Written by Steven Dooley, FX & Macro Strategist – APAC

Global overview

US shares were sharply lower overnight with the S&P 500 falling to three-month lows. The broader financial worries saw the US dollar favoured and currencies like the AUD hit. This morning’s Australian inflation and tonight’s US durable goods orders are today’s key releases.

“Higher for longer” hits markets

Financial markets continue to be hit by the so-called “higher for longer” narrative with last week’s Federal Reserve statement – signaling expectations that US interest rates will still be above 5.00% by the end of next year – weighing on sentiment.

Overnight, US shares were sharply lower, with the S&P 500 down 1.5% and falling to the lowest level since June. The Nasdaq also lost 1.5% and similarly fell to three-month lows.

The risk aversion gripping markets saw the US dollar favoured with the USD index rising to the highest level in 10 months.

The AUD/USD was hit hard, down 0.4%, as it closed at the fifth-lowest level for the year.

Central bank divergence back on the agenda

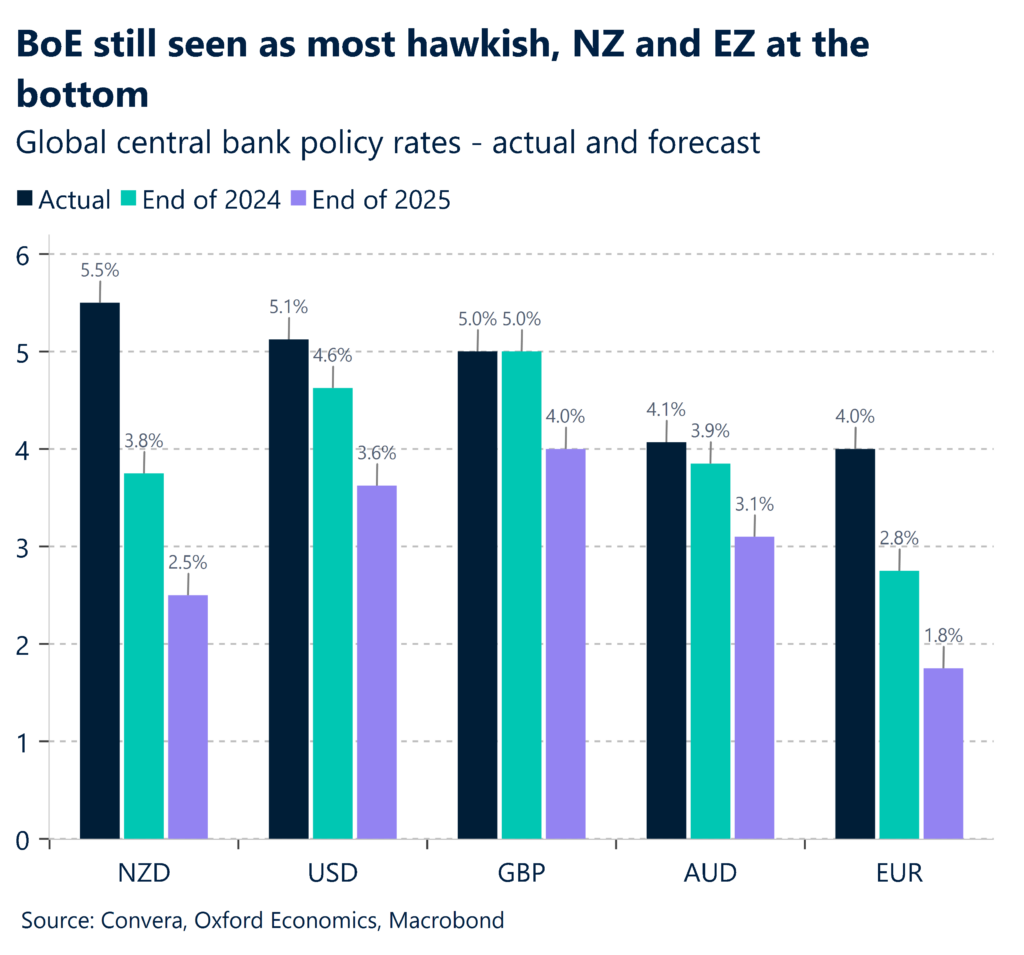

The Fed’s tough talk last week contrasted with a view in other markets that key central banks might be moving to a loosening bias.

