Written by Convera’s Market Insights team

The backdrop going into November. The current global macro environment can be seen as a direct result of the pandemic and fiscal and monetary policy measures used during the last three years. We have previously defined the post-pandemic global economy from 2021 onwards by three distinct, yet interconnected characteristics. Global businesses and investors have lived through and dealt with (1) a high interest rates environment, where (2) the procyclical parts of the global economy have already fallen into recession in the developed world, (3) but where the consumer continues to power the rest of the economy with the excess savings built up during the lockdown period and amidst extremely tight labor markets. These three themes have governed macro and markets for the better half of the past two years.

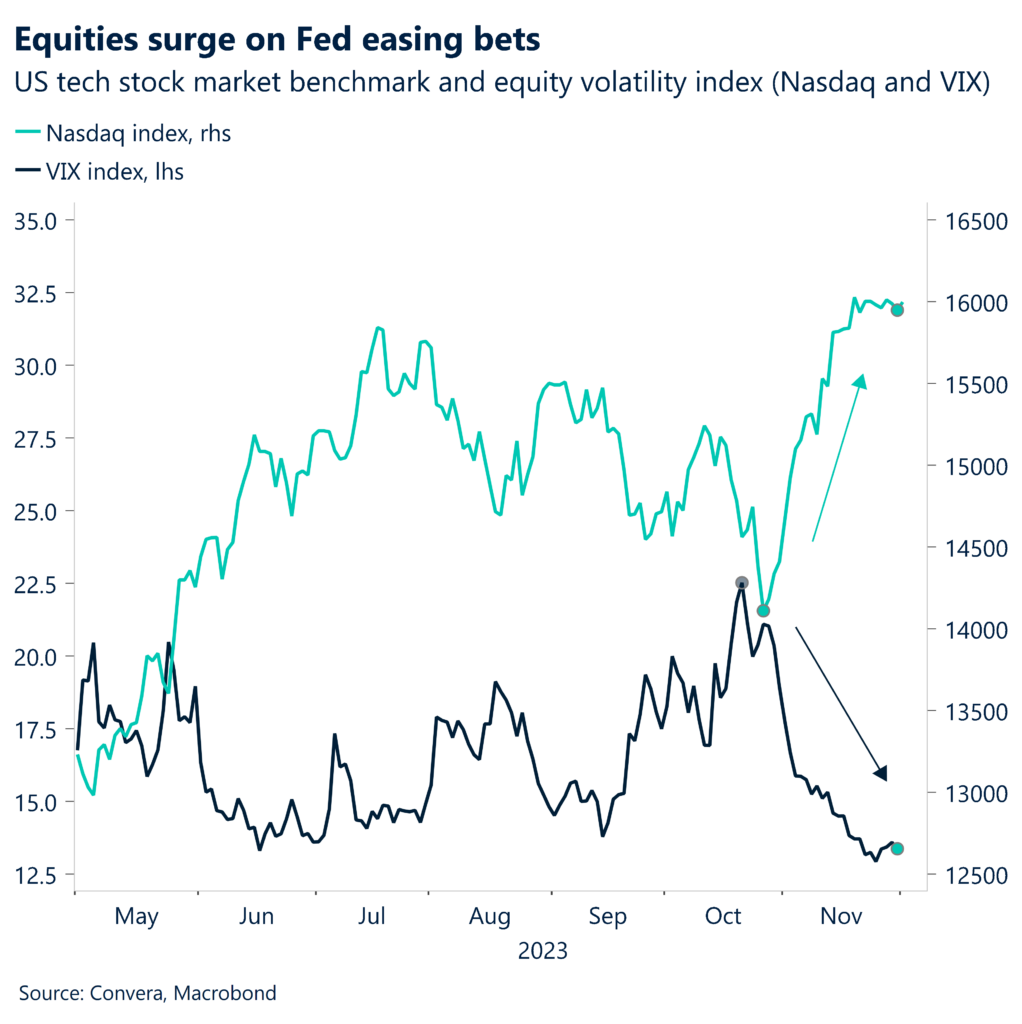

A regime shift on its way. We have noted recently in previous publications that all of those factors are in the process of slowly turning, which could make the upcoming quarters volatile. Interest rates seem to have peaked, the procyclical parts of the global economy are attempting to rebound and the consumer and labor markets are expected to weaken. And this potential macro regime shift is in our opinion the reason why the dollar has recently been on a downward trend and why global equities have recorded their best month in three years, up around 9% in November alone.

