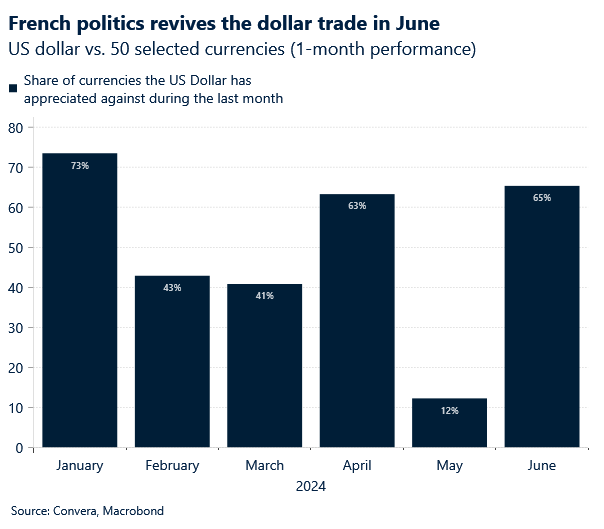

Dollar’s June revival as PMI top estimates

Boris Kovacevic – Global Macro Strategist

The Greenback gained momentum just before the weekend as the patch of regional purchasing manager indicators supported the thesis of the United States outperforming its developed market peers. The US Dollar Index (DXY) rose for a third consecutive week and has extended its year-to-date gains to 4.5%. The barometer for the strength of the reserve currency is now trading just 0.6% shy of its 2024 high reached around the middle of April. The US dollar has risen against 65% of the world’s currencies in June and has more than made up the losses incurred in May.

The main catalyst for the current mini leg higher in June had been the fallout of the European parliamentary election and French president Emmanuel Macron calling for a surprise general election at the end of the month. US inflation surprising to the downside on three different occasions two weeks ago and investors raising their expectations for Fed cuts in 2024 from one to two limited the dollar’s upward potential. Still, the PMIs from Europe and the US supported the Greenback going into the weekend. The US composite index rose to 54.6 in June and reached its highest level since April 2022. A detailed look reveals more good news. The employment and new orders sub-indicators jumped to 51.7 and 53.4 as the price component moderated. Friday’s data undermines the thesis of a slowing economy but stands in contrast to the recent weakening of consumer spending and labour market data.

We will continue to focus on the data to gauge how much room the Fed will have to cut rates this year. Against this backdrop, this week’s PCE report will be highly crucial. Incorporating the newest data into a simple regression model on the Fed’s preferred price gauge (core PCE) gives us a monthly growth rate of 0.1%, which would be seen as further progress to reaching the 2% target. This could put the annual headline number on track for a fall from 2.7% to 2.6% in May.

European recovery stalls

Boris Kovacevic – Global Macro Strategist

The euro fell for a third straight week after macro data on Friday highlighted weakening momentum of Europe’s economic recovery. Especially the divergence with the better-than-expected US data took investors by surprise, which added to the already downbeat sentiment surrounding the common currency. EUR/USD is flirting with the $1.07 level but considering the drastic movement in the options market, the 2% fall since Macron called the snap election does appear to be relatively minor.

We see this as a combination of two factors. The euro decoupled from implied volatility rates at the beginning of 2023 and has been trading sideways despite volatility rates continuing to fall. This means that the euro is not as prone to decline as volatility rates rise again. Secondly, given the disinflationary forces in the US and markets expecting the Fed to cut interest rates this year, traders are hesitating to put too much weight into the Greenback. The short-euro trade has therefore been expressed better via other currency pairs like EUR/CHF, EUR/NOK, or EUR/SEK.

Going to the macro data from Friday, the preliminary HCOB Eurozone composite PMI edged down to 50.8, sharply missing the market consensus of 52.5. The print marked a fourth consecutive month of expansion but was the lowest reading since March. The weakness mainly stems from the deteriorating conditions in the manufacturing sectors, which fell to a 6-month low. Services sector too showed signs of faltering as the flash PMIs fell to 52.6 in June, a fifth month of growth, although the lowest for three months. At a regional level, France and Germany reported a fall in their composite indices to 48.2 and 50.6, respectively. As for the former, output expectations for the next twelve months have weakened, as companies expressed uncertainty about the upcoming election results, as well as more broad geopolitical risks.

