Written by the Market Insights Team

Could the worst still be ahead?

Kevin Ford – FX & Macro Strategist

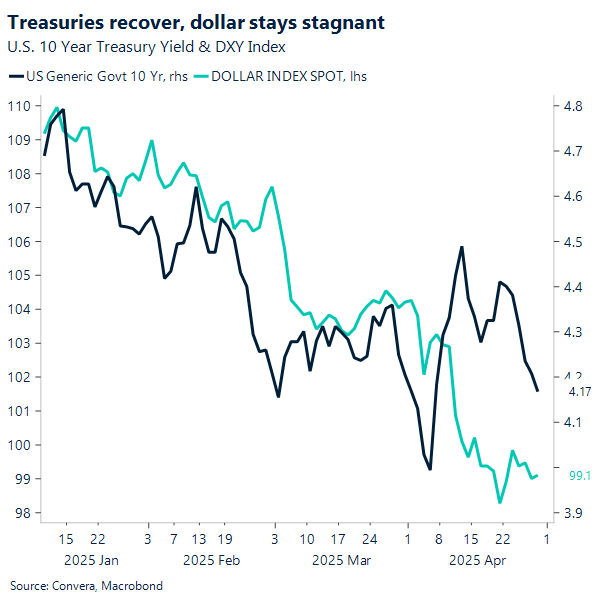

Mid-week has brought another noteworthy price movement in markets. The 10-year U.S. Treasury yield dropped from a recent high of 4.58% a few days ago to 4.16% yesterday. With market fears easing—reflected by the VIX Index falling below 25—U.S. stocks have held steady, maintaining last week’s gains. However, the dollar remains stagnant despite the broader market rally.

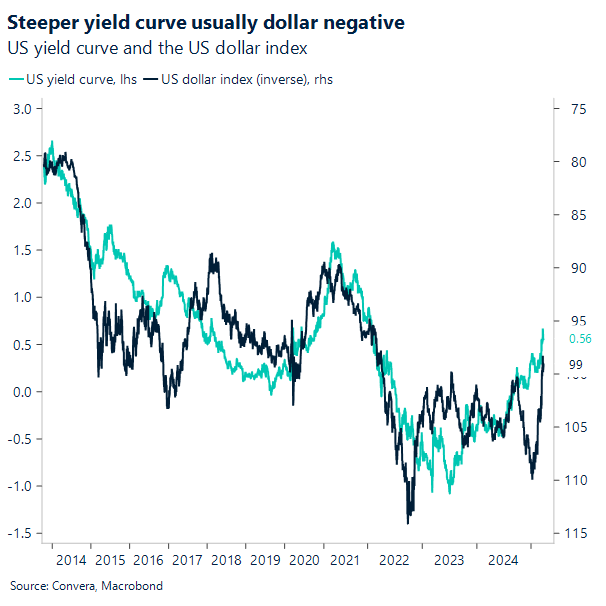

Growth concerns continue to weigh heavily on sentiment. WTI oil prices are approaching a potential break below $60 per barrel. This cautious outlook is also shaping the U.S. yield curve, which has steepened recently—a development that typically supports a weaker dollar, especially when worries about growth dominate and volatility eases.

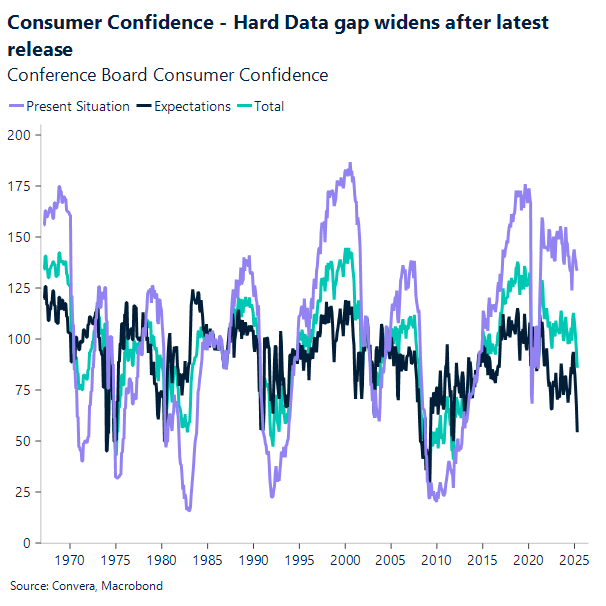

Could the worst still be ahead? The growing gap between weak soft data and hard data still brings key points. This disconnect could stem from lags in economic impacts, front-loaded consumption aimed at avoiding higher prices or disconnect between consumer sentiment and behavior. If the issue is simply a lag, the recent market rebound may not hold for long.

What else might support the growing fears of a slowing U.S. economy? First, the Beige Book, which last week highlighted a significantly worsening outlook in several Districts as economic uncertainty, particularly around tariffs, increased. Second, ocean container bookings from China to the U.S. are down over 60%. The U.S. imports $600 billion worth of goods from China, with 95% arriving by sea and retailing for around $2 trillion. Prolonged tariffs at current levels could deal a major blow to the retail economy. However, quarterly earnings from U.S. companies provide additional insights. While uncertainty is now widely regarded as the new normal, some companies have noted that consumer health remains strong. This was echoed by the CEOs of Amex and Capital One in their recent earnings calls. Clearly, the impact of tariffs will vary across sectors.

