Inflation trumps the Fed (and jobs data)

Boris Kovacevic – Global Macro Strategist

A strong non-farm payrolls report on Friday and French president Emmanuel Macron announcing a snap election on Monday lead to some volatile trading on FX markets early on this week with the euro suffering the most from a flight to safe-haven currencies. Bond yields across the world jumped due to the US economy seemingly having remained resilient and investors pricing in political risk premia into European sovereigns.

This all changed during yesterday’s session when US inflation surprised all expectations to the downside, setting off a capital rotation back into risk assets like the euro, pound, and equities. Not even the hawkish upside revision of the Fed’s inflation and rates projection was enough to make up for the weak CPI report. We have come a full circle after the release of the labor market report with EUR/USD and long-dated Treasury yields almost exactly at the levels they had been on Friday.

US inflation stagnated for the first time in almost two years on a monthly basis, printing a growth rate of 0%. The annual headline number fell from 3.4% to 3.3% in May with core inflation declining to 3.4% and therefore setting a three-year low. The 3- and 6-month annualized rates declined as well in a sign that the disinflationary process has continued. The 2-year US Treasury yield fell from 4.83% to below 4.7% in the first hour after the release and just slightly bounced back after the FOMC meeting later yesterday. EUR/USD pushed higher by around 0.75% beyond the $1.08 level but gave up some of the gains in the later US session.

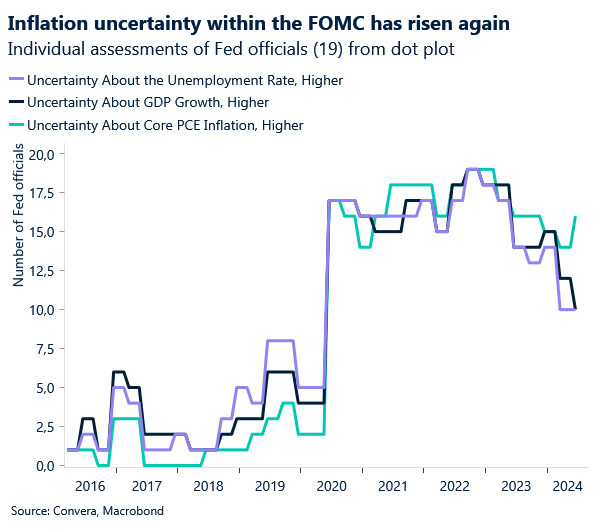

The CPI report overshadowed the Fed’s rate decision looking purely at the market’s reaction to both events. However, the FOMC meeting was not as lacklustre as economists had expected. The benchmark policy rate remained unchanged at 5.25% but policy makers revised up their rates and inflation projection with the median dot-plot showing just one instead of three cuts for 2024. The FOMC now sees core PCE inflation at 2.8% in 2025 (vs. 2.6%) and the unemployment rate at 4.2% (vs. 4.1%). The growth outlook remained the same. Without the context of the CPI report, this rate decision would have been seen as hawkish. However, investors seem to see the Fed’s rate projection as already priced in and almost outdated given the inflation print for May. This point is highlighted by markets still expecting the Fed to cut rates in September and December this year.

The press conference from Jerome Powell added a bit of hawkishness into the mix and cut the US dollars daily loss by about a third. The Greenback is still likely to lose all its gains made last week after the strong US labor market report. We are now focusing on the PPI number coming out today to see if the disinflation is confirmed by a second data point.

Sterling rides the risk wave

George Vessey – Lead FX Strategist

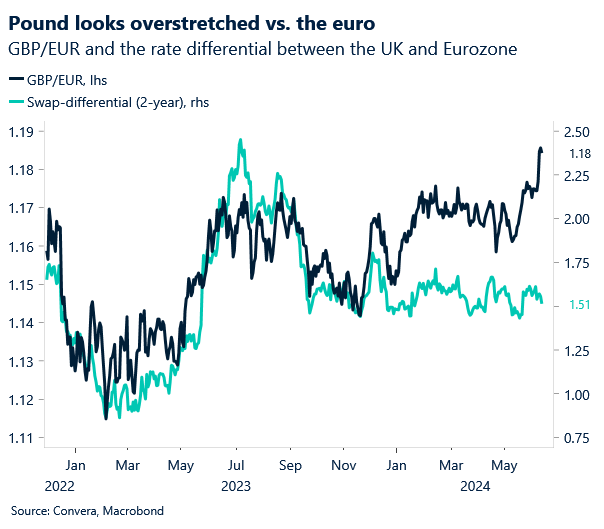

The British pound rose to a 3-month high against the US dollar following the softer US CPI print. A bout of risk-taking swept across financial markets in anticipation of more Fed rate cuts on the horizon. GBP/USD is flirting with its 200-week moving average, which was a strong resistance level back in March when the pair fell over 4% in six weeks after failing to hold above it. But Fed rate cut bets were being dialled back at that point. Now they are being dialled up. A convincing close above $1.2857 (200-day MA) could open the door to $1.30 soon.