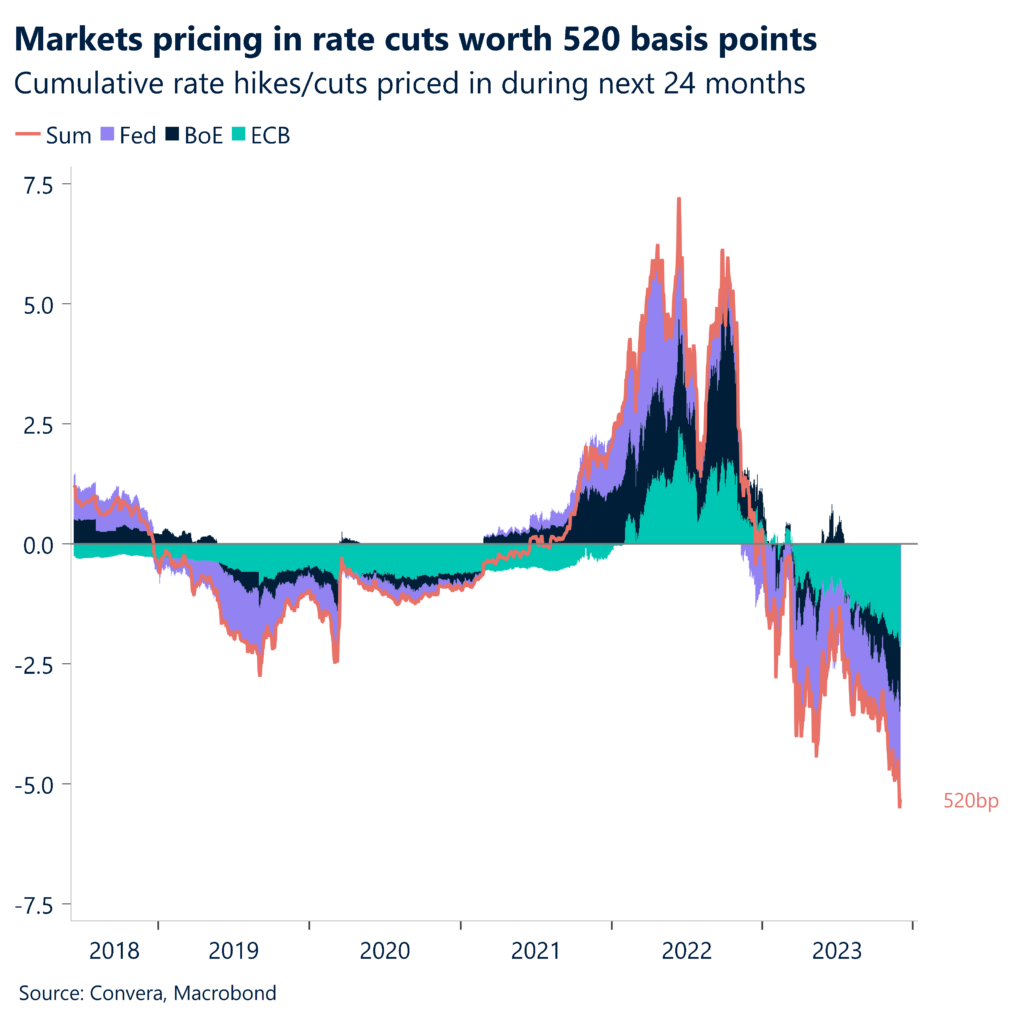

Let’s get specific. Going from the big picture themes to the specific events that have driven this change in sentiment in November, we once again highlight three developments. (1) G3 central banks deciding not to raise interest rates at their last meetings. (2) Signs emerging that the US labor market is cooling. (3) US, Eurozone and UK inflation surprising to the downside in October. This led to the largest monthly drop of the GS financial conditions index in the US in recent decades. Taken together, investors have felt comfortable to start pricing in significant rate cuts from the Federal Reserve, European Central Bank and Bank of England for 2024.

