Written by Steven Dooley and Shier Lee Lim

Fed minutes hit markets

Global markets continued to weaken overnight with the most recent move lower driven by mixed commentary from last night’s US Federal Reserve minutes.

While the Fed signaled that inflation risks are now easing, the central bank also said there was real uncertainty over when the Fed might begin to cut rates.

US shares fell with the S&P 500 down 0.8% and the Nasdaq down 1.0%.

In FX, the US dollar gained, with the USD index up 1.2% over the last two days.

The AUD/USD led losses down 0.5%. The EUR/USD fell 0.2% while the GBP/USD gained 0.4%.

The USD/JPY gained 0.9% while the USD/CNY climbed 0.1%.

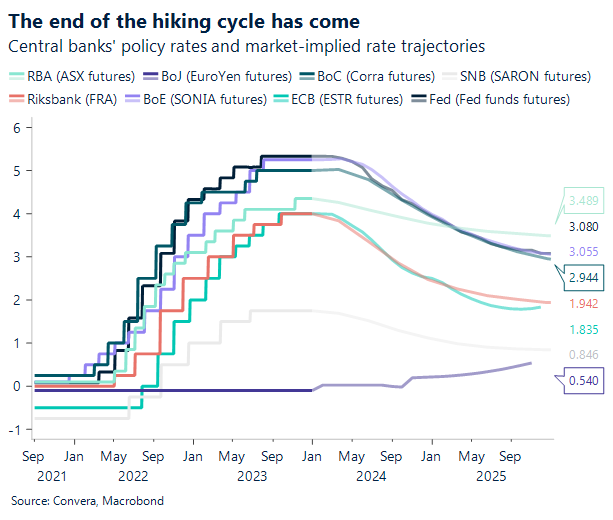

Central banks near peak

Further loosening of financial conditions encouraged by dovish central banks will be advantageous for risk sensitive currencies like the Australian dollar – at least over the longer term.

Better growth forecasts are being anticipated by the market as financial conditions improve due to central bank guidance. Our argument is that this process shouldn’t be standard. The rate at which policies are implemented into growth is important.

We think that due to their slower pass through, Europe and the UK will probably continue to suffer the effects of previous policy tightening rather than the advantages of rate cuts that haven’t yet happened in the coming quarters at least. Small open economies with faster pass-through rates include Scandis and Antipodeans are most likely to benefit.

US election to drive volatility

Into 2024, global unrest and politics should be major themes in FX.

The US elections will be a major event. Risks to the dollar from the elections will be skewed to the upside as the market digests the prospect of fresh tariffs if the current US presidential polling, favouring a return of Donald Trump, continues.

We see several policy avenues that might affect foreign exchange rates, including fiscal policy, trade policy and tariffs, US-China ties, and currency policy. should fetch a lower FX risk premium this cycle than in previous cycles, with the focus being on any tariff proposals and less room for radical policy changes in comparison to 2016 and 2020.

Though there are concerns about the structural deficit and a possible fiscal cliff in 2025, none of these events is likely to be a deal-breaker for the USD at this time. Additionally, FX policy is essentially a second-order tactical factor for the dollar this year, but it can come back into the spotlight, particularly given the present lofty USD values.

US dollar stages comeback

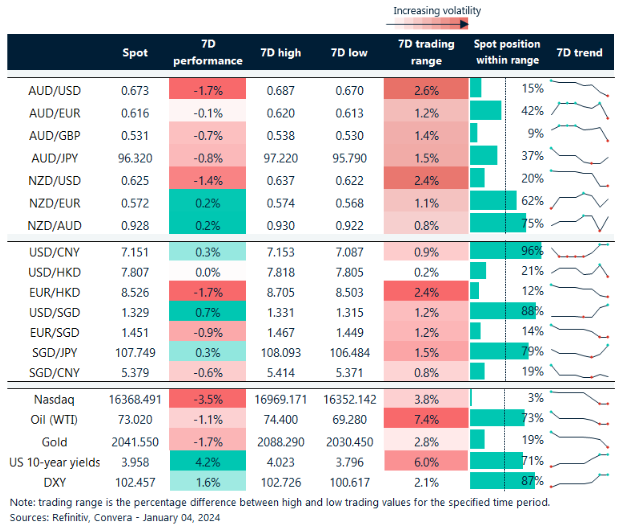

Table: seven-day rolling currency trends and trading ranges

Key global risk events

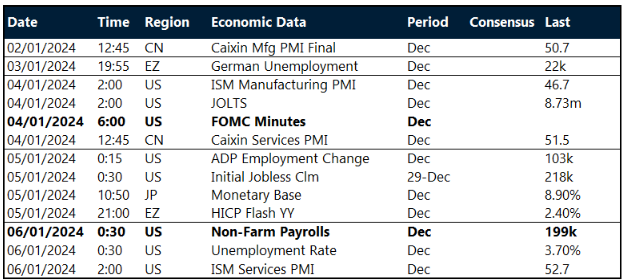

Calendar: 1 – 6 January

All times AEDT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.