In particular, market expectations for the euro have shifted markedly, with market pricing looking for the European Central Bank deposit rate to fall from 4.00% currently to 2.80% at the end of 2024. The market sees the ECB rate at 1.80% at the end of 2025.

The Reserve Bank of New Zealand is also seen as likely to reverse course soon and this has, no doubt, recently pressured the kiwi. On the other hand, the US Fed and UK’s Bank of England are seen as remaining the most hawkish, providing support to their currencies.

Australian inflation in focus

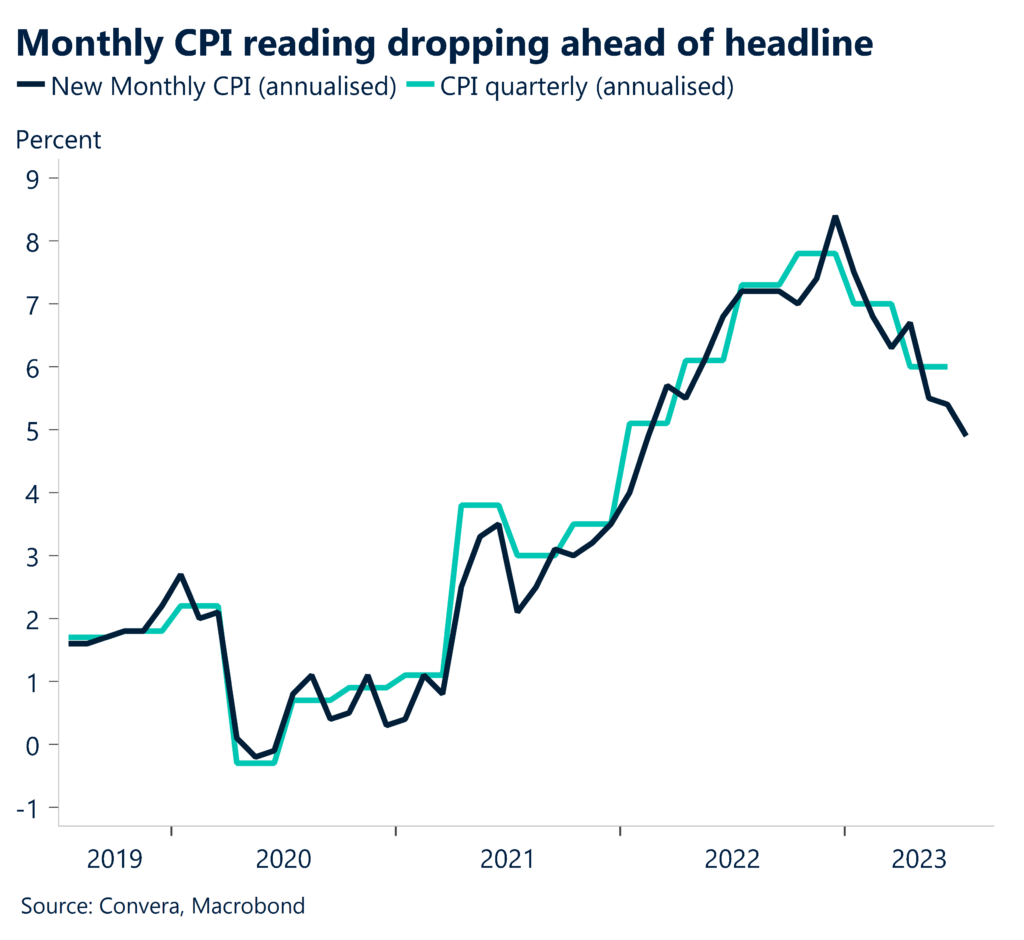

Australia’s monthly inflation number is this morning’s key release with market forecasts looking for an increase from 4.9% in July to 5.2% in August. The recent jump in oil prices is likely to be the main contributor to higher inflation.

Australian inflation is due at 11.30am AEST.

Later, US durable goods orders are due. The increase in durable goods orders in August, excluding transportation, is anticipated to be 0.1% m-o-m, per Reuters Poll, continuing to signal solid growth in the US economy.

August saw high industrial production, and regional manufacturing surveys indicated that new orders were improving. Overall durable goods orders might be more negative, down 0.5% m-o-m in August, but this is likely due to a reduction in Boeing net orders as well as weakness in other transportation equipment.

A higher-than-expected reading may see further gains for the USD.

Aussie back near lows

Table: seven-day rolling currency trends and trading ranges

Key global risk events

Calendar: 25 – 29 September

All times AEST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.