Check out our latest Converge Market Update Podcast covering global market’s start to 2024, central bankers fight against investors, the US macro outperformance, China’s watershed moment and geopolitical developments featuring global macro strategist, Boris Kovacevic.

Written by Steven Dooley and Shier Lee Lim

US inflation continues to cool

Global markets ended a quiet week with a muted reaction to more good news on US inflation.

US inflation continued to fall in December with the annualised personal consumption and expenditure number – the Federal Reserve’s preferred measure on inflation – steady at 2.6% while the core number fell from 3.2% to 2.9%.

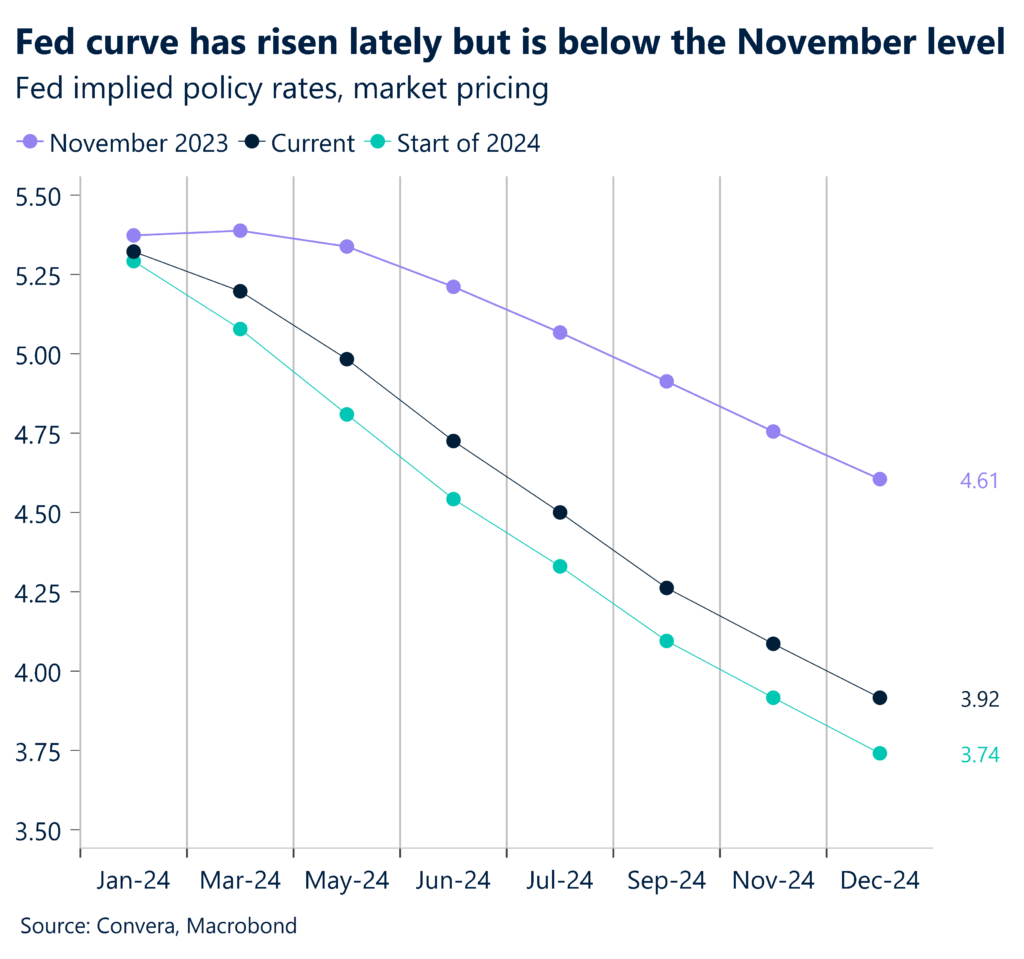

The result leaves the door open for a Fed cut in March with markets ascribing a 50% chance of a cut.

However, FX markets were mostly unmoved by the data.

The euro was mostly lower last week after Thursday’s European Central Bank decision indicated policymakers were growing more concerned about slowing growth. The GBP was broadly steady last week.

The Japanese yen was initially stronger after the Bank of Japan’s policy decision but USD/JPY ended the week flat.

The AUD/USD ended down 0.1% on Friday to also finish broadly flat for the week.

