Written by Steven Dooley, Head of market Insights

Global overview

The US dollar was lower for a second day despite better data in a sign that markets are instead focused on commentary from Fed officials. The Chinese yuan was weaker ahead of today’s GDP reading.

US dollar mostly lower despite strong data

The US dollar fell for a second day despite a stronger-than-expected retail sales number and better industrial production numbers.

Instead, markets remain focused on commentary from Federal Reserve officials that suggests that higher bond yields mean there is less necessity to raise official interest rates further.

Overnight, Richmond Federal Reserve president Tom Barkin said higher bond yields have tightened conditions but the Fed can’t rely on bond yields to necessarily do the central bank’s work for it.

All eyes are on the major speech from Fed chair Jerome Powell due on Thursday night.

China GDP due

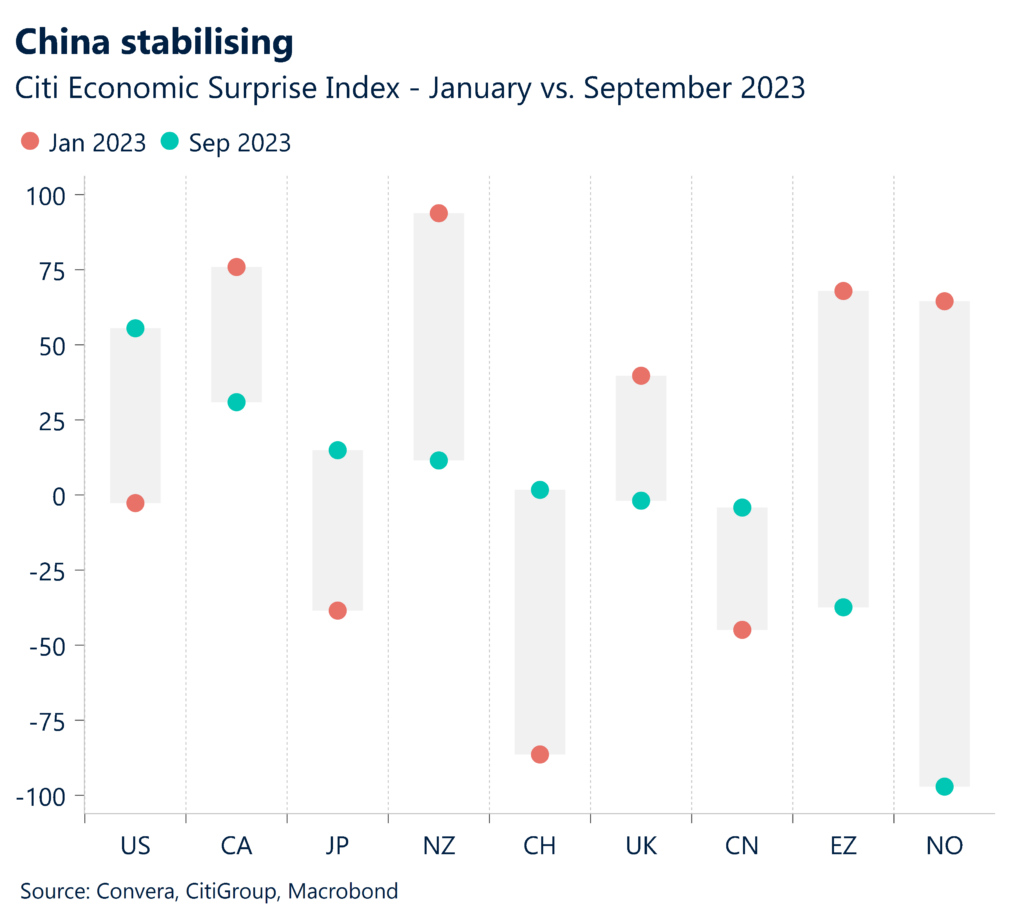

Chinese September-quarter GDP is the big event today. The market expects real GDP growth to decline from 6.3% in Q2 to 4.4% YoY in Q3.

The market expects largely steady industrial production and retail sales growth in September, at 4.3% and 4.5% YoY, respectively, down only slightly from 4.5% and 4.6% in August.

Meanwhile, we anticipate fixed asset investment growth be flat at 3.2% in September.

The recent signs of stabilization include PMIs and the moderate property rebound in top-tier cities. Overall, we continue to have a cautious view for growth.

