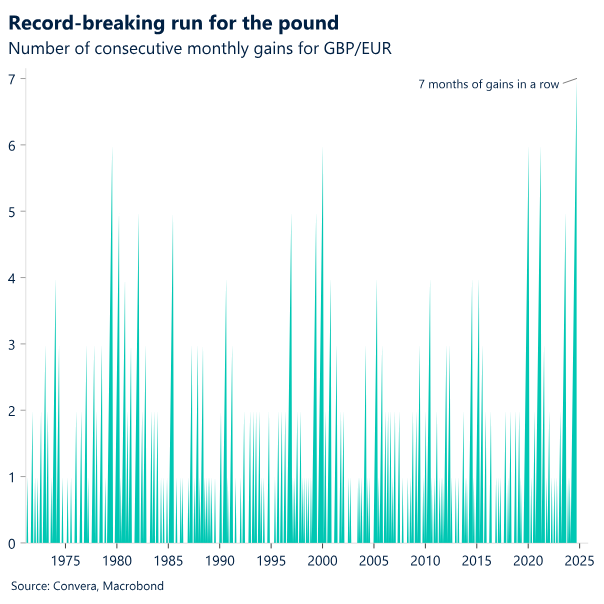

As such, the UK’s economic outlook remains far more upbeat than its European peers, hence the Bank of England’s more cautious stance on cutting interest rates. This gives the pound both a growth and yield advantage over the euro, which is why GBP/EUR is on a record-breaking monthly run. Sterling also closed the month out above €1.20 versus the euro, marking its first such achievement since May 2016.

Dollar benefits from trimmed 50bps cut bets

Ruta Prieskienyte – Lead FX Strategist

After two consecutive days of declines, the dollar regained some strength on Monday, with the US dollar index (DXY) bouncing off its 200-week moving average support level. Despite this late recovery, the DXY ended the quarter nearly 5% lower, marking its worst Q3 performance since 2012. The dollar continues to underperform against commodity-linked G10 currencies as well as the British pound, but advanced against safe-haven currencies and Scandinavian currencies. The dollar was also buoyed by a cautious sentiment in North American and European equity markets, despite a strong rally in China’s CSI 300, which surged over 8% during Monday’s trading.

On the macroeconomic front, both the Chicago and Dallas manufacturing indices surprised to the upside. The Chicago PMI edged up to 46.6 in September from 46.1 in August. Although still in contractionary territory, the details were mixed: order backlogs and employment showed slight improvements, while supplier deliveries, new orders, and production continued to decline. Additionally, prices paid remained elevated for the second consecutive month. A combination of better-than-expected macro data and Powell’s speech hinting at a more gradual rate cut pace led the market to slightly reduce expectations for a November rate cut. The yield on 2-year US Treasuries increased by 5 basis points, causing the yield curve to bear flatten. The probability of a 50 basis point rate cut in November dropped below 50%, according to both Fed fund futures and overnight index swaps, reflecting growing uncertainty over whether a back-to-back jumbo rate cut is necessary based on the current economic evidence. While this macro data is positive, the Federal Reserve’s primary focus remains on the labour market, which, despite volatility and notable revisions, has shown signs of cooling in recent months.

On today’s economic calendar, the key data releases include JOLTS, which surprised to the downside last month, and the ISM manufacturing index, which is expected to remain around the 47-48 range ahead of this week’s main event, the US NFPs report on Friday. Throughout the day, several Fed officials—Bostic, Cook, Barkin, and Collins—are also scheduled to speak, which may provide further insights into the Fed’s policy outlook. From a political perspective, today’s televised debate between US vice-presidential candidates JD Vance and Tim Walz could inject some fresh volatility into FX markets overnight. This debate represents the last opportunity for either campaign to make a significant impact in front of voters, as Donald Trump has ruled out another debate with Kamala Harris. Polls will be closely watched to gauge any potential influence. Currently, the PredictIt index shows Kamala Harris ahead with a 56-47 margin to win the election in November, while Polymarket predicts a tighter race, with Harris leading 50.2-48.8.

