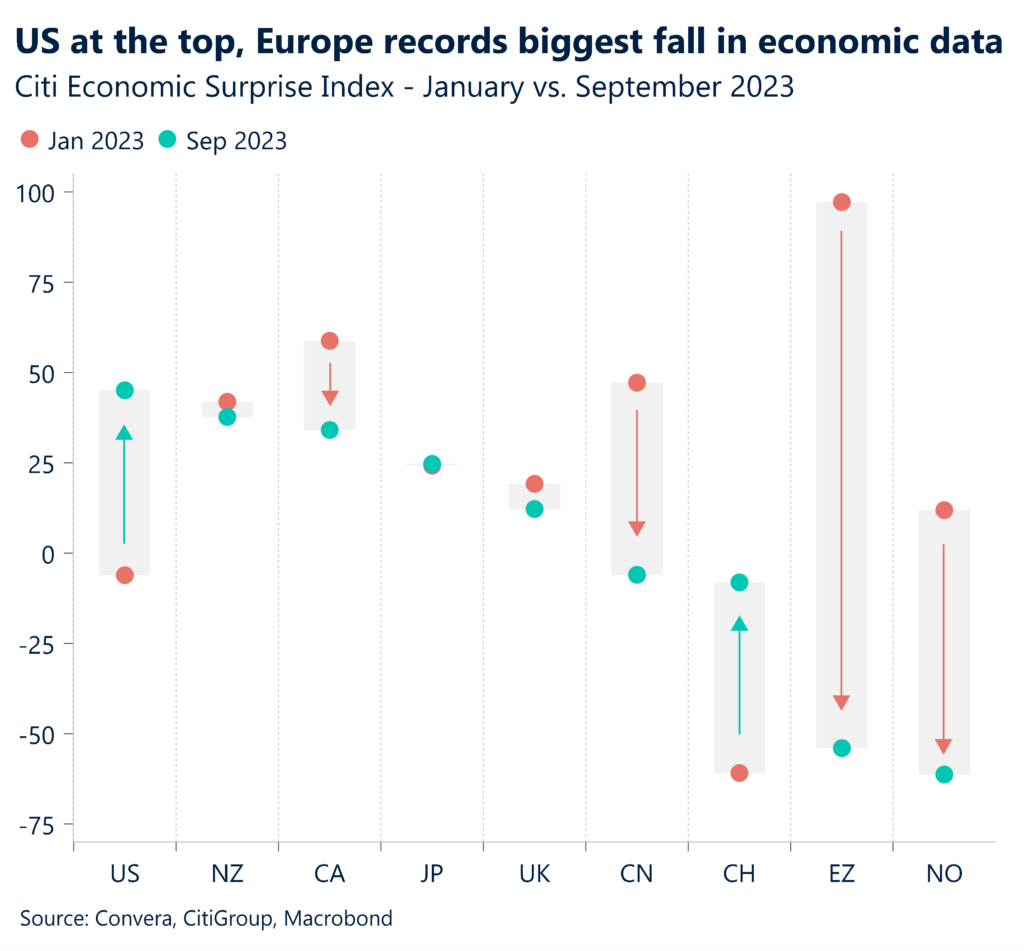

Global overview

The USD hit new highs after a stronger US PMI number. The Aussie was the hardest hit. Today, all eyes are on the USD/JPY as it nears 1990 highs. The RBA is also due.

US continues to outperform

The US dollar surged to new highs overnight after a better-than-expected manufacturing PMI number continued to show the US economy’s ongoing outperformance compared with other economies.

While the September manufacturing number remained below the make-or-break level of 50, the 49.0 result was well above the 47.8 expected.

The USD index hit new 10-month highs.

The Australian dollar was the hardest hit with the AUD/USD down 1.2%. The EUR/USD and GBP/USD both fell 0.9%.

