Written by Convera’s Market Insights team

Higher dollar going into month-end

Boris Kovacevic – Global Macro Strategist

The US dollar inched marginally higher in yesterday’s trading session due to favourable month-end flows, cautious positioning ahead of the Fed and BoJ rate decisions and weaker macro data out of Europe. The Greenback pushed higher against most majors such as the euro, pound, and yen but suffered losses against the Swiss franc and Canadian dollar.

However, the more significant development happened on equity markets as the slide of high valuation tech stocks continued. The Nasdaq shed another 1.7% and fell to its lowest level since early June, down around 9.4% from its peak. This pushed implied volatility rates higher and most likely contributed to yesterday’s risk off sentiment on FX markets, evident in the depreciation of most emerging market currencies.

Markets have already positioned and committed to the Fed pivot coming in September, meaning that any deviation from that assumption would lead to unfavourable position unwinding. Yesterday’s macro data from the US was neutral to slightly positive for the Greenback as job openings remained largely unchanged and consumer confidence rose. The gauge from the Conference Board increased from 97.8 in June to 100.3 in July. Optimism remained muted, though, as the present conditions index fell to the lowest in more than three years. Consumers are gloomy and are in need of lower rates, still. This is evident in the quits rate as well, which remained unchanged at its post-pandemic low of 2.1%.

Today’s risk events include the ADP employment report and employment cost index with the highlight being the FOMC rate decision afterwards. Markets are broadly expecting Jerome Powell to confirm the desire to ease policy in September as the disinflation process continued and the labor markets starts to ease.

Pound lags G10 peers ahead of BoE

Ruta Prieskienyte – Lead FX Strategist

The British pound fell to a three-week low of $1.283 amid a brewing risk-off sentiment in anticipation of the Bank of England’s upcoming monetary policy decision on August 1st.

The market’s priced-in probability, reflected in the OIS curve, remained stable at 57%, indicating fragile conviction that the BoE will lower the key interest rate by 25bps to 5% from a 16-year high of 5.25%. The decision remains uncertain given the surprisingly robust 0.4% GDP growth in May and persistently high services inflation of 5.7%. Regardless of the outcome, we expect heightened volatility across GBP crosses in the aftermath of the event, given the market’s long positioning.

Looking ahead, the market is not anticipating a persistent increase in volatility in today’s trading session as the overnight GBP/USD ATM option volatility remains broadly in line with the July average. If Powell gives markets assurance over a September rate cut, the pound may appreciate somewhat. However, the extent is likely to be limited, given that a Q3 Fed cut is fully priced in and the BoE’s August decision remains a much more pressing and finely balanced matter.

Euro range bound ahead of Fed

Ruta Prieskienyte – Lead FX Strategist

The euro briefly plunged below the $1.08 mark for the first time in over three weeks amid a mixed bag of macroeconomic reports from the Eurozone. European equity markets closed the day in the green as investors digested fresh earnings reports, while the bond market remained bid. Front-end German bond yields declined for the sixth consecutive session to touch a near seven-month low at 2.54%.

The Eurozone economy expanded at a faster-than-expected 0.3% in Q2, according to preliminary figures, led by growth in France, Italy, and Spain. Meanwhile, Germany unexpectedly contracted by 0.1% quarter-on-quarter, compared to forecasts of a 0.1% gain. There was a notable decline in investments in equipment and buildings, as the industrial sector continues to be particularly strained by high interest rates.

Inflation in Spain eased more than estimated to 2.8% year-on-year, while inflation in Germany unexpectedly edged up to 2.3% year-on-year, versus expectations of a 2.2% rise. Price growth accelerated for food and steadied at 3.9% for services, while the cost of energy declined at a slower pace. Compared to the previous month, the CPI edged up 0.3%, the most in three months. Investors continue to price in another 25bps cut in borrowing costs by the ECB in September.

Despite the data dump, the one-week EUR/USD realised volatility remains near 2024 lows as cautiousness prevails and markets gear up for this week’s Fed and BoE meetings. The Euro Index declined by 0.16% for a second consecutive session to a four-week low.

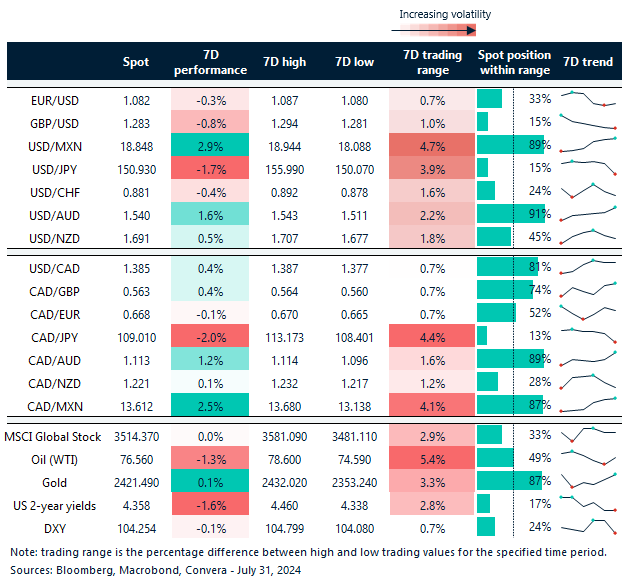

GBP, CAD retreat ahead of Fed, BoE

Table: 7-day currency trends and trading ranges

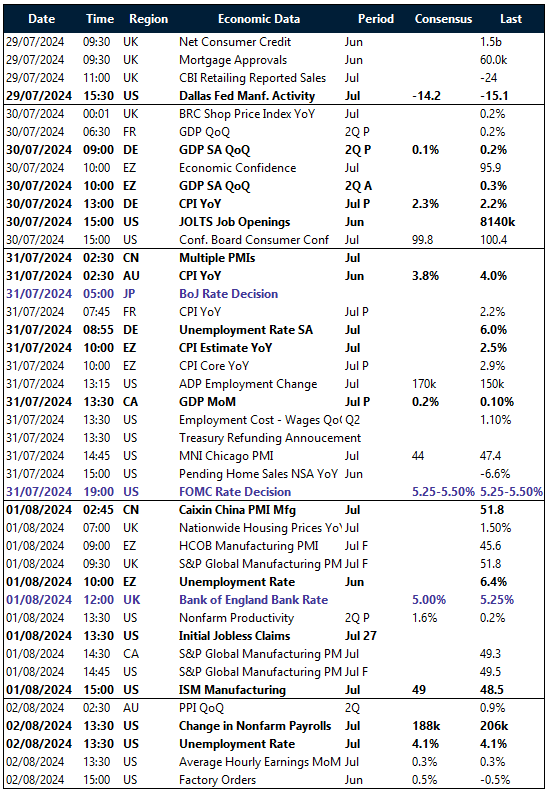

Key global risk events

Calendar: July 29-August 02

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.