Soft inflation strengthens the case for an ECB October cut

Ruta Prieskienyte – Lead FX Strategist

Germany’s preliminary annual inflation rate dropped to 1.6% in September, below the forecast of 1.7% and down from 1.9% in August, marking the lowest reading since February 2021. The cost of goods declined by 0.3%, while services inflation, a measure closely monitored by the ECB Governing Council, eased slightly to 3.8% from 3.9%. The core inflation rate also declined, falling to 2.7%, its lowest since January 2022, from 2.8%. On a month-to-month basis, the CPI showed no growth, against expectations of a 0.1% increase. Similarly, the EU-harmonised CPI dropped to 1.8% year-on-year, below the consensus forecast of 1.9%, and decreased by 0.1% month-on-month.

Since last Friday, preliminary inflation figures from France, Spain, and Italy have also come in lower than anticipated. Given the cumulative downside surprises, the European Central Bank (ECB) will have few reasons to avoid cutting rates, as evidenced by market pricing, where the probability of an October rate cut surged to over 90% in the Overnight Index Swap (OIS) curve, up from 40% just a week ago. Headline inflation progress has outpaced the ECB’s own projections, while risks to the growth outlook continue to mount. Reports emerged yesterday that Germany’s government is preparing to downgrade its forecast for the country’s economic growth, now predicting no expansion for this year, down from the previously projected 0.3%. There are strong reasons to expect an October rate cut, despite resistance from the ECB’s more hawkish Governing Council (GC) members. The recent macroeconomic data, market pricing, and a subtle shift in ECB rhetoric support this view. Last week, Isabel Schnabel, one of the ECB’s most influential members and a frequent signal of changes in GC thinking, highlighted growing growth risks, noting that disinflation remains on track. This sentiment was echoed by ECB President Christine Lagarde on Monday, who, while focusing on inflation, acknowledged that service prices are easing and core inflation is on a downward trend. Should the ECB choose not to cut rates in October and instead maintain a quarterly cadence, markets would likely view this as a policy misstep, leading to further bull steepening in the money market curve and raising concerns over the ECB’s credibility.

In terms of market reaction, EUR/USD continued to trade in a volatile manner due to quarter-end flows, but ultimately ended the day in the red. The euro touched $1.12 for the fourth time in seven days but has struggled to sustain levels above that mark. One key factor preventing the euro from advancing further is the widening of front-end rate differentials. Around the time of the Fed rate cut, the 2-year US-DE yield spread narrowed to 135 basis points, a multi-month low, but has since risen to 151 basis points, marking a one-month high.

In related developments in the bond markets, the 10-year OAT-Bund yield spread, a proxy for French risk premium, has climbed to 80 basis points, nearing its highest level since the end of June, as investor concerns about economic growth continue to intensify. Today, the French government faces a deadline to present its budget for parliamentary debate, raising the potential for further political turbulence. Additionally, credit rating agencies are set to review France’s fiscal health in the coming weeks, with Fitch and Moody’s scheduled to assess the country on 11 October and 25 October, respectively, following an earlier downgrade by S&P Global.

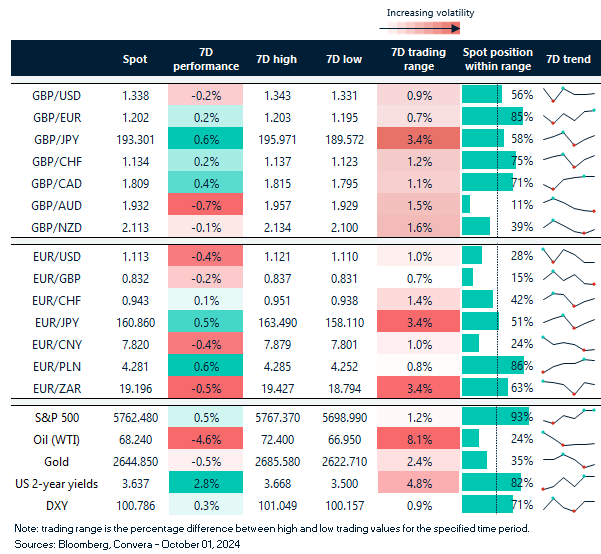

Euro feeling the pain

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: September 30-October 04

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.