Written by Convera’s Market Insights team

ADP report does not matter, until it does

The US 10-year government bond yield is currently the most watched market indicator in the world. While fears of oil prices pushing beyond $100 per barrel and inflation not returning to the Fed’s 2% target have not eased, it seems that the supply side is the primary driver of the move higher in yields. Although the looming fear of a temporary shutdown has been eased, or at least postponed into November, faced with a hawkish Federal Reserve, the Fed’s QT program, and heavy auction sales of US treasuries, investors continued their relentless selling of US government bonds this week. However, in addition to the supply side, strong macro data has been supporting the re-pricing of yields as economists pushed out their expectations for an imminent US recession.

The US 10-year yield reached the highest level since 2007 at 4.88% on Wednesday and most government bonds across the world have followed suit. However, while yesterday’s data releases have been mixed with the ADP jobs growth disappointing (89k vs. 180k jobs created) and the ISM PMI and especially factory orders (1.2% vs. -2.1%) surprising to the upside, investors put more weight on the labour market data. While the private report from ADP has been negatively correlated with the actual job growth reported by the US bureau of labor, and usually does not move markets, it did yesterday.

US and German 10-year yields fell from multi-year highs at 4.88% and 3.02% to 4.77% and 2.92%. The fall in interest rates gave risk assets like equities some relief with the S&P500 and Nasdaq both rising by more than 1% intra-day. The US Dollar Index fell by 0.6% from its 10-month high at 107.50 and is currently up around 7% from the July low. Now, all attention turns to the release of weekly initial jobless claims later today before the release of the non-farm payrolls report tomorrow.

Boris Kovacevic – Global Macro Strategist

Yield and oil slip, euro back above $1.05

The euro has mostly been overpowered by the US dollar in recent weeks as the global increase in government bond yields overshadowed any new developments in Europe. We are currently still in the regime, in which investors wait on the bottoming of the Eurozone economy with economic data continuing to show weakness in activity. And while we are past the point where every economic data release is weakening or disappointing expectations, a majority of indicators still are. The euro has still been able to push back a bit against the dollar in yesterday’s trading as investors stopped their relentless selling of government bonds, pausing the move higher in yields.

Yesterday’s news flow has been mixed. Lagged (hard) data is coming in weaker than expected, highlighting the Eurozone’s difficulty returning to economic growth. Producer price inflation continued its descent into negative territory, falling by the most on record at -11.5%. Retail sales for the month of August fell -1.2% and have now been negative on a year-on-year basis for 11 consecutive months. At the same time, today’s German export data showed how net trade most likely pulled GDP lower once again in Q3, as the trade surplus narrowed to €16.6B in August, from €17.7B the month prior.

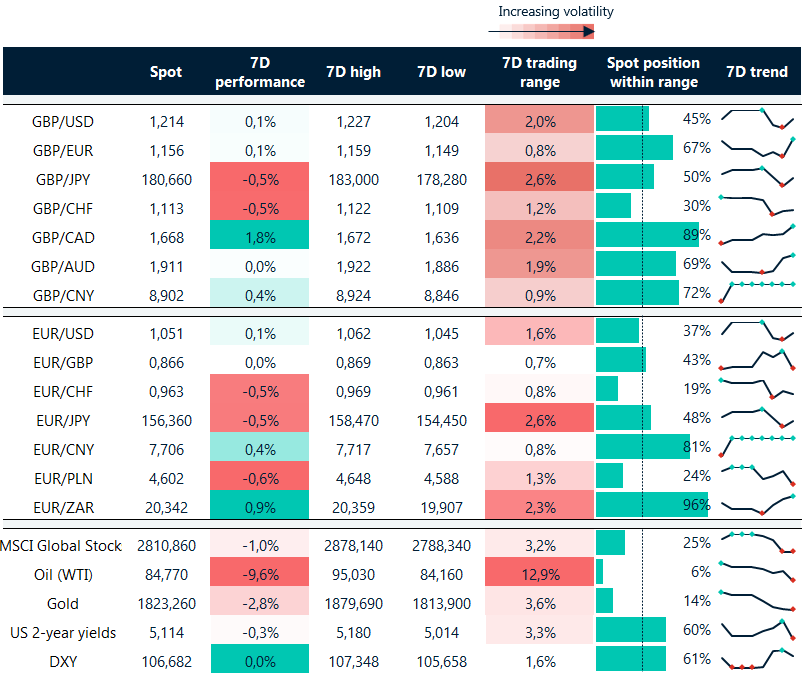

The euro, currently sitting near $1.05, has also benefited from oil prices being down more than 10% in a week, as investors think about the implications of higher yields on economic growth and demand for commodities. Christine Lagarde once again confirmed her stance that the ECB has reached the peak in interest rates and that they will stay in restrictive territory for as long as necessary. However, as we have pointed out, a sustained path beyond the $1.08 level can only be engineered by higher European growth rates and falling yields in the US.

Boris Kovacevic – Global Macro Strategist

Correlation with euro could prove dicey for pound

The pound bounced from the low $1.20 region towards $1.22 against the US dollar yesterday, in line with a retreat in US Treasury yields and oil prices and a bullish day for equities. The sharp move has resulted in GBP/USD unwinding the oversold intraday and daily studies. We’re wary of the pound’s strong positive correlation with the euro though, because if EUR/USD slides towards parity again, this would likely bring sub-$1.20 levels into focus for GBP/USD.