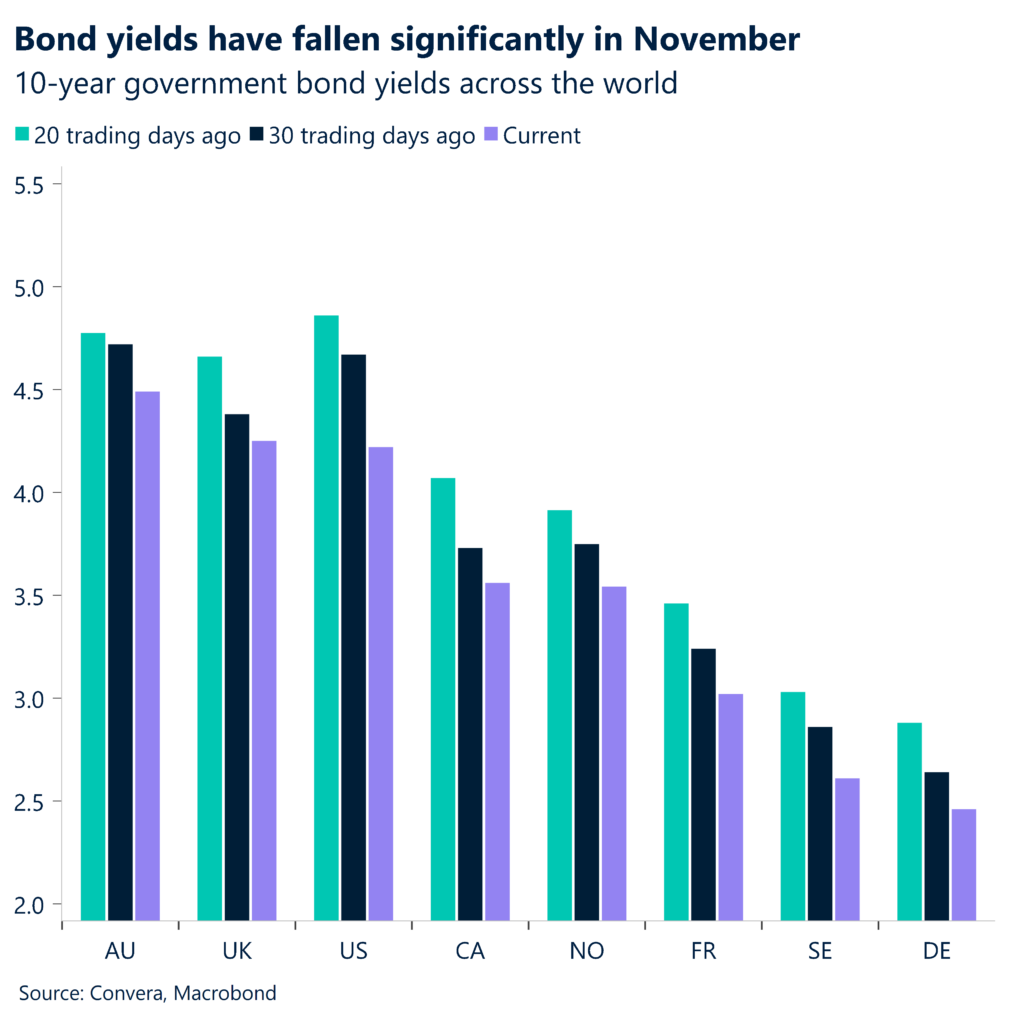

The result has been a historic November. November has gone into the record books as the best month for US Treasuries since the 1980s with the Bloomberg aggregate government bond index rising by more than 4% this month. The fall in yields has sparked an “everything rally” from high yield credit, to EM equities and FX. With the economic data in the US weakening enough for the Federal Reserve to consider ending its tightening cycle, but not enough to cause panic over a near-term recession, the soft-landing narrative has pushed up the MSCI World Index 9.1% in November. This thesis was reinforced this week with multiple Fed officials, notably Fed governor Christopher Waller, stating the central bank would be comfortable leaving rates at current levels for now. Markets are currently expecting the Fed to start its easing cycle in May and cut interest rates five times next year.

The US economy is slowing. The US economy slowed in recent weeks with inflation cooling and signs emerging that the labour market tightness is easing. New home sales in the US declined by 5.6% to 679,000 in October, following a strong growth rate of 8.6% in the previous month. At the same time, the general business activity index for manufacturing in Texas, published by the Federal Reserve Bank of Dallas, fell to the lowest level in four months in November.

