Hot labour data knocks back Fed cut hopes

US Treasuries sold off 3–6bps overnight, led by the front end, after a much stronger-than-expected payrolls report (+130k vs consensus +65k) and a weak 10yr auction.

Traders now expect the first Fed rate cut in July, not June. The US two-year yield rose as much as 10bps intraday before settling 6bps higher at 3.51%.

January NFP rose 130k (consensus +65k), unemployment fell to 4.28% (consensus 4.4%), and average hourly earnings rose 0.41% m/m (consensus +0.3%).

The labor force participation rate edged up to 62.5%.

Fed officials signaled caution, with one noting rates should remain “somewhat restrictive” to avoid persistent inflation. US equities closed flat as the jobs data weakened the case for imminent rate cuts.

Gilts outperformed on bull flattening as UK political concerns eased, though headlines remain volatile.

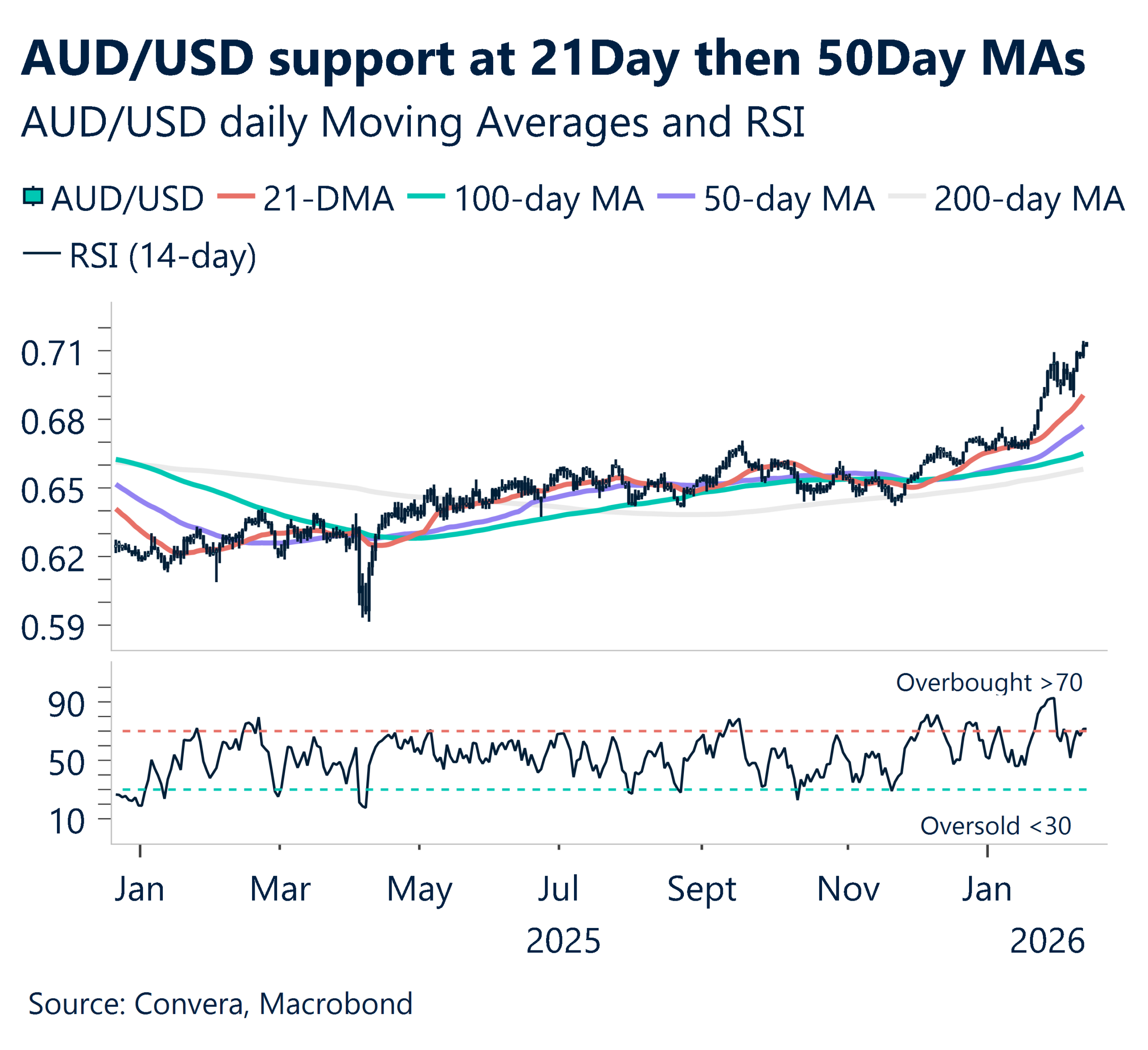

Aussie jumped 0.7% overnight on RBA’s Hauser comments. Kiwi was flat.