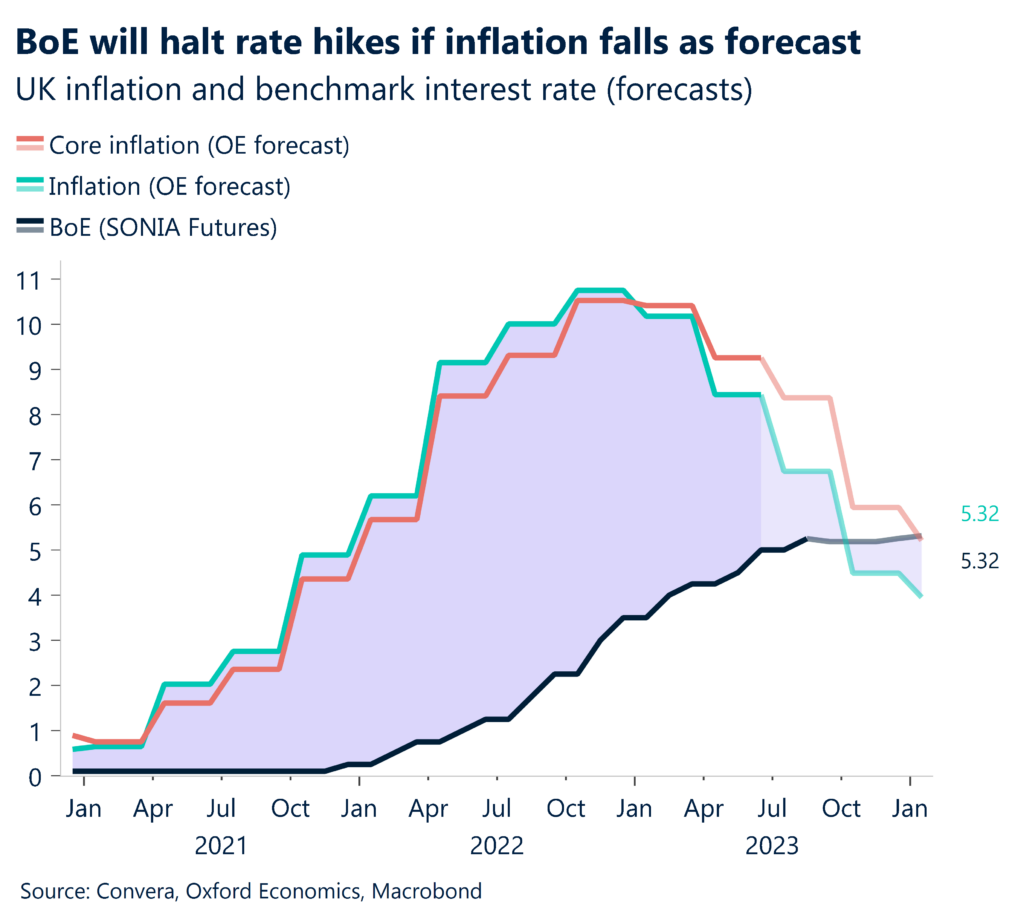

GBP weaker ahead of UK inflation

UK CPI might be the driver in European trading tonight.

The British pound was sent sharply lower after last month’s lower than expected inflation reading. The August core CPI inflation shocked considerably to the downside down by almost 0.7 percentage points at the core level. Inflation for services also decreased, from 7.4% to 6.8%.

The possibility of an outright decrease in food prices (as indicated by the BRC shop price index), continued rent increases, and rising gasoline prices are important trends to keep in mind when reading the September report.

Overall, headline and services inflation are expected to edge down slightly from Aug 6.7% to 6.5% consensus, and core inflation to slightly decline from 6.2% to 6.0%. Retail price index inflation is expected by the market to be down 0.2 percentage points to 8.9% (Prior: 9.1%).

The British pound was weaker overnight with the GBP/USD down 0.3%.

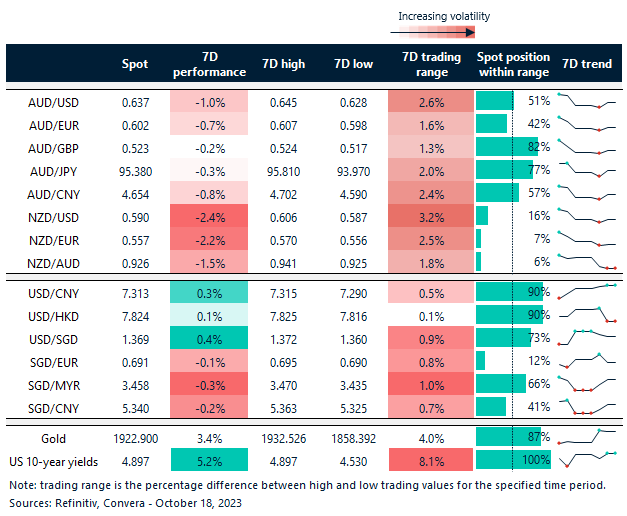

Chinese yuan in focus ahead of GDP

Table: seven-day rolling currency trends and trading ranges

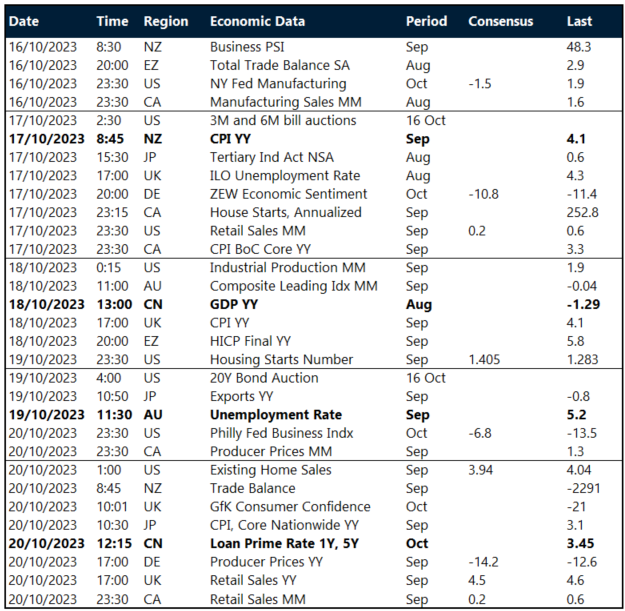

Key global risk events

Calendar: 16 – 20 October

All times AEST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.