Global Macro

Last week’s major events

US real (inflation adjusted) consumer spending and core inflation both grew by 0.2% in October, less than in the previous month. This comes as good news for the Fed, which has recently paused its tightening cycle. The Fed has made some progress on inflation as the central bank’s preferred price index (PCE) fell from 3.4% to 3.0%. At the same time, continuous jobless claims rise by 86,000 to 1.927 million ending 18 November, reaching the highest level since November 2021.

Disinflation supports ECB easing bets. Flash HICP data showed a more substantial-than-expected deceleration in inflation across the Eurozone, including Germany, Italy, and Spain. The headline rate declined to 2.4% y/y in November, reaching its lowest level since July 2021. Considering the latest developments, markets are pricing in 100 basis points of ECB easing for 2024 with the first rate cut near enough fully priced in for April.

European bottoming from low levels. At the same time, consumer sentiment in Germany for December improved marginally, partially reversing a decline since July. Confidence remains well above its nadir during the height of the energy shock last year but is still depressed overall. That said, this data follows a slew of improving soft (leading) indicators across Europe, although given the expected weakening of the European labor market and reduced fiscal spending, we’re not expecting a strong economic recovery next year. The main narrative in Europe is the following: Leading indicators are bottoming while hard data points remain depressed and are in some cases, especially on the labor market side, deteriorating.

