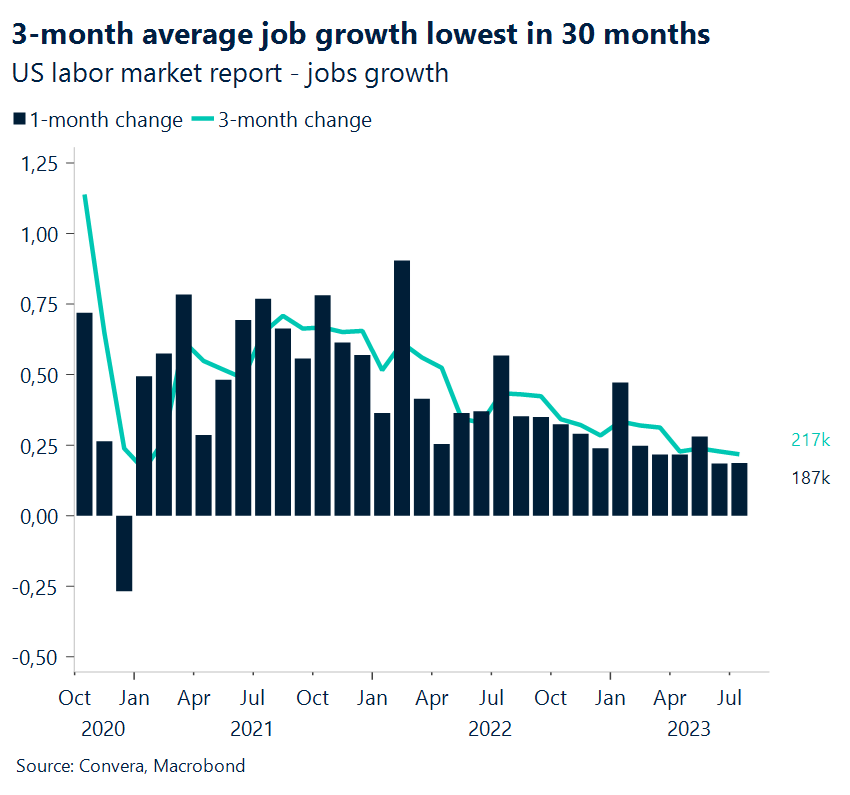

US jobs growth falls to 30-month low

The latest US jobs report had something for everyone in it, but markets chose to focus on the headline job growth miss, sending yields and the US dollar down on the last day of the trading week. Now it’s up to the upcoming US inflation report to strengthen or question the ever more likely scenario of a US soft landing.

The US labour market remains incredibly tight judging by elevated wage growth (4.4%) and the unemployment being only 10 basis points higher than the 50-year low reached in April. However, jobs growth has continued disappointing the consensus and has been revised to the downside for six consecutive months now. The US economy added 187k jobs in the month of July, bringing down the three-month average to the lowest level since January 2021 at 217k. A favourable inflation print on Thursday could bring down the probabilities of a rate hike by the Federal Reserve (Fed) in September even further, which currently stands at only 13%.

Short-term treasuries continued their sell-off after Atlanta Fed President Bostic said that there would be no need to raise interest rates further to ease inflation. However, longer-dated government bond yields soared higher, in the process steepening the yield curve and putting pressure on the US dollar. Both the S&P500 and Nasdaq fell by the most last week since the collapse of the Silicon Valley Bank back in March, shedding 2.8% and 3.1%.

Pound mixed as UK GDP eyed this week

The Bank of England (BoE) raised its key interest rate to a fresh 15-year high last week as expected, but the pound slipped against most peers as it starts the month of August on the back foot. GBP/USD fell to a 5-week low last week as risk aversion swept across financial markets following the US credit rating downgraded. The currency pair bounced off key support levels nearer the $1.26 handle but suffered its third weekly decline in a row, whilst GBP/EUR sunk back below €1.16.

It was a three-way vote split amongst the BoE’s Monetary Policy Committee last week, six voting for a 25-basis point hike, two for 50 basis points and one committee member voting for no change. The main takeaway from the press conference was that the BoE thinks rates are restricted as they are, but the job to tame inflation isn’t over – so markets are pricing another 25-basis point hike in September but are no longer fully pricing another one after that. So, we are certainly near the peak it seems, but the BoE wants to make sure everyone knows interest rates won’t be coming down anytime soon. Still, the expected peak of UK rates has dropped from 6.5% to around 5.7%, narrowing the gap with the Fed’s expected peak rate, which is another reason why the pound has surrendered most of the gains it made last month, falling about 3% from above $1.31.

