Written by Steven Dooley and Shier Lee Lim

Aussie, kiwi bounce from recent lows

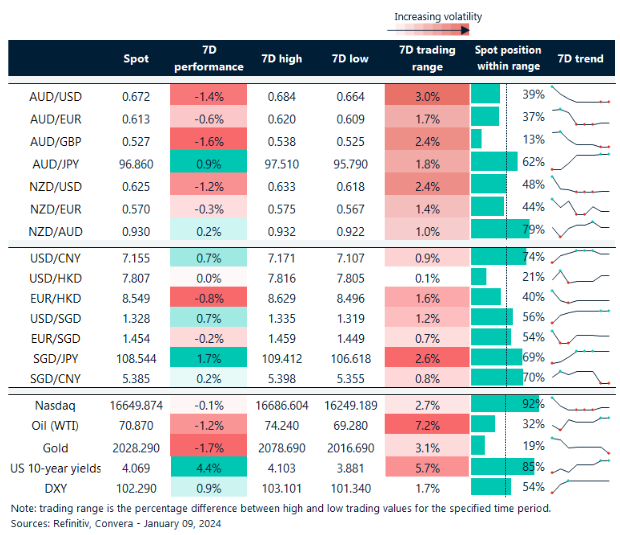

A strong showing from US shares helped key currencies recover overnight with the Australian and New Zealand dollars both bouncing from recent lows.

The AUD/USD rebounded from the four-week lows seen on Friday while the NZD/USD climbed from three-week lows as US shares produced a strong session.

The S&P 500 gained 1.4% while the Nasdaq jumped 2.1%. US shares were helped by news of strong consumer demand over the Christmas break.

FX markets were quieter in Asia with the USD/CNH flat and the USD/SGD down 0.1%.

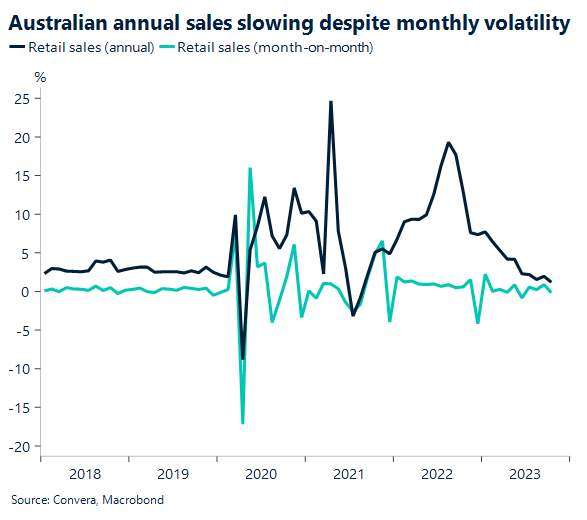

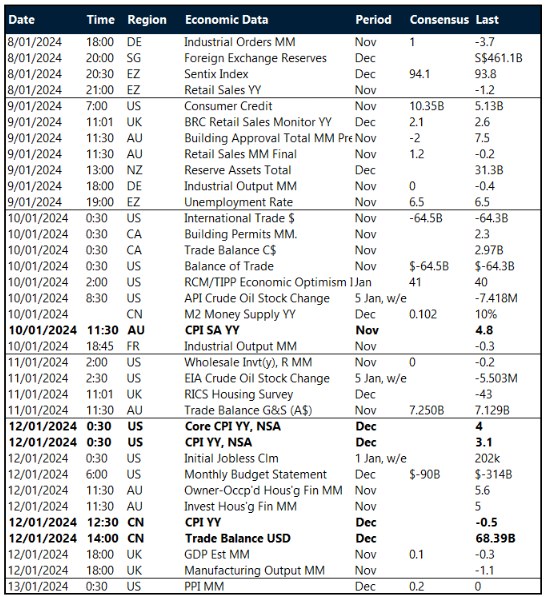

The Australian dollar will remain in focus today with retail sales and building approvals due. On Wednesday, the Australian monthly inflation reading is due.

US data slowing, but moderately

The US dollar was mostly weaker overnight as US bond yields eased. The US ten-yield bond yield fell from 4.04% to 4.01% overnight.

The next key US release is the US NFIB small business survey, seen as likely to fall 0.1 percentage point in December after falling 0.1 point in November. The net proportion of enterprises expecting the economy to improve has been negative since November 2020.

Separately, the Dallas Fed banking conditions survey indicated that credit conditions were tightening at a slower rate.

As a result, the net proportion of enterprises anticipating credit conditions to soften may improve slightly, but will still be in contractionary territory. Furthermore, easing financial circumstances may alter the net proportion of enterprises planning capital expenditures and job growth.

The US dollar index continued to see support level at 103. As per the chart below, small business pricing intentions generally lead CPI and there may be a risk of higher US inflation print and therefore higher DXY index.

Euro weakening ahead of jobs data

The euro has gained versus the US dollar over the last two months – in line with most other currencies – but the EUR has fallen versus other markets like the Aussie, kiwi and SGD.

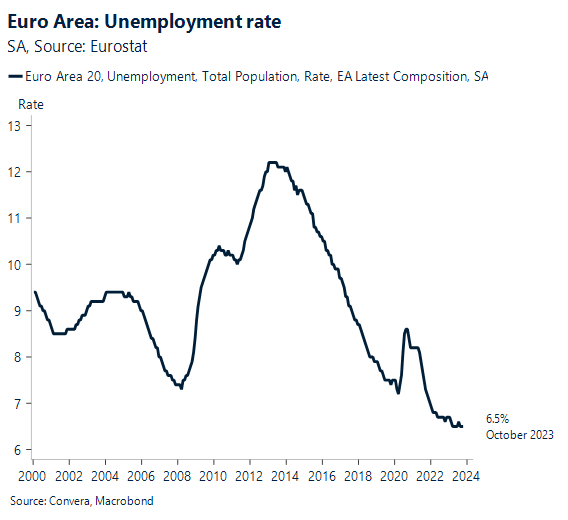

Looking forward, eurozone’s harmonised unemployment rate looks set to remain steady in November at 6.5%, but with greater risk of an positive surprise — lower unemployment — that could support the EUR in the short term.

Continued resilience in the unemployment rate despite weak activity surveys and a likely recession in the eurozone would be unsurprising, in our opinion, because many eurozone countries have so-called job retention schemes, which mean that the ILO’s LFS measure of unemployment is kept artificially low relative to the national claims measure.

We already know that the ILO’s LFS measure remained steady in Germany (at 3.1%) and fell in the Netherlands, and that the Spanish jobless claims rate fell in November, albeit this may have been offset by the corresponding French measure, which climbed by a similar amount.

The EUR/USD’s recent gains have reflected the pull-up factor of declining inflation and a pivoting Fed, which has been supportive of cyclical currencies like the euro at the expense of the dollar.

More broadly, however, the trend is likely EUR negative going forward, with our year-end target for EUR/USD at 1.0700.

Aussie, kiwi rebound from lows

Table: seven-day rolling currency trends and trading ranges

Key global risk events

Calendar: 8 – 13 January

All times AEDT

Have a question? [email protected]