Investors are now turning their attention to the confidence indicators from the Ifo, GfK and DGECFIN institutes to gauge how the second quarter is getting underway. We don’t expect a drastic change with the German business and consumer confidence numbers remaining largely unchanged on Monday and Wednesday. EUR/USD will therefore take its impulses from the US PCE report on Friday.

Pound trading lower after trifecta of misses

Boris Kovacevic – Global Macro Strategist

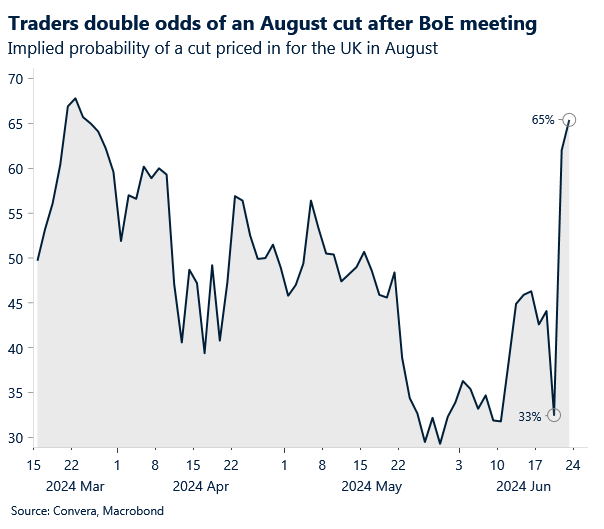

Inflation in the United Kingdom has fallen back to the 2% target of the Bank of England for the first time in almost three years, strengthening the case for starting the easing cycle this summer. Policy makers voted to leave interest rates unchanged at 5.25% at last week’s meeting but recent comments from British central bankers suggest that the sentiment towards a cut is growing. While services, rent and wage inflation remains elevated and therefore a source of uncertainty, the fact that tight monetary policy is working its way through the economy will most likely be enough of a reason to ease policy this year. The probability of an August cut rose from around 30% to 65% following the CPI report, the BoE decision and PMI numbers.

The UK composite PMI fell for a second consecutive month from 53 to 51.7 in June, marking its weakest growth rate this year. The back up in momentum was mainly caused by slower services growth, which fell from a one-year high in April (55.0) to a seven-month low in June (51.2). The recent labour market report also showed the unemployment rate rising to 4.4% in April, reaching its highest level since September 2021.

This trifecta of negative surprises led GBP/EUR to its first weekly decline since early May as the currency pair fell from its one-and-a-half year high at €1.19 to now trading at €1.1820. The European risk premium receded a bit last week as investors continue to digest the implications of the upcoming French elections. GBP/USD fell for a third straight week and is now trading in the mid $1.26 region after having climbed to $1.2850 two weeks ago.

JPY under renewed selling pressure

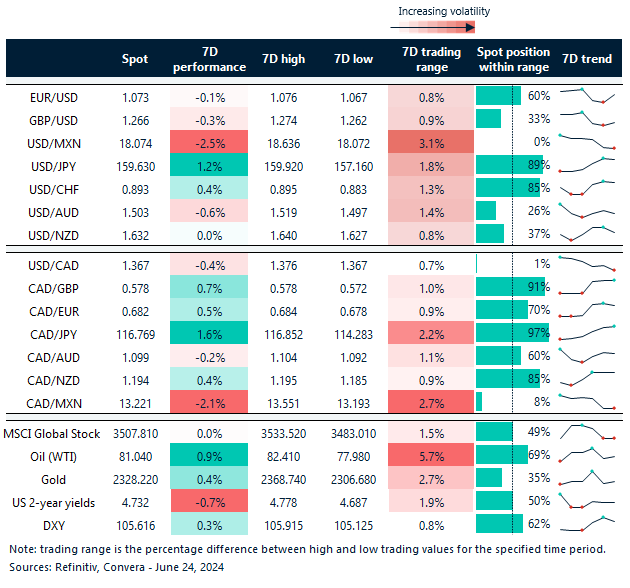

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: June 24-28

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.