Written by Steven Dooley, Head of Market Insights, and Shier Lee Lim, Lead FX and Macro Strategist

CPI in shock drop, but Fed stays cautious

The US dollar tumbled overnight after a shock drop in US inflation but a more cautious statement from the US Federal Reserve saw the greenback regain some losses.

Headline CPI was flat in May – versus forecasts for 0.1% – down from 0.3% in April. The annual rate was 3.3%, also below forecasts, and down from 3.4% last month.

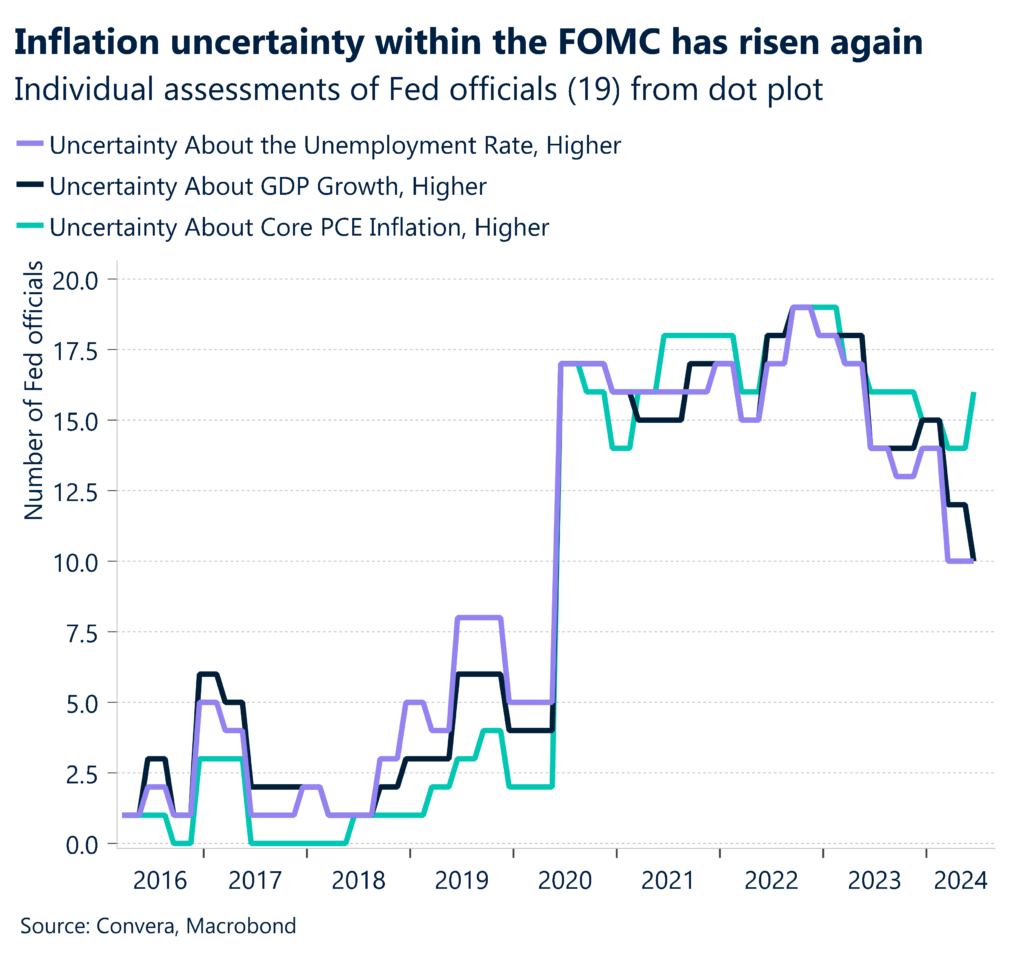

However, the critical Federal Reserve decision saw the central bank more cautious with Fed chair Jerome Powell saying the central bank will need to remain data dependent.

The so-called dot-point projections now see only one rate cut in 2024.