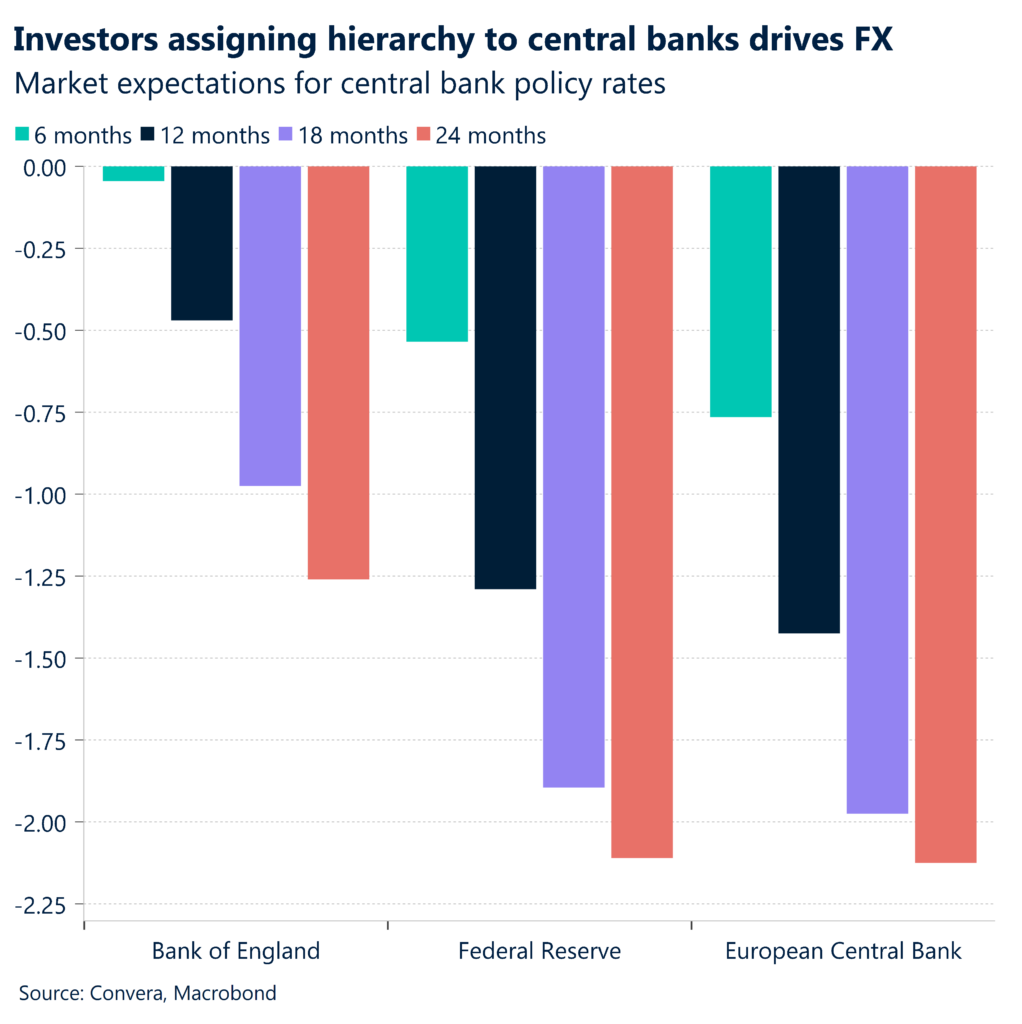

Markets priced for perfection. Markets are both positioned for a soft landing and for the Fed to cut rates. So, any economic data that comes in weaker than expected, is initially good for risk assets and bad for the dollar. However, if US macro data starts going from bad to recessionary, then the soft-landing narrative will fall. At the other end of the spectrum, if US data outperforms expectations by a large margin, this would put the chances of rate cuts into question. And we think that both scenarios would lead to higher market volatility. Especially given the currently suppressed levels and complacency of investors. On the FX side, investors are in the game of assigning a hierarchy to G10 central banks based on their likelihood of easing policy in 2024. The more rate cuts are priced in, the more the respective currency is expected to weaken going forward. The Fed and ECB have led the pack in this regard as of late.

Investors looking to confirm two assumptions. Looking into December, how likely is this risk rally to continue? To answer this question, we can once again highlight our three drivers of the November risk rally and simply ask: are these themes likely to continue? Because if central banks are done raising interest rates, if the US economy slows at a moderate level and inflation numbers continue coming down, the equity rally continues, and the dollar remains on the defensive. However, if either the assumption of (1) the soft landing or (2) central bank policy easing falls, risk assets will have a harder time climbing to new peaks at year end.

Global Macro

The view ahead

Two big weeks ahead. The good news for investors is that December will provide plenty of opportunity to answer key questions with a lot of data coming up. The next two weeks will be accompanied by the nonfarm payrolls report, CPI inflation and the FOMC meeting on the US side. In Europe, we are looking forward to UK GDP and labor market numbers and the ECB, BoE and SNB policy meetings. Looking beyond these two regions, rate decisions in both Canada and Australia will be key as well. While no change in policy is expected, forward guidance at the last meeting of the year has the potential to become market moving.

The 14-day look ahead. A more detailed analysis can be found in our weekly risk calendar.

Monday (04.12) – German export, US factory orders

Tuesday (05.12) – RBA interest rate decision, US ISM Services

Wednesday (06.12) – Australian GDP, Eurozone retail sales, BoC interest rate decision

Thursday (07.12) – Eurozone GDP

Friday (08.12) – US nonfarm payrolls

Monday (11.12) –

Tuesday (12.12) – UK labor report, ZEW sentiment, US inflation,

Wednesday (13.12) – UK GDP, US PPI, Fed interest rate decision

Thursday (14.12) – SNB, BoE and ECB rate decisions

Friday (15.12) – Flash PMIs for Eurozone, UK, US, ECB staff projections

All dates GMT

FX Views

Dollar bears hoping for a dovish Fed ahead

USD: Worst month in a year. As global bonds secured their best month since the financial crisis and global stocks their best month in three years, the US dollar posted its worst month in a year. The moves were driven by increased speculation the Federal Reserve and global peers have largely finished hiking interest rates and will start cutting next year. With US 2-year bond yields subsequently falling to their lowest level since the Northern Hemisphere’s summer, the dollar’s yield advantage is being eroded and investors are on the hunt for higher returns elsewhere. In fact, the USD is only up against 12% of 50 currencies globally over a 3-month period, compared to a share of almost 90% just five weeks ago. As we enter the festive period – the deterioration of the dollar may deepen as historically December is the worst month of the year for the world’s reserve currency. We note, the dollar index (DXY) remains 11% above its long-term mean and has clocked its longest daily streak above the 95.0 level since 2003. We think there is more scope for depreciation, but if recession risks rise, the dollar may enjoy a wave of safe haven demand in the interim.

EUR: Signs of a European bottoming are emerging. The euro’s volatility of late has mostly been a function of USD moves and Fed rate expectations. Earlier this week the euro hit a 3-month high against the US dollar above $1.10 on the back of dovish Fed comments spurred a renewed risk rally, before the pair recoiled on the back of a cooler than expected Eurozone inflation print. Core HICP rate fell to the lowest point since April 2022 on annual basis and turned negative on monthly basis – the largest monthly decline since January 2020. A continuation in the disinflationary trend pushes back against the ECB’s higher for longer rhetoric and increases the probability of a bottoming of the European business cycle. Markets are pricing in 13bps cut in the key policy rate as early as March while the cumulative rate cut bets increased to 110bps for the whole of 2024 (up from 100bps at the beginning of the week). Despite the recent dovish repricing, EUR/USD closed out the month up 2.9%, the biggest monthly gain since November 2022, and is on track for the fourth consecutive weekly gain.