Against the euro, sterling hit its highest level since August 2022 amidst the political risk emanating from France. Further upside cannot be ruled out as traders add to euro bearish bets against the pound over the next month which covers election risk in the UK and France. One-month risk reversals in EUR/GBP rallied to 33 basis points, puts over calls, the most since October 2019. Ultimately, this implies option traders are preparing more for the pound to rise, instead of fall, against the euro over the next month.

We take a cautious stance on this though. Whilst external factors have been more influential in moving GBP than domestic data and UK election developments, we think markets are underpricing the chance of a Bank of England (BoE) rate cut this summer. The pound may lose some of its recent momentum if UK services inflation comes in cooler than expected next Wednesday, as it would raise the probability of a BoE cut in August and bring rates differentials back to the fore, especially when it comes to GBP/EUR.

Euro recovers; macro overshadows politics

George Vessey – Lead FX Strategist

EUR/USD jumped around 1% after the US inflation print yesterday, more than recouping the losses suffered post the EU elections last weekend. European politics only matters when it develops into Black Swan events like during the debt crisis. Otherwise, macro remains key. This mantra has held up so far with the US non-farm payrolls and CPI reports overshadowing any reaction to the European and snap French elections.

Our note to clients on Tuesday: We think that markets did a good job adjusting to the composition of the new European parliament. Now that the initial re-pricing process is over, the medium-term implication for the euro will likely be more muted as the Fed and US macro continue to set the currency’s direction. True, the risk premium due to the upcoming election in France could cap any meaningful gains for the euro. However, US macro will continue to be the primary driver of price action. If the US economy unexpectedly slows beyond what is priced in and the Fed has to cut interest rates sooner than anticipated, European politics will play second fiddle to events unfolding in the US.

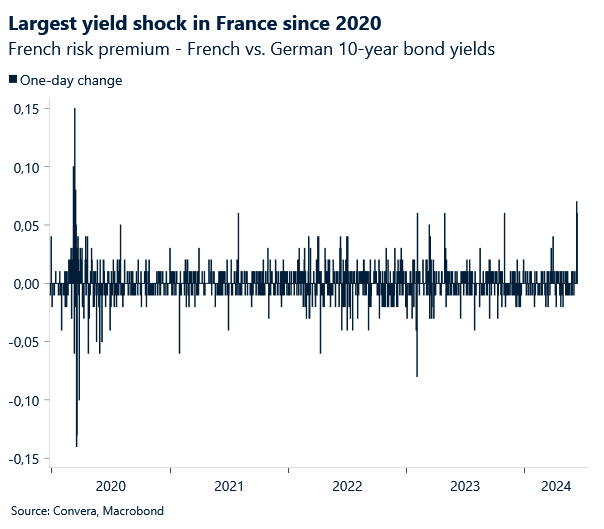

This doesn’t mean we’re ignoring the political situation across Europe. France’s longer-dated bonds will underperform their German peers in the coming weeks as traders move to incorporate a political risk premium ahead of the first round of French parliamentary elections on 30 June. And we expect markets to take notice of opinion polls – where larger leads for Le Pen’s party could further rock French bonds and will be seen as a euro negative.

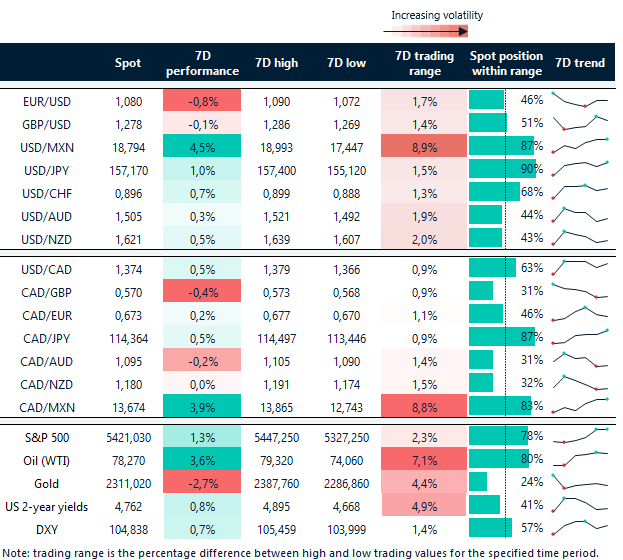

EUR/USD at $1.08 after CPI and Fed

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: June 10-14

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.