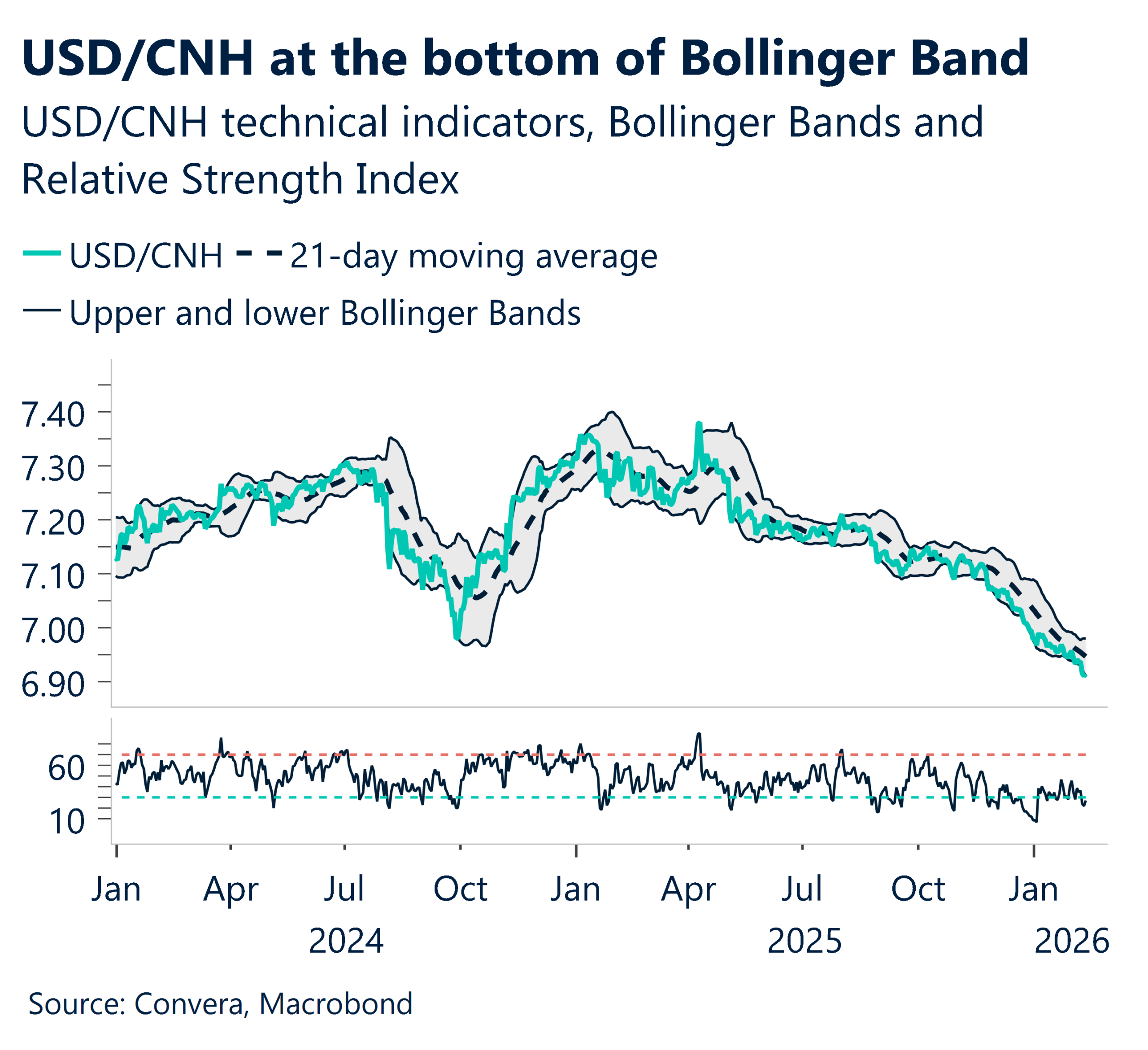

USDSGD down 0.2% and USDCNH was flat.

