Greenback gains across Asia

The US dollar started the new week stronger across Asia as growing concern around the Iran war and its impact on global energy markets weighed on sentiment.

The US dollar index is only 0.3% away from hitting its highest level since last May, supported by safe-haven flows and the US’s status as a major energy exporter.

Crude oil jumped further on Monday morning, rising more than 2.0%, with WTI crude opening at USD102.60 per barrel and Brent crude opening at USD114.50.

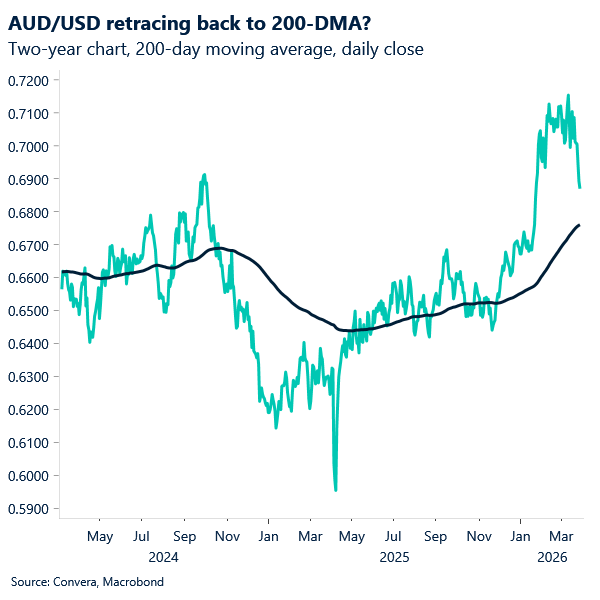

The AUD and NZD both started Monday lower, adding to last week’s 2.3% weekly loss in AUD/USD and 1.5% weekly loss in NZD/USD.

USD/SGD was higher in early Monday trading after last week’s 0.5% gain.

Chinese yuan weaker even as China’s profit engine fires up

China’s industrial profits jumped 15.2% year on year in January and February, a sharp acceleration from the modest 0.6% gain recorded across all of 2025. Makers of computers and electronic equipment led the charge, posting the fastest profit growth.

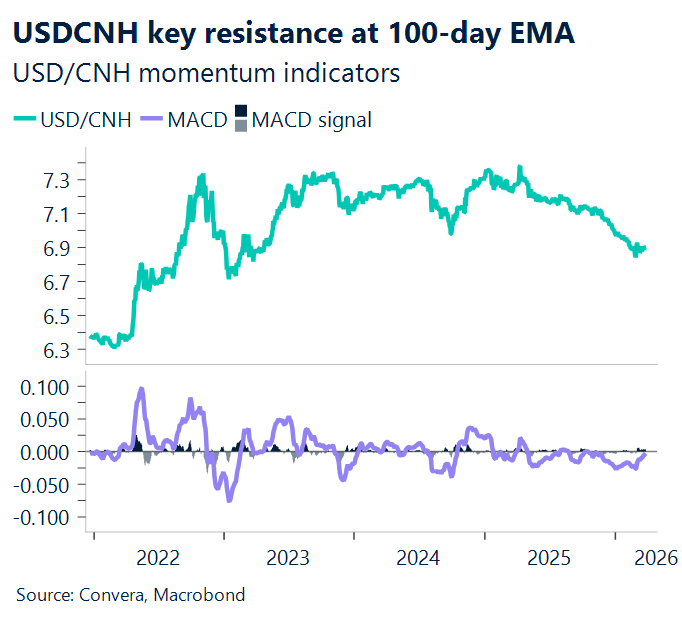

Still, rising input costs are squeezing business margins, and the economic fallout from Middle East tensions could emerge in the coming months. Watch for potential moves in USD/CNH as these crosscurrents play out.

Offshore, USD/CNH has climbed more than 1% from its late February low of 6.8267, set on 26 February. The next key resistance is the 100-day EMA at 6.9665. Recent price action suggests the dollar may remain firm in the short term if incoming data continues to favour the US side of the story.

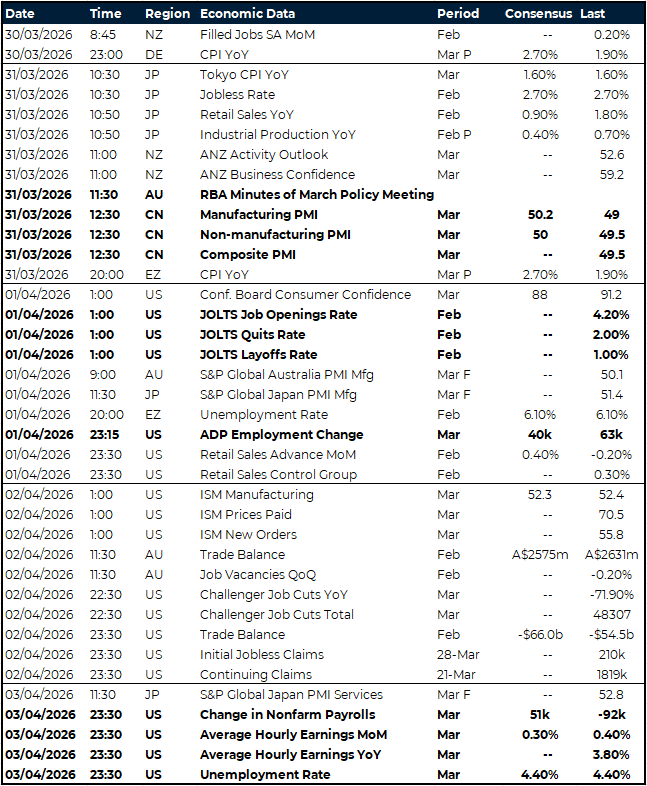

RBA minutes, US jobs report in focus

A holiday-shortened week brings a dense calendar focused on inflation and labour market signals. Monday sees German CPI (prior: 1.9% y/y), which will help guide the euro’s direction.