USD/CNH back towards highs

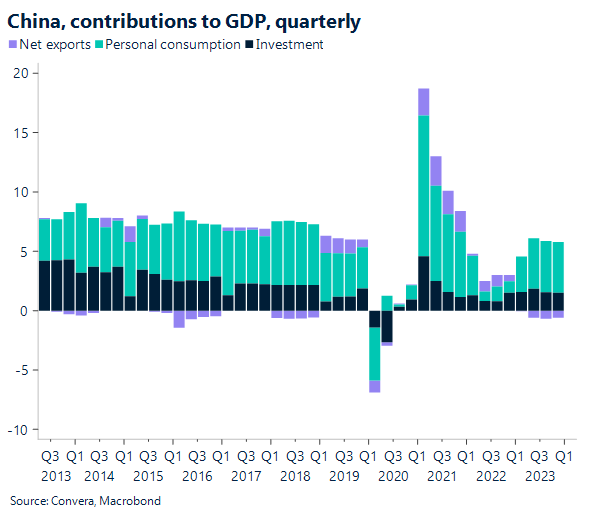

In 1H24, we anticipate that the Chinese economy may turn more positive, but in 2H24, it will moderate to trend growth.

Because of the shifting dynamics in the price of commodities globally, we anticipate that the deflation – ie falling rate of inflation — will cease in 2024.

Despite this, low inflation will continue because of policy assistance that is skewed toward production rather than consumption.

USD/CNH has recently come free of the Nov-Jan pattern lower and looks towards the initial target of 7.239-7.2665.

Central banks might need to stay tight

As a result of this year’s major positive shocks fading, restrictive monetary policy, increasing rates, and other factors, global GDP looks likely to drop to below-potential.

Despite the fact that headline inflation is predicted to decline in the upcoming year, we anticipate a change in inflationary attitudes that will maintain global core inflation at around 3%, mostly due to ongoing pressure to raise labor and service pricing.

There will likely need to be a continuing tightening tilt in central bank language.

Given high rates, slowing growth, a difficult environment for stocks, and elevated geopolitical risks, we anticipate the VIX to generally trade higher in 2024 than in 2023.

The timing and severity of an eventual recession, which is still a real possibility, will determine how much the VIX increases.

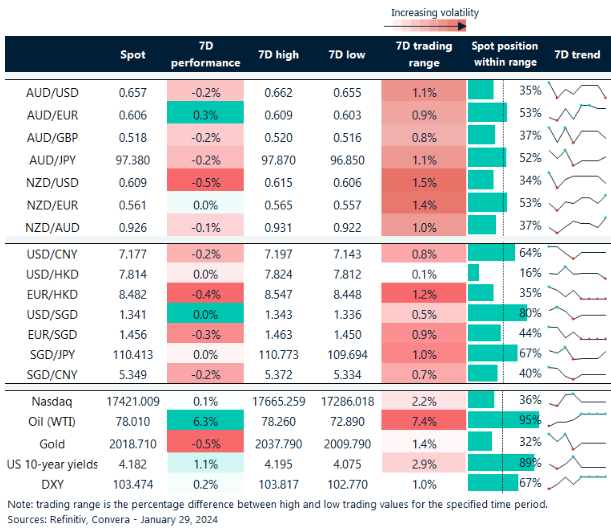

Flat week for FX

Table: seven-day rolling currency trends and trading ranges

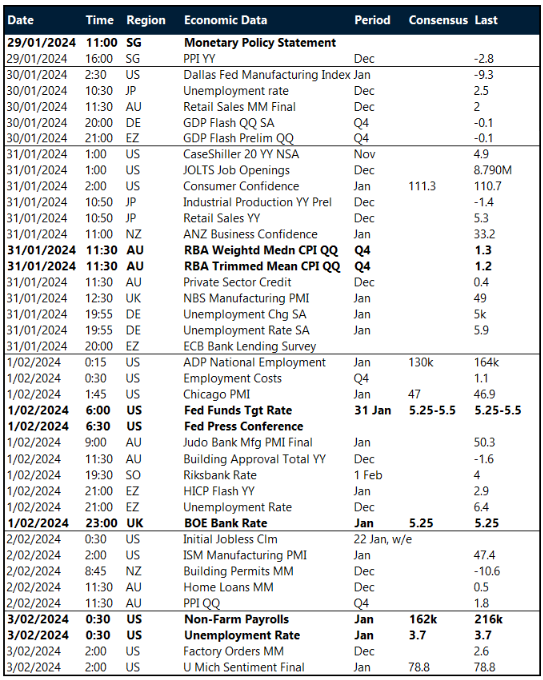

Key global risk events

Calendar: 29 January – 3 February

All times AEDT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.