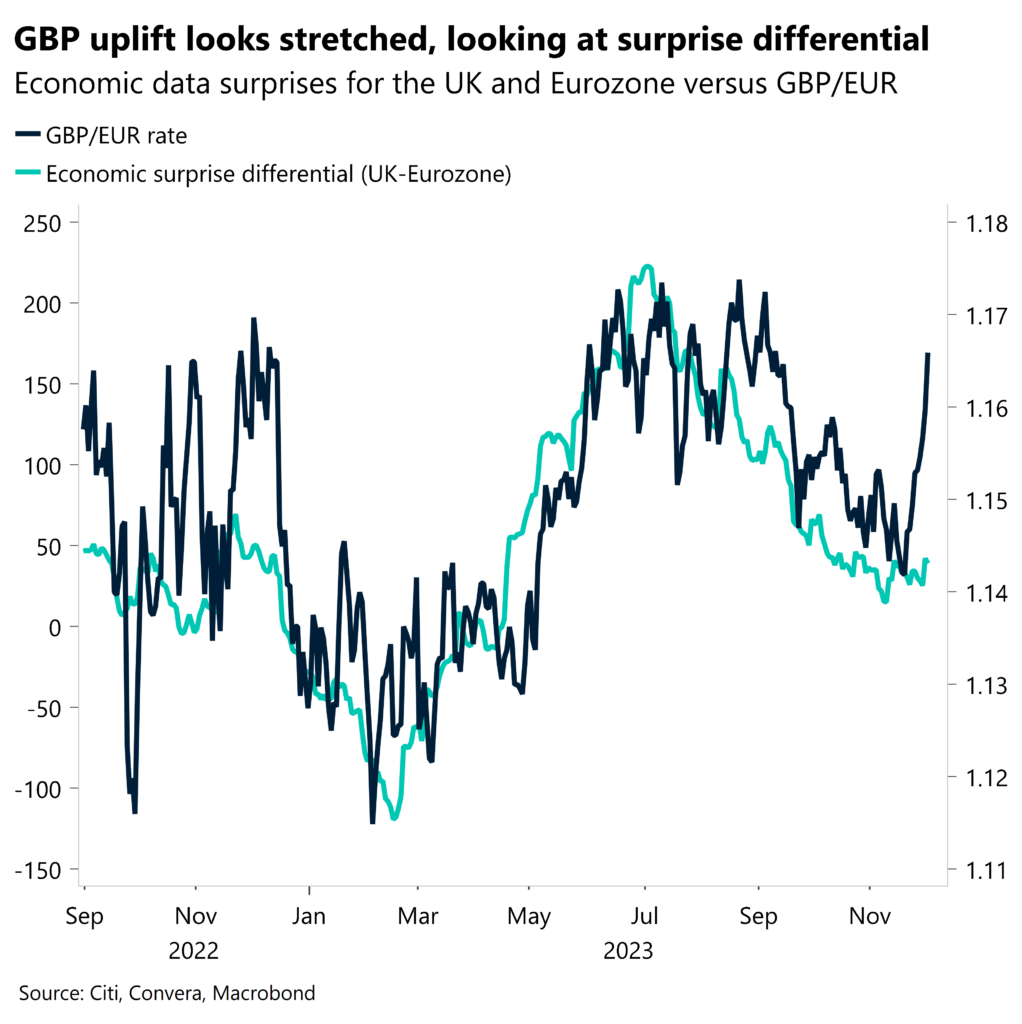

GBP: Energised by risk rally. The pound is on track for its fourth weekly rise in five against the US dollar despite a corrective pullback from almost 3-month highs above $1.27. GBP/USD also recorded its biggest monthly rise (+4%) in a year. A recent string of better-than-expected UK data and hawkish Bank of England comments have supported the UK currency, especially given markets are no longer pricing three full rate cuts by the BoE in 2024. However, given relatively stable swap and rate differentials, we still think the pound is largely reaping the rewards of the global risk rally more than anything else. This is evidenced by GBP/USD’s strong correlation with global equities and sterling’s depreciation against its riskier Antipodean and Central Eastern European peers of late. As expected via the overbought conditions on GBP/USD, we’ve already seen a retracement lower, but consolidating above both its 100- and 200-day moving averages puts a firmer base under the currency pair around the $1.25 threshold.