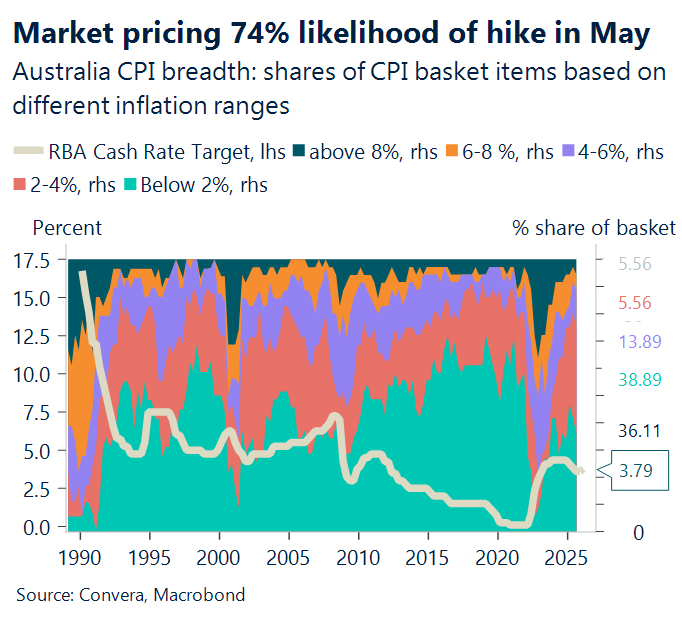

Tuesday’s data spotlight includes Tokyo core CPI, Japanese industrial production and China’s PMIs, all key barometers for regional growth sentiment. The RBA meeting minutes may clarify the domestic policy outlook, while UK Q4 GDP is forecast at 1.0% y/y (prior: 1.0%), and UK business investment is expected to fall 2.7% q/q.

Eurozone CPI (prior: 1.9% y/y) and core CPI (prior: 2.4% y/y) headline European inflation releases, with German and French data also due. Wednesday’s focus shifts to US JOLTS job openings, ADP employment and consumer confidence, while Australian building approvals and Japanese Tankan surveys offer further insight.

Thursday features Australia’s trade balance and US ISM manufacturing (forecast: 52.4, prior: 52.3), alongside weekly jobless claims. Friday is marked by Good Friday market closures, but crucial US labour data will still be released, including nonfarm payrolls (prior: -92k, expected: 51k), the unemployment rate (prior: 4.4%, expected: 4.4%) and average hourly earnings. These releases are likely to increase volatility in thin market conditions.

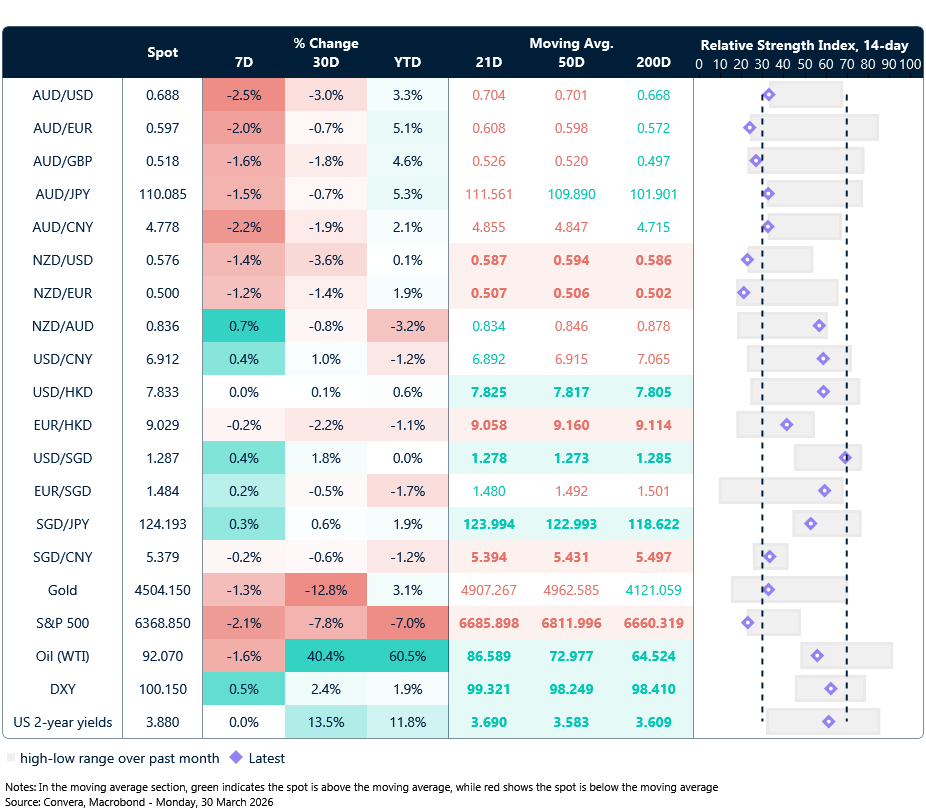

USD nears May highs

Table: seven-day rolling currency trends and trading ranges

Key global risk events

Calendar: 30 March – 3 April

All times AEDT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.