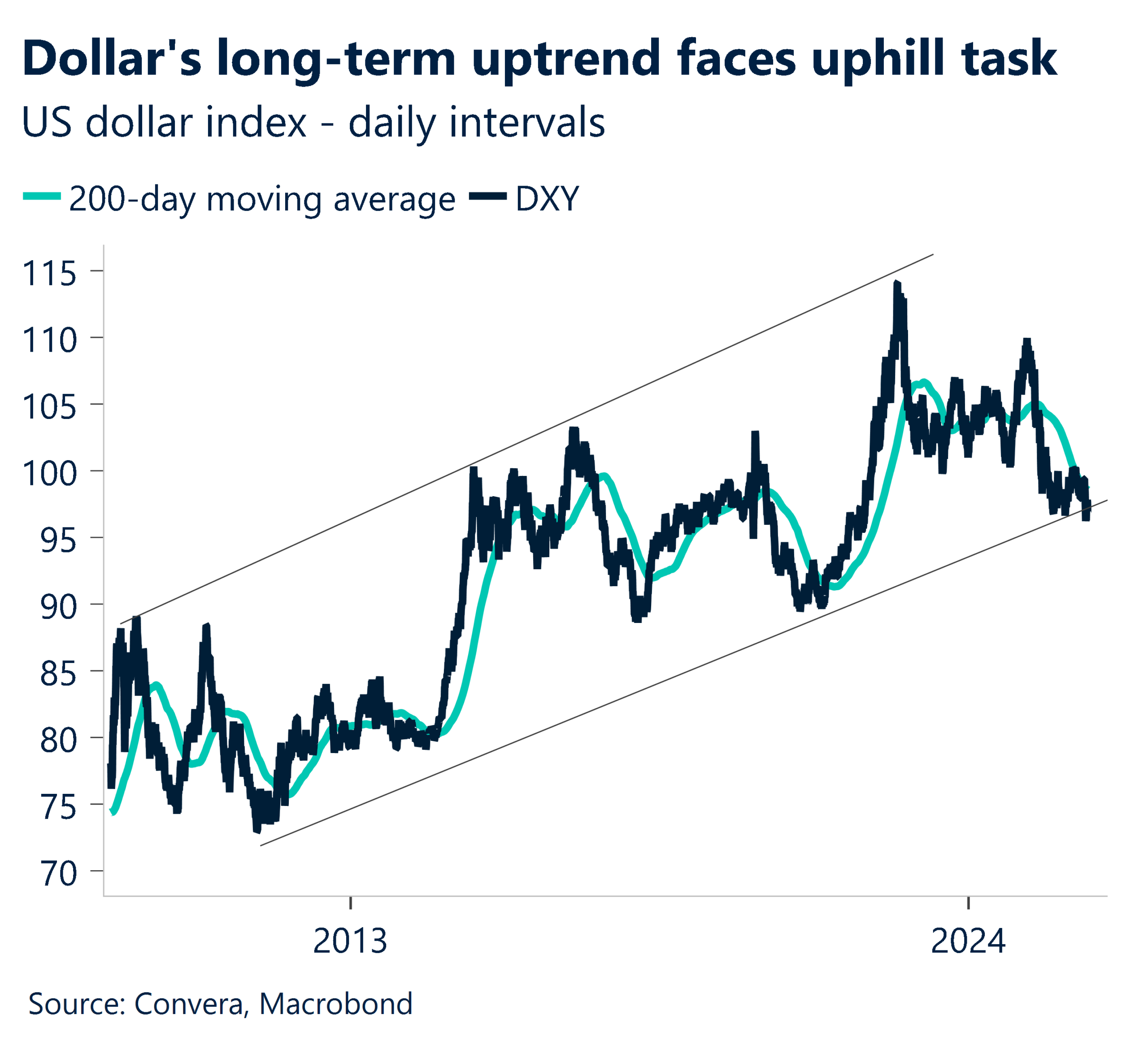

Dollar index down for 4th straight trading day.

RBA warning lifts Aussie dollar

RBA deputy governor Andrew Hauser says inflation remains “too high” and the central bank can’t allow it to persist much longer, according to Bloomberg. He argued that some of the recent rise in prices shows stronger demand running into supply limits. If that’s the case, he warned, inflation could stick around, and the bank “can’t let that happen.”

His comments pushed AUDUSD above 0.71.

Hauser added that policymakers need to “respect the speed limit,” saying that trying to push the economy beyond its capacity would only fuel inflation, which he called the biggest drag on productivity growth.

AUD/USD now trades just 0.2% below its recent high of 0.7143, last reached on February 11.

Key support sits at the 21‑day EMA at 0.6957, followed by the 50‑day EMA at 0.6822. The pair is also overbought on the RSI.

China prices slip again as demand stays weak

China’s consumer prices rose just 0.2% in January, falling short of the 0.4% forecast and slowing from 0.8% the month before.

The statistics bureau said the softer reading reflected the timing of the Lunar New Year and cheaper oil, but those factors were already well understood.

The miss underlines how stubborn China’s deflation pressures remain.

Factory‑gate prices also stayed negative. Producer prices fell 1.4% from a year earlier—slightly better than expected and the smallest drop since July 2024—helped by firmer commodity prices and efforts to rein in excessive competition.

USDCNH is now sitting near a 33‑month low, trading just 0.02% above the recent trough of 6.9049, last reached on February 10.

Key resistance stands at the 21‑day EMA at 6.9411, followed by the 50‑day EMA at 6.9801.