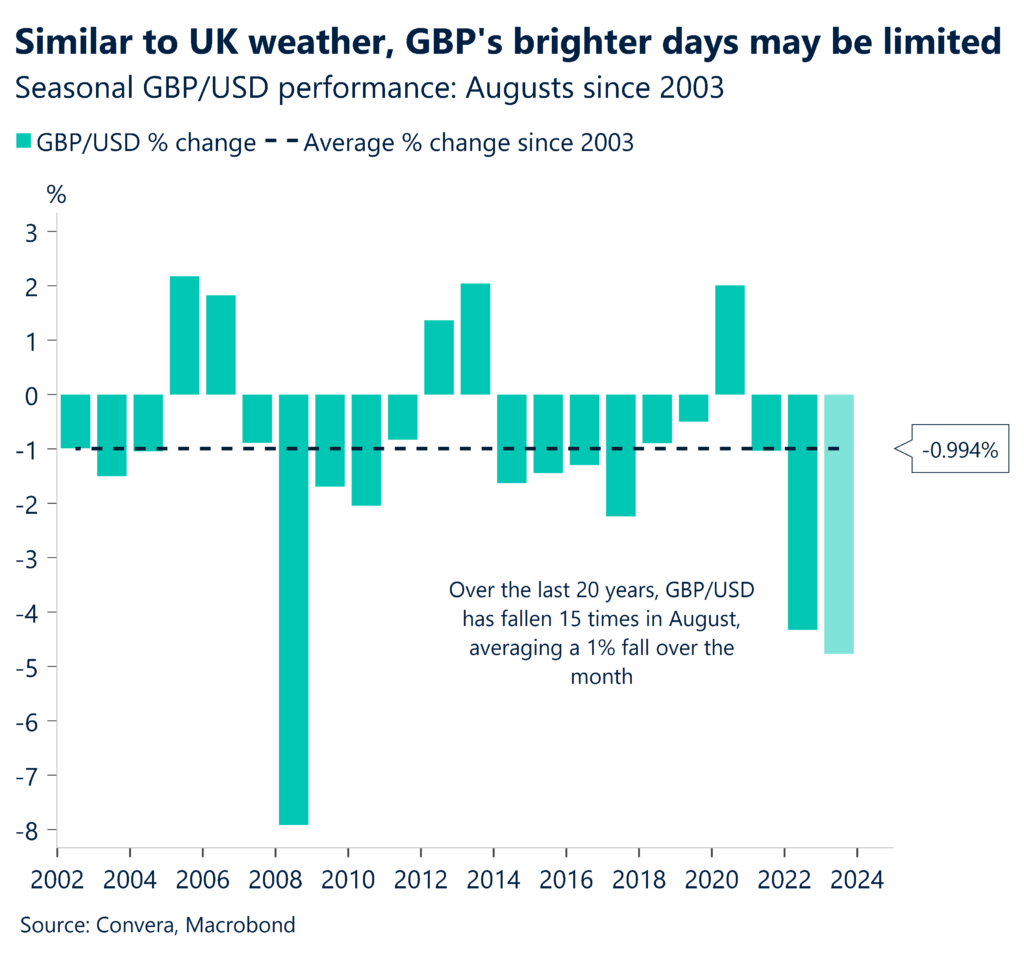

This week, there’s limited top-tier UK data to digest except for UK GDP on Friday, which is set to show a modest increase in second quarter output. The BoE and GBP traders will be more interested in services inflation and wage growth though, which will be published next week. Additionally, although we note that seasonality trends should not be used in isolation, the pound has started August as it usually does – weaker against the US dollar.