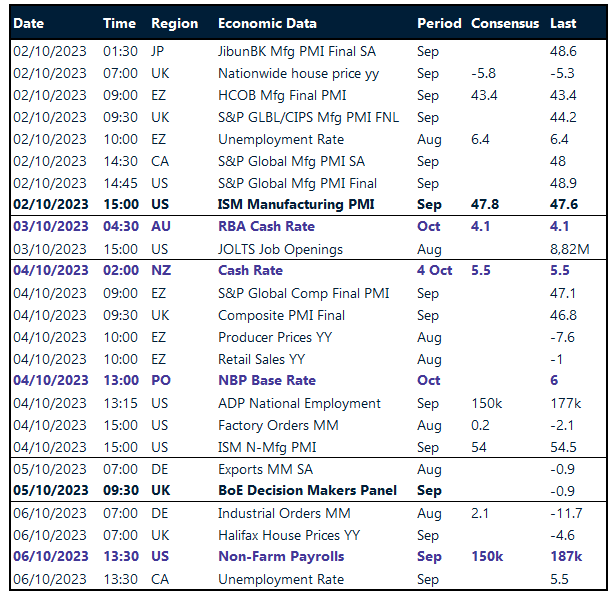

Sterling received a much-needed reprieve yesterday with the help of a correction in bond markets. The key now is whether these reversals hold. The pound also jumped on the news that UK business activity was less subdued than initially feared in September, with the final reading of services PMI upgraded to 49.3 from the preliminary 47.2 that shocked investors last month and influenced the Bank of England’s (BoE) decision to keep interest rates unchanged, which hurt sterling. Money markets are now pricing a 50% chance of another rate hike by the BoE this year, up from 22% just a few days ago. Today, the BoE’s Decision Makers Panel survey will be watched closely as it might guide the BoE’s November policy decision.

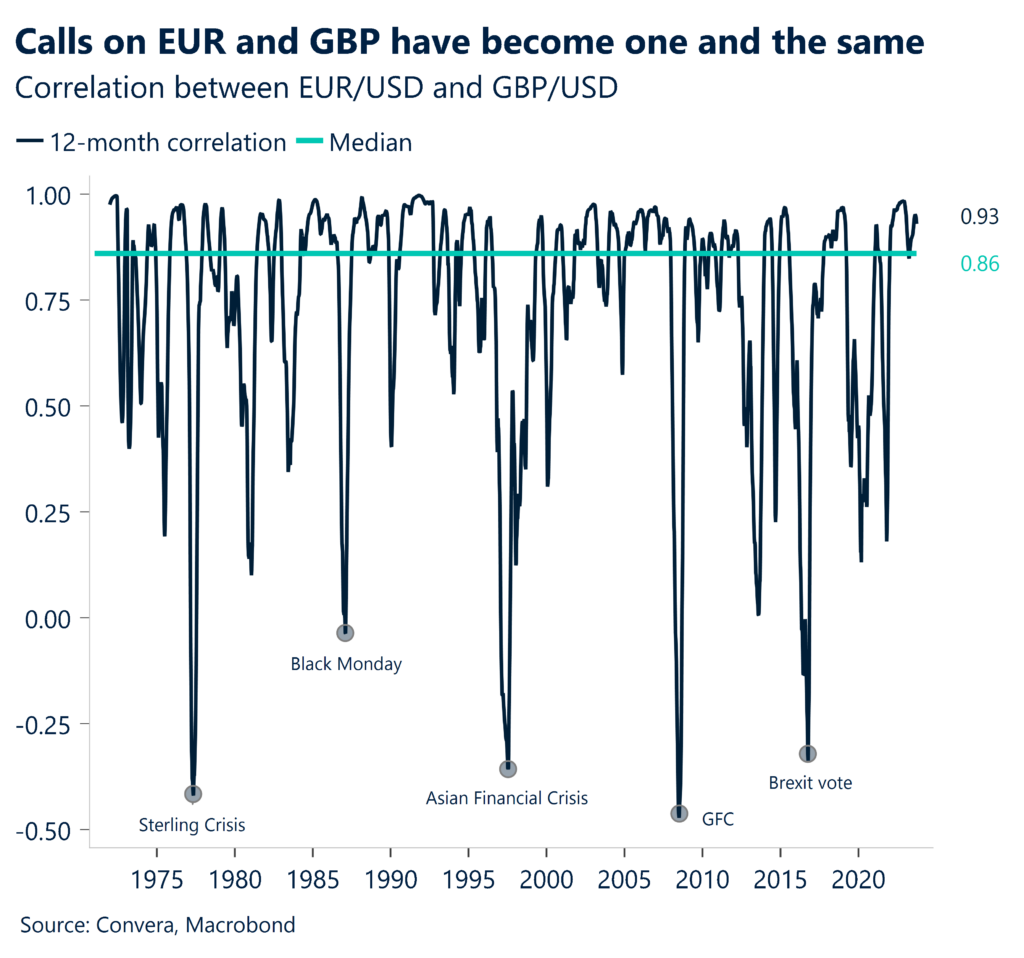

The multitude of headwinds facing the euro is a concern though because the 12-month correlation between EUR/USD and GBP/USD is 0.93, comfortably higher than the historic median of 0.86. Although oil prices have slumped heavily over recent days, if they resume their ascent and climb towards $100 per barrel as some analysts are hinting at, this will hurt the Eurozone economy and the euro. Moreover, renewed concerns about Italy’s fiscal position mean headwinds for the euro are getting stronger. These are two of many factors increasing the risk of EUR/USD falling further in the short-term, which in turn could drag GBP/USD lower as well.

George Vessey – Lead FX Strategist

Oil prices down almost 10%

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: October 2-6

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.