Written by Steven Dooley and Shier Lee Lim

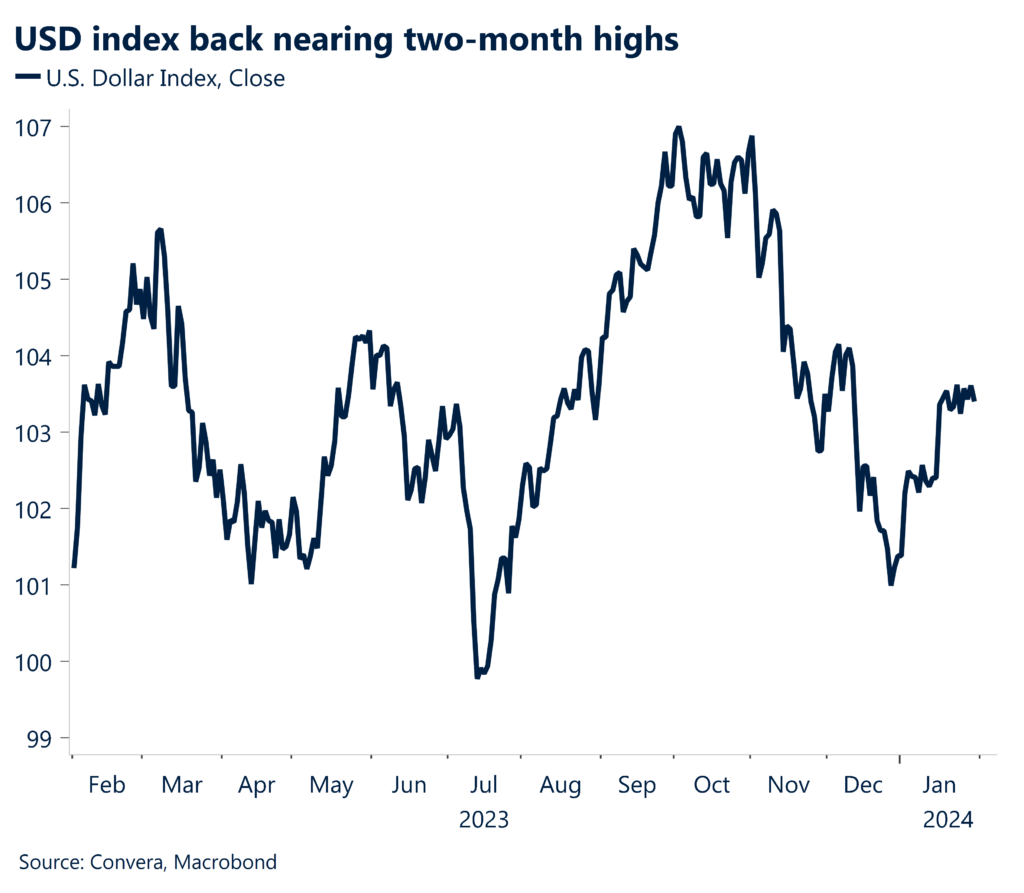

Greenback gains as Powell pushes back

The US dollar was mostly higher overnight after the US Federal Reserve kept interest rates on hold and signaled a March rate cut was unlikely.

The Fed chair Jerome Powell said the critical next step for the Fed is for the board to be “confident” inflation is nearing its 2.0%.

Importantly, Powell said he didn’t think it was “likely” the Fed would have confidence around inflation levels in March.

The probability of a March cut fell from near 50% to 35% after the decision (source: CMW Fedwatch).

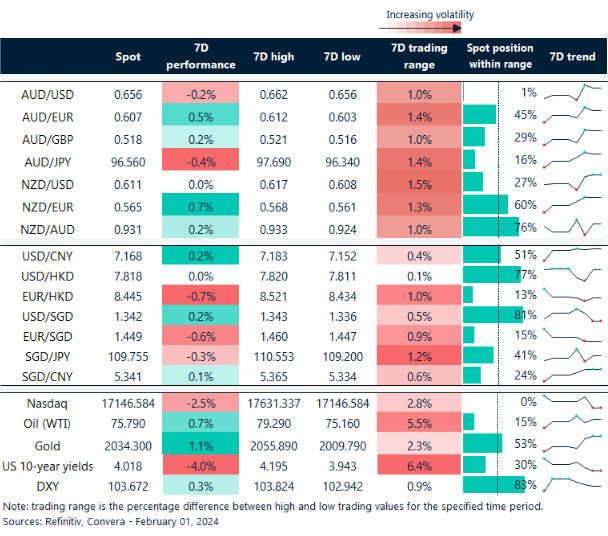

The Aussie led the losses with the AUD/USD down 0.6%. A weaker than expected December inflation reading – with headline annual inflation falling from 5.4% to 4.1% – also weighed on the Aussie.