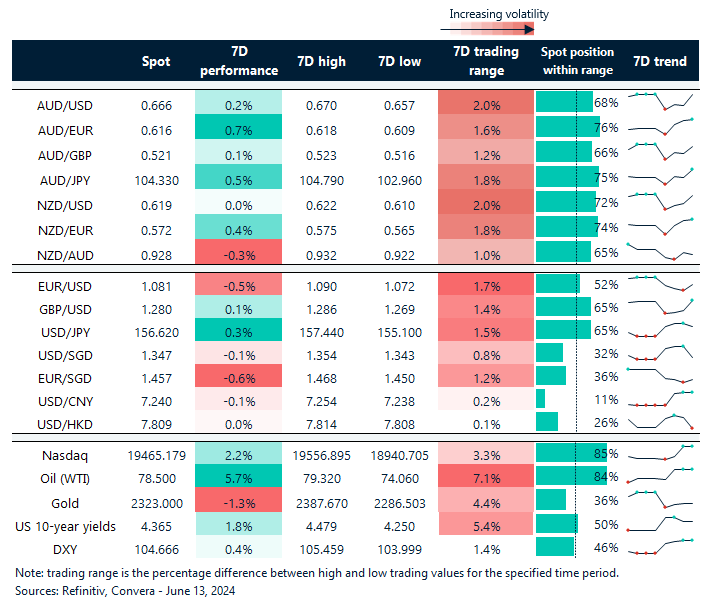

The most notable move was in USD/JPY – the pair initially fell 1.1% before recovering to end down only 0.2%.

The AUD/USD gained 0.8% while NZD/USD climbed 0.7%. The USD/CNH and USD/SGD both fell with USD/SGD near three-month lows.

AUD recovers as valuation gaps with US narrows

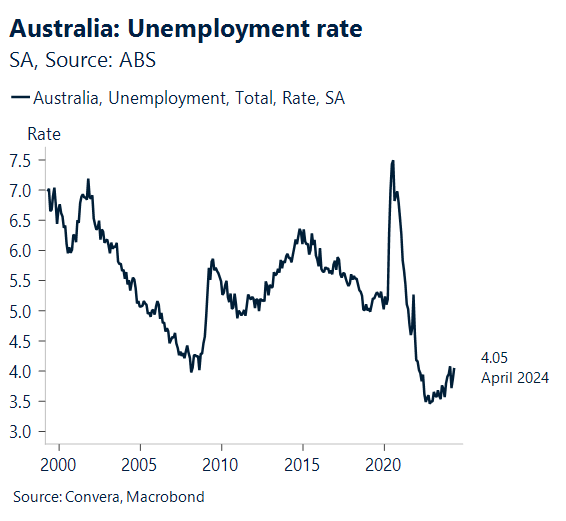

The Australian May jobs report is due at 11.30am AEST. The Australian employment market has remained mostly stronger and there’s a chance of a solid 40k increase in employment in May. A higher-than-average percentage of respondents to the labor force report for April stated they were expecting a new job.

As a result, we anticipate strong employment growth this month. This suggests, in our opinion, that the unemployment rate may retrace around half of its 0.2 percentage point increase in April, returning to 4.0%.

After the third consecutive quarter of below-trend GDP growth in Q1, we do, however, anticipate trend employment growth to moderate over the next months. This is consistent with weakening lead indicators, such as business surveys and job vacancy data.

After bottoming out in February, AUD FX has recovered, closing valuation differences with regard to US interest rates, GDP, and commodity prices.

GBP might be pressured by US exceptionalism and seasonality

There are hints of life in the UK property market. Modest price increases are occurring, approvals have increased, and the most recent data from the Bank of England indicates a rise in mortgage lending.

The RICS survey’s price balance is still negative at -5, but there have been almost no fresh buyer inquiries—a significant improvement from the middle of the previous year.

Though buyer enquiries are outperforming fresh orders to sell, this indicates that we shouldn’t anticipate a major rebound in home values very soon, particularly if the financial market’s assessment of rate cut turns out to be accurate.

The GBP/USD has continued to find resistance at 1.28/2900 and after again turning near that zone the GBP could see some weakness in the short-term.

US dollar lower on the day

Table: seven-day rolling currency trends and trading ranges

Key global risk events

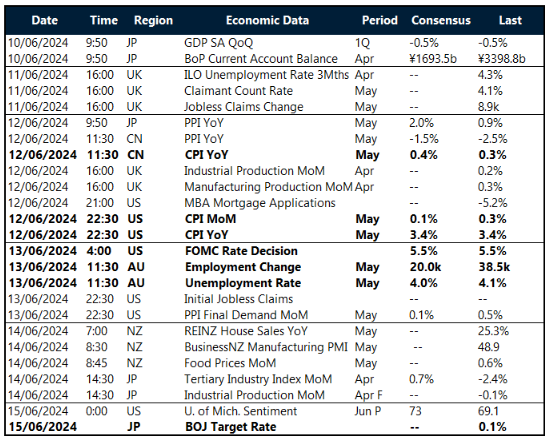

Calendar: 10 – 15 June

All times AEST

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.

Have a question? [email protected]