Euro slides after German industrial output disappoints

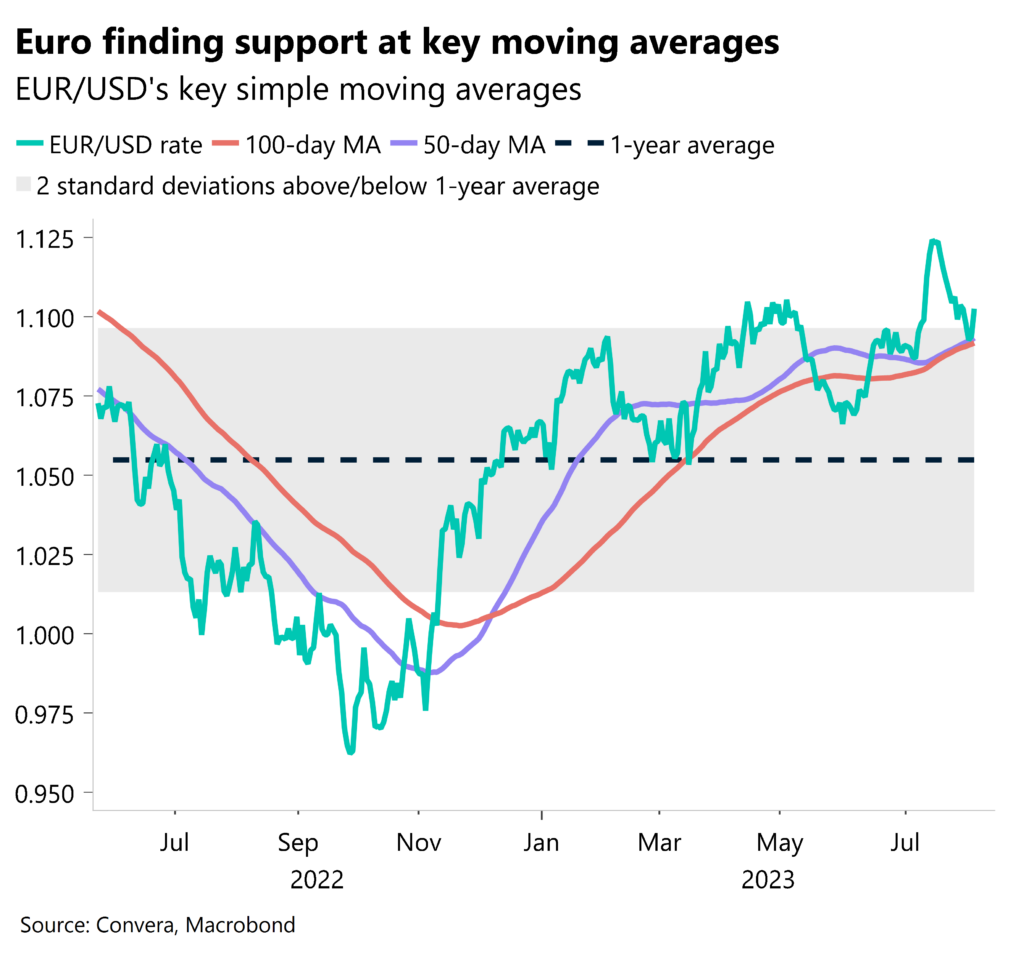

With the US dollar slumping on Friday, EUR/USD managed to close the week back above $1.10, but the euro has started the new week on a softer note following weaker-than-expected German industrial production data. The recent deterioration of German macro data has reignited political debates about inflation and the future of Europe’s industrial sector.

While the recent easing of supply-chain bottlenecks has been welcomed news, a combination of falling demand and new orders and a weakening global consumer have become the main culprit of a stagnating German economy. As most hard data points have stagnated and remained in negative territory, GDP growth has been lacklustre for the past three quarters and the IMF expect Germany’s economy to contract overall in 2023. Forward looking indicators support this notion too with both soft and hard macro data pointing to a subdued outlook going into the second half of the year. Indeed, this morning’s industrial production data for June (-1.5%) came out much weaker than the consensus (-0.3) and versus our own forecast of a 0.4% decline.

EUR/USD is back under the key $1.10 handle, but to see a significant continuation of this move lower the currency pair will have to convincingly break below its 50- and 100-day moving averages, located just above $1.09, which offered decent support last week.

Risk aversion rattles stocks & riskier currencies

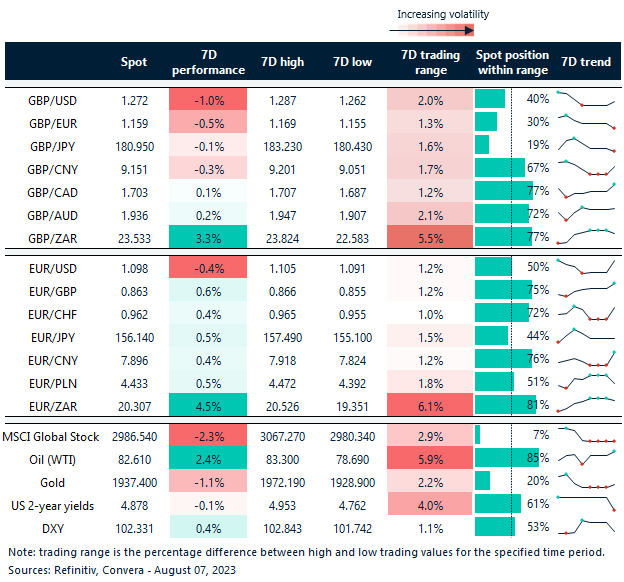

Table: 7-day currency trends and trading ranges

Key global risk events

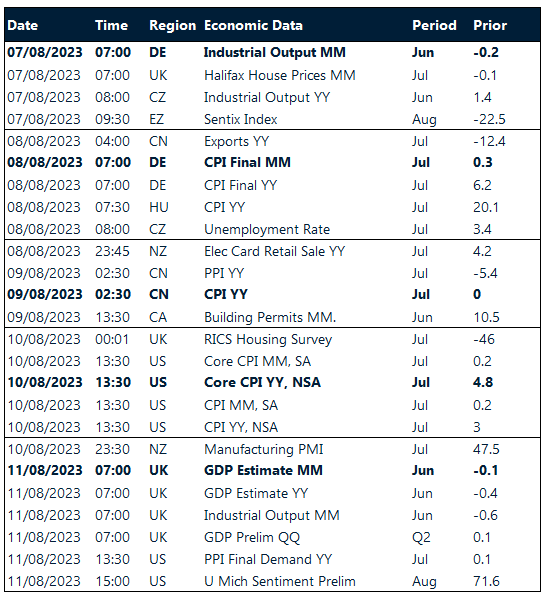

Calendar: August 7-11

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.