CHF: Strongest in almost four months. After hitting an 8-year low in the summer, USD/CHF recovered a total of 8% over ten consecutive weekly gains. But after topping out just above 0.92, the franc looks set to notch seven weekly gains out of nine to drag the pair back towards 0.87. Despite the risk rally of late, which would usually soften franc demand, falling US yields have weighed heavier on the dollar, sending the currency pair towards fresh 4-month lows. Although Swiss bond yields have also fallen, with the 10-year clocking a 6-month low this week, a patch of robust domestic data may have also helped the Swissy. The Swiss investors’ sentiment index turned higher, retail sales surprised sightly better and business morale was at a 7-month high in November. Thus, in a sign of broader strength, the franc’s over 1% gain against the euro this week, marks its fourth biggest weekly rise of the year and is increasing the likelihood that EUR/CHF will suffer its sixth successive yearly decline. In two weeks, the Swiss National Bank will deliver its final policy decision of the year.

CAD: Recovers to a 2-month high. The Canadian dollar strengthened towards the $1.35 level against the US dollar, marking a renewed two-month high amid expected oil supply pressures. A unanimous OPEC+ decision to reduce daily output by an additional million barrels offset economic data indicating a slowdown in the Canadian economy. Data this week unveiled that the Canadian GDP contracted by 1.1% in Q3 on annualized terms, a stark contrast to market expectations of a 0.2% expansion and a positive Q2 performance of 0.3%. The result underscored that higher interest rates from the Bank of Canada (BoC) are being transmitted to a greater extent to the Canadian economy, putting pressure on the central bank to adopt a dovish monetary stance. This aligned with a higher unemployment rate and slowing consumer inflation, prompting expectations in the markets for the BoC to initiate a policy rate cut as early as March 2024 with a 60% probability. Over 100bps loosening is already priced in for the whole of next year.

AUD: Hits 18-week high. The Australian dollar rose for three weeks in a row and hit an 18-week high this week thanks to the global risk rally supporting riskier currencies. It has struggled to extend its recovery against the US dollar over recent sessions though. Still, AUD/USD is tracking above its 100- and 200-day moving averages in a sign that a bullish trend is emerging, which falls in line with our positive bias on the Aussie going into 2024 given it is 15% undervalued compared to its long-term average. The Reserve Bank of Australia’s rate decision is due on Tuesday with no change to policy expected, but the AUD may be supported if the RBA retains its hawkish stance given upside inflation surprises of late which have seen markets price out rate cuts by the RBA next year.

CNY: Yuan hits 3-month highs. The Chinese yuan has extended its recovery against the US dollar this month, with CNY strengthening over 2%. USD/CNY broke below 7.15 and hit three-month lows. The move builds on its small gains in October amid a weaker greenback, strong PBoC fixing, and early signs of stabilization in China’s growth momentum. USD/CNY is consolidating firmly below its 50- and 100-day moving averages. However, we think general dollar weakness has been the primary driver of the rally as other domestic supports remain tentative. Key macro data has shown a mixed recovery and policy easing is still gradual. Meanwhile, seasonal USD/CNY outflows are emerging into year-end. As such, the CNY rally might stall over coming weeks absent clear upside surprises in the growth outlook. The yuan should take further cues from broad dollar trends and risk sentiment, while volatile daily fixes by the PBOC may trigger some volatility. Key upcoming data includes Caixin Services PMI and trade balance.

JPY: Yen bears still have the upper hand. The yen hit a 2-month high against the US dollar this week, dragging USD/JPY under ¥147, but the pair failed to gain momentum and pulled back above ¥148 as month-end flows supported the dollar. The currency pair remains stuck in a relatively wide ¥145-¥152 range as optimism over a soft landing in the US economy limits the downside. We think yen bears still have the upper hand as long as recession fears remain at bay. Meanwhile, the Bank of Japan looks set to lag global tightening until 2024. The upcoming US ISM and payrolls will be key for dollar/yen direction. In Japan, any hawkish lean from dovish board members could boost speculation for a swifter normalization path.