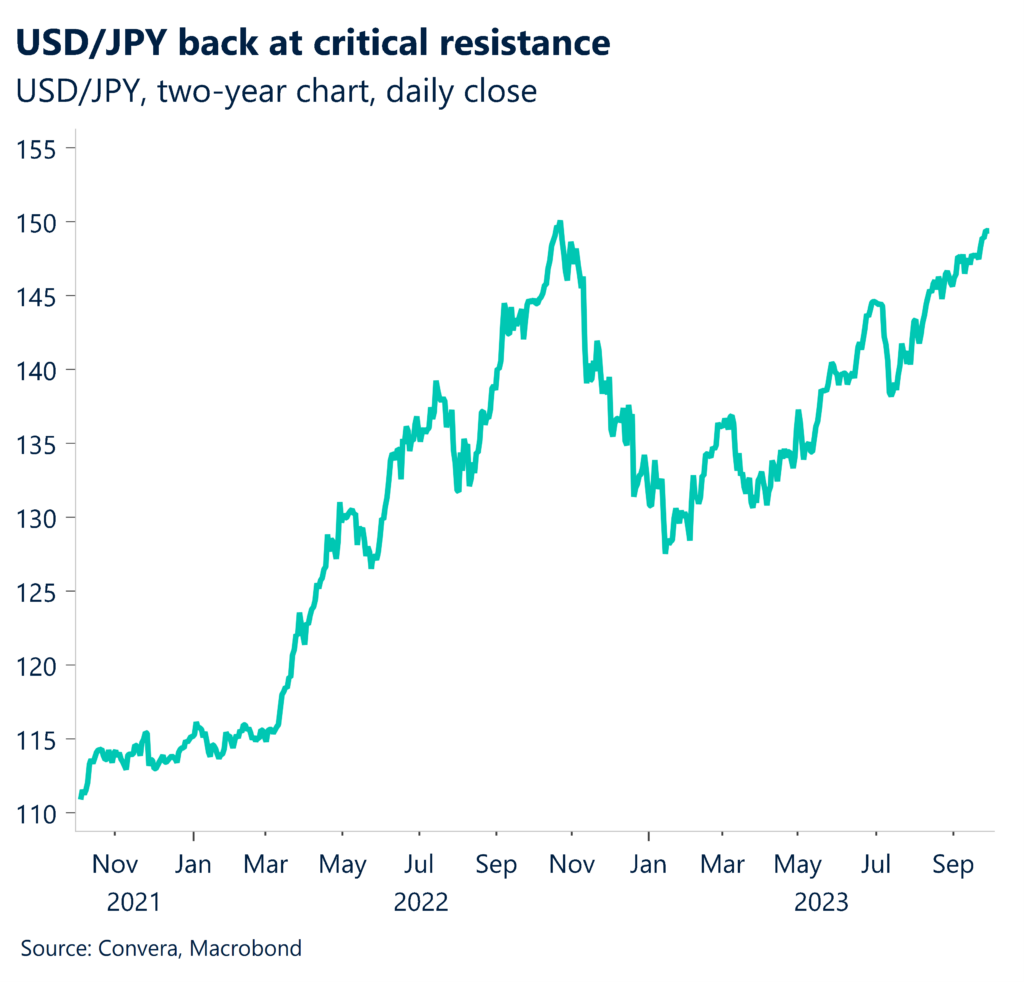

USDJPY at key level

The USD/JPY closed at 149.85 overnight – its second highest close since 1990. The ongoing strength in the US dollar – and the Bank of Japan’s recent signals that it is not willing to begin to raise rates – have contributed to the USD/JPY’s 14.6% gain since the start of the year.

Overall, USDJPY upside might be restricted for the time being, especially given intervention risks above 150.

We expect there will be limited tolerance from Japanese authorities above this level – the next phase in this process will involve “rate checks” by the BoJ.

Over the longer term, while US and Japanese policy remains at polar opposites, a significant break above the key 150 level cannot be ruled out.

RBA on hold…for now

The Reserve bank of Australia is due at 2.30pm AEDT. The RBA looks likely to announce that the cash rate will remain steady. Although Michele Bullock, the new RBA Governor, will preside over this board meeting, we do not anticipate any significant changes in communication, either in terms of substance or manner.

We anticipate it will once more signal a modest tightening stance and reiterate that more policy tightening “may” be necessary, pending new data and the development of risks.

However, at the November meeting, given that September-quarter CPI inflation data will be available, and the continued identification of upside risks relating to the RBA’s current near-term inflation outlook, we view a 25bp increase in November as somewhat more likely than not.

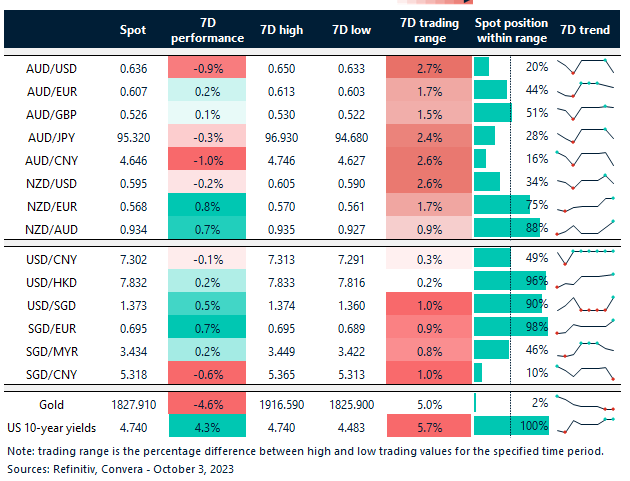

USD hits new highs

Table: seven-day rolling currency trends and trading ranges

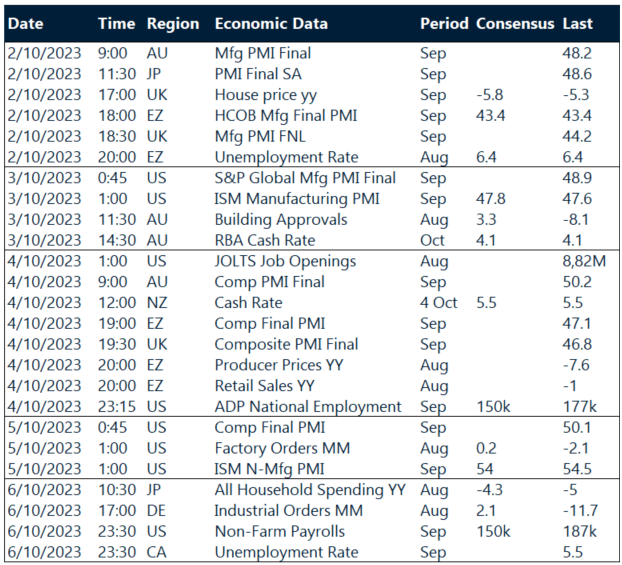

Key global risk events

Calendar: 2 – 6 October

All times AEST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.