Global overview

Financial markets continued in their recent buoyant mode with the S&P 500 and Nasdaq hitting new highs. Central banks remain in focus with the RBA, Fed and ECB providing updates over the next 48 hours.

Aussie boosted, Chinese yuan surges

Global optimism continues to boost markets with the S&P 500 climbing to the highest level since August this year and the tech-focused Nasdaq hitting the highest level since January 2022.

The ongoing hopes that the US Federal Reserve has finished its rate-hiking cycle are the main driver with the benchmark 10-year bond yield falling to 4.41% overnight – well down on the 5.02% seen four weeks ago.

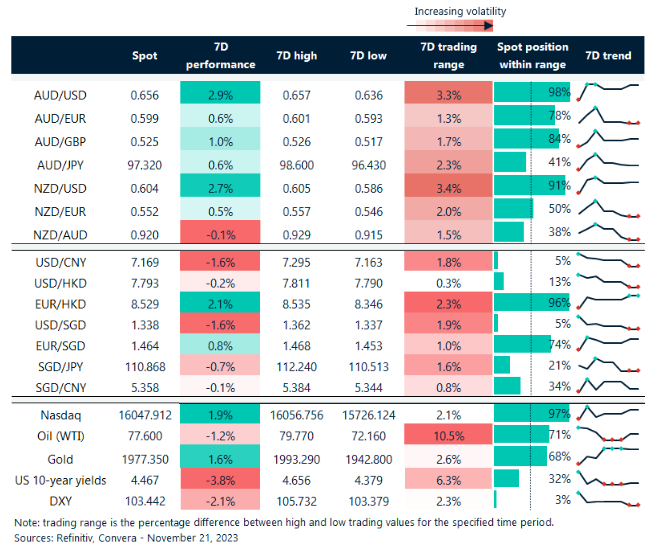

Risk-sensitive currencies like the Australian dollar have outperformed in this environment with the AUD/USD up 0.8% overnight as it hit the highest level since 10 August.

The NZD/USD gained 0.9% while the USD/SGD fell 0.4%.

The Chinese yuan surged after the People’s Bank of China kept the loan prime rate on hold – seen as a sign of positive for the Chinese economy. The USD/CNH fell 0.7%.

The global central bank outlook remains key to FX markets with Reserve Bank of Australia minutes and a speech from RBA governor Michele Bullock due today, the Fed minutes due overnight, and European Central Bank president Christine Lagarde speaking on Wednesday night.

Pound supported ahead of Autumn Statement

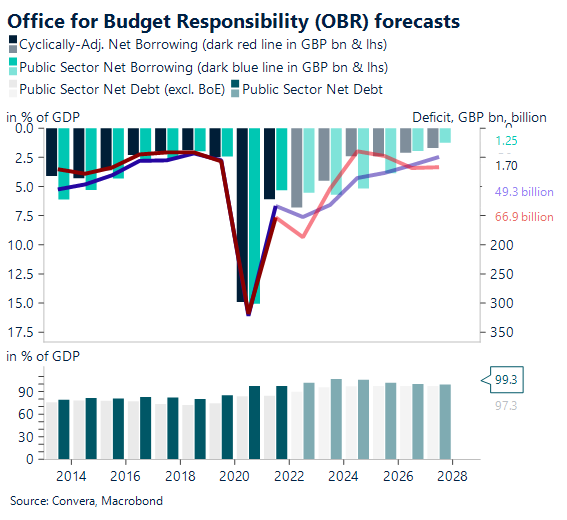

The headline budget deficit (PSNB-ex), as of the six months of the fiscal year that have been published, is almost £20 billion less than what the Office for Budget Responsibility (OBR) had predicted at the time of the March Budget.

The day before the Autumn Statement, the October numbers are released, making them a significant collection of data. But as the Chancellor’s budgetary choices will have been approved long before this data set is made public, they will mostly be predicated on results from the first half of the fiscal year. In October, the OBR projected a £16.3 billion cash deficit and a £13.7 billion PSNB-ex deficit. Considering the recent pattern of improved outturns, there might be a chance that these deficit projections are less than what the OBR anticipated.

The BoE is somewhat more aggressive than the ECB in terms of monetary policy. Although the UK and the euro area are both experiencing slow economic development, we believe that the UK is less likely to have a recession. This provides support to the GBP.

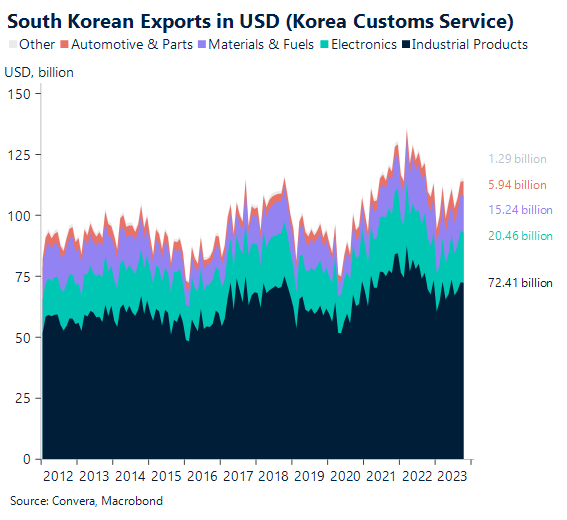

South Korea exports due

For the first twenty days of November, we anticipate that export growth will increase to 8.3% y-o-y (October: 4.6%). It’s also possible that November’s daily average export growth held steady at 8.3% y-o-y (October: 8.6%), indicating two months in a row of increases.

Thanks to robust US demand, most products—including chips—likely maintained their sequential increases over the first 20 days of November. Simultaneously, we anticipate that export growth to China will strengthen the export recovery. We anticipate that November as a whole will see the first double-digit increase since May 2022, supported by a rebound in export prices and strong demand from important trade partners.

The recovery in electronic exports is still going strong, recent tax reforms have increased income, and lower oil prices all support the Korean won.

Aussie, yuan jump

Table: seven-day rolling currency trends and trading ranges

Key global risk events

Calendar: 20 – 25 November

All times AEDT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.