The British pound remained resilient. The USD/JPY fell 0.4%.

Euro weaker ahead of employment numbers

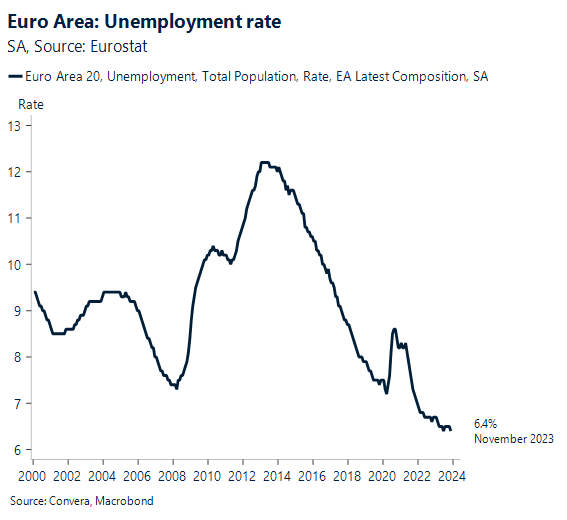

The EUR/USD fell 0.3%. Tonight’s unemployment rate in the euro area for December will likely remain at 6.4%, a record low, even though there are slight chances for a lower number.

Overall, we believe that the unemployment rate’s durability in the face of weak activity surveys and the likelihood of a recession in the euro area is not surprising, given the prevalence of “job retention” programs in many of the region’s member states. This indicates that, in comparison to the national claims measure, the ILO’s LFS estimate of unemployment has been intentionally maintained low.

Limited data is currently available at the nation level, but we do know that Spain’s jobless claims rate decreased in December and that the ILO’s LFS measure increased by 0.1 percentage points to 3.6% in the Netherlands.

The euro remains in a short-term negative trend with next support seen to 1.0720 in EUR/USD.

China’s last major read before New Year

Chinese purchasing manager indexes – for manufacturing – are due.

Given the weak trade data between Korea and China in the first 20 days of January and the possible back-loading of exports to Europe as a result of the ongoing conflict in the Red Sea, we expect the Caixin PMI, which surveys more SMEs and exporters in the eastern coastal regions of China, to fall into contractionary territory in January, dropping to 49.5 in January from 50.4 in December.

Korea’s export growth to China from January 1st to 20th increased to 0.1% year over year from December’s -3.0% growth. However, due in part to a high base from the previous year, import growth deteriorated to -19.5% from -7.9%.

Whether we receive a strong mix of fiscal, monetary, and property sector policy response will determine how the risks to the RMB are balanced. With indications of a potential greater pivot to boost the Chinese economy, the stimulus’s efficacy and quality will ultimately be demonstrated, helping the Chinese yuan to gain. Corporate earnings repatriation should provide a significant boost to the RMB in the event of an effective stimulus, particularly given the low FX conversion ratio.

USD stronger across markets

Table: seven-day rolling currency trends and trading ranges

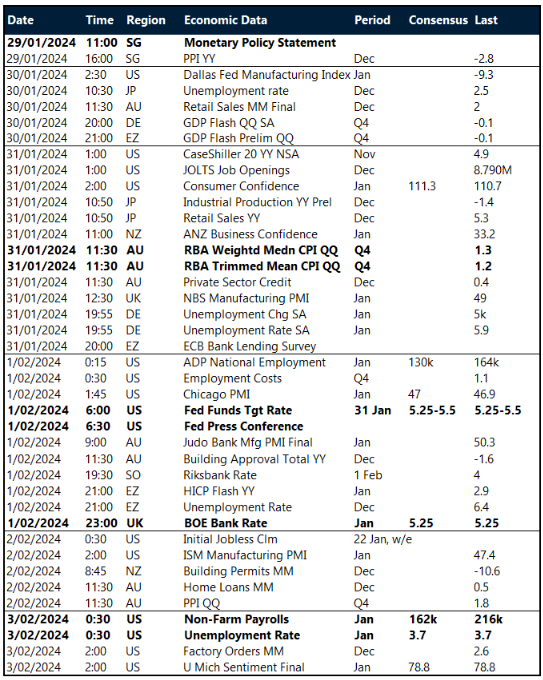

Key global risk events

Calendar: 29 January – 3 February

All times AEDT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.