Aussie overbought on RSI

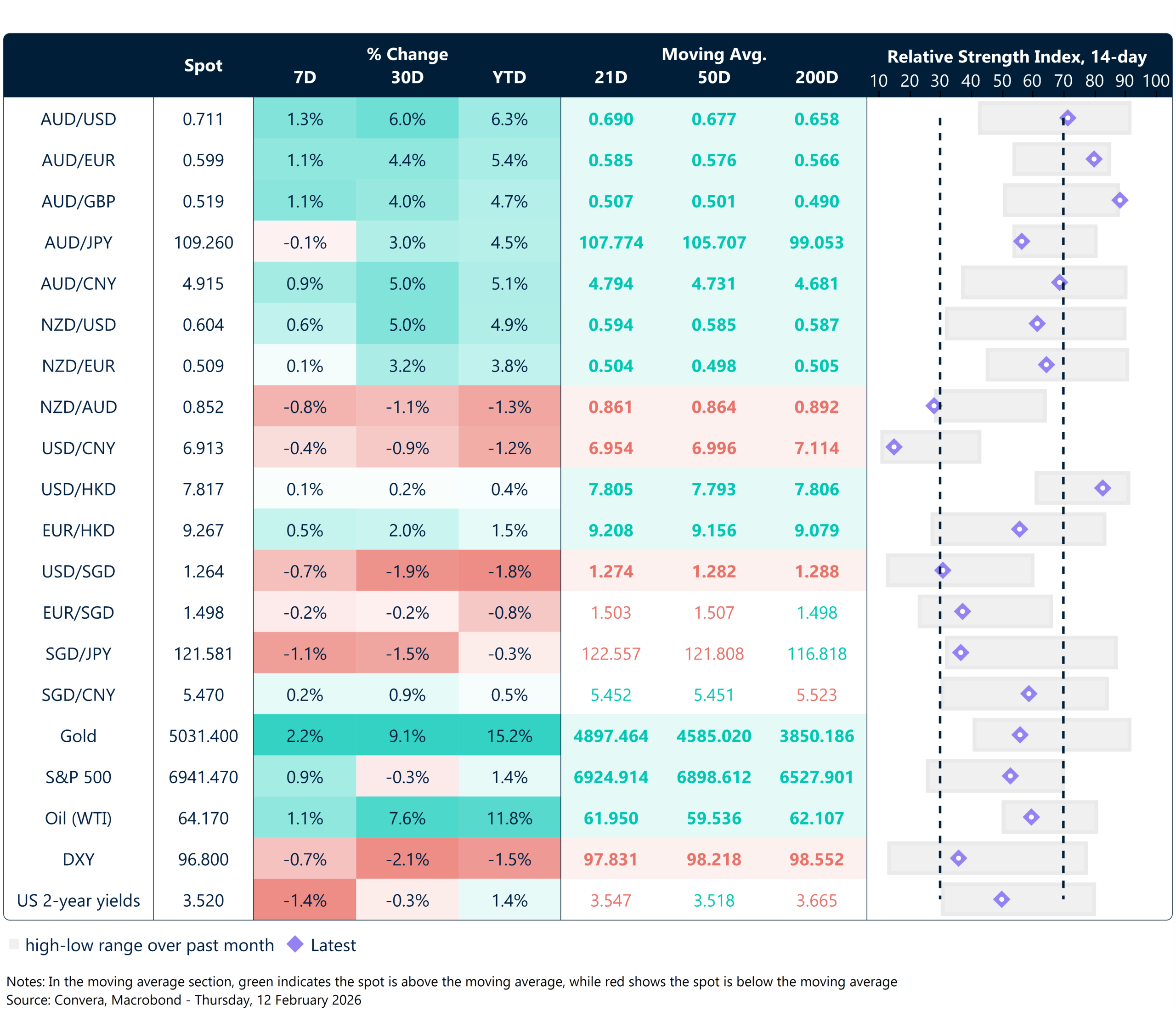

Table: seven-day rolling currency trends and trading ranges

Key global risk events

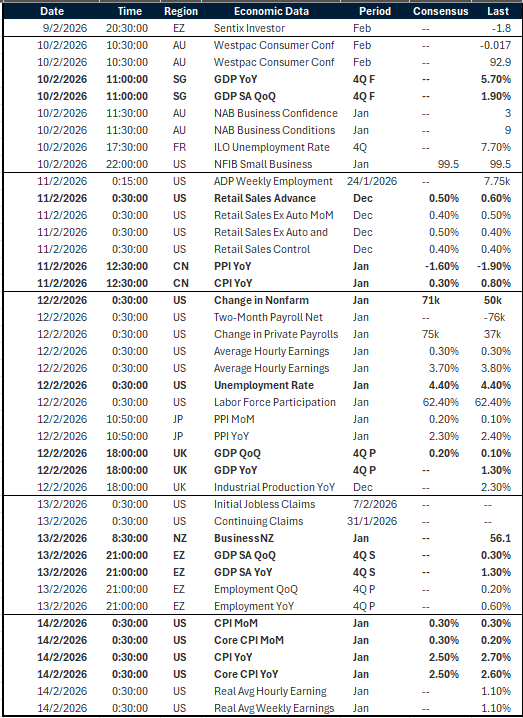

Calendar: 9 – 14 February

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.