Today, the US GDP, PCE, and April jobs report will shed light on whether hard data confirms the trends that soft data has been signaling in recent weeks.

No changes for the Loonie

Kevin Ford – FX & Macro Strategist

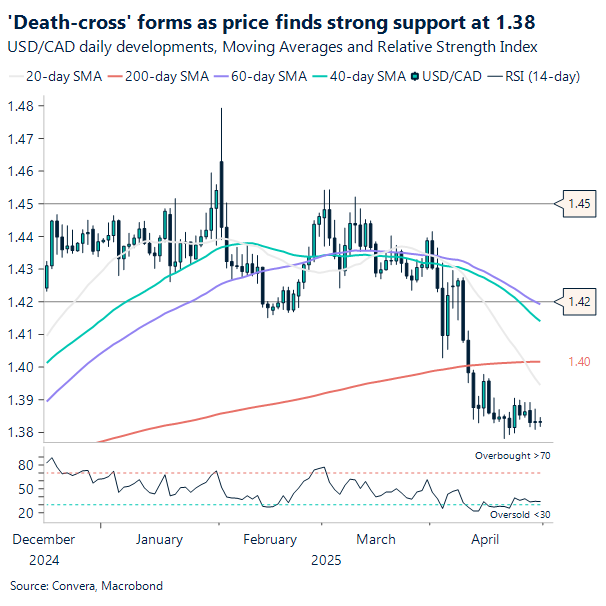

A relatively quiet end of the month for the the Loonie, which has been supported by sustained dollar weakness, with the DXY index dropping 4.5% this month to its lowest level since April 2022. The USD/CAD has gained 4% in April, finding solid support at 1.38 after five consecutive weeks of declines from 1.44. Remaining below its 200-day SMA of 1.4015, the Loonie has established a key support level at 1.378 and resistance at 1.39.

Current price action indicates a potential medium-term rebound, with the pair possibly revisiting the upper end of the 1.373–1.40 range. From a technical perspective, a death cross has formed, with the 200-day SMA crossing below the short-term 20-day SMA—a pattern that typically signals continued downside momentum.

While today brings the release of Canada’s advanced GDP figures for February, market attention will largely be driven by hard data out of the U.S. and any trade policy remarks from the U.S. administration, which could influence sentiment and price action.

Mexico and U.S. water agreement

Kevin Ford – FX & Macro Strategist

The U.S. and Mexico reached two critical agreements on Monday, easing tensions that threatened to complicate trade negotiations sparked by tariffs imposed by the U.S. administration.

First, Mexico committed to deliver additional water from the shared Rio Grande basin to Texas farmers. This move comes after U.S. concerns that Mexico was failing to meet its obligations under a decades-old water-sharing agreement. Second, the two nations reached a deal to tackle the New World screwworm pest in Mexico, averting the possibility of restrictions on U.S. livestock imports from its southern neighbor.

Mexico is showing its ability to work with the U.S. despite the confrontational tone of the U.S. administration. Unlike Canada, which has opted for retaliation in response to tariffs, Mexican President Sheinbaum has chosen a path of negotiation. This approach was evident in the recent agreements, including Mexico’s commitment to deliver more water to Texas farmers and a joint effort to tackle the New World screwworm pest. While details of the water-sharing deal remain scarce, both nations reaffirmed the value of the 1944 treaty, agreeing it continues to benefit both sides without needing renegotiation.

These agreements reflect Mexico’s focus on maintaining critical trade and agricultural ties, a reassuring signal for markets wary of escalating tensions. By addressing key issues through collaboration rather than conflict, Sheinbaum’s strategy highlights the importance of agriculture in strengthening U.S.-Mexico relations and navigating the challenges posed by tariffs.

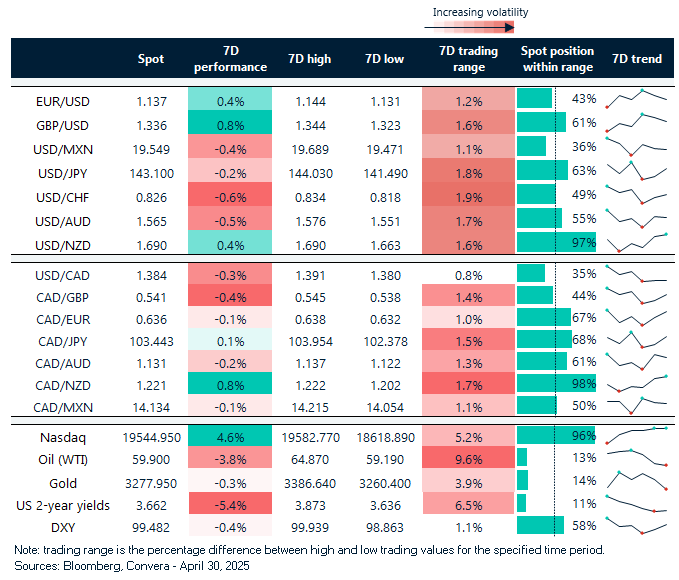

WTI Oil falls below $60 as US 2-year yields slide 5% in a week

Table: 7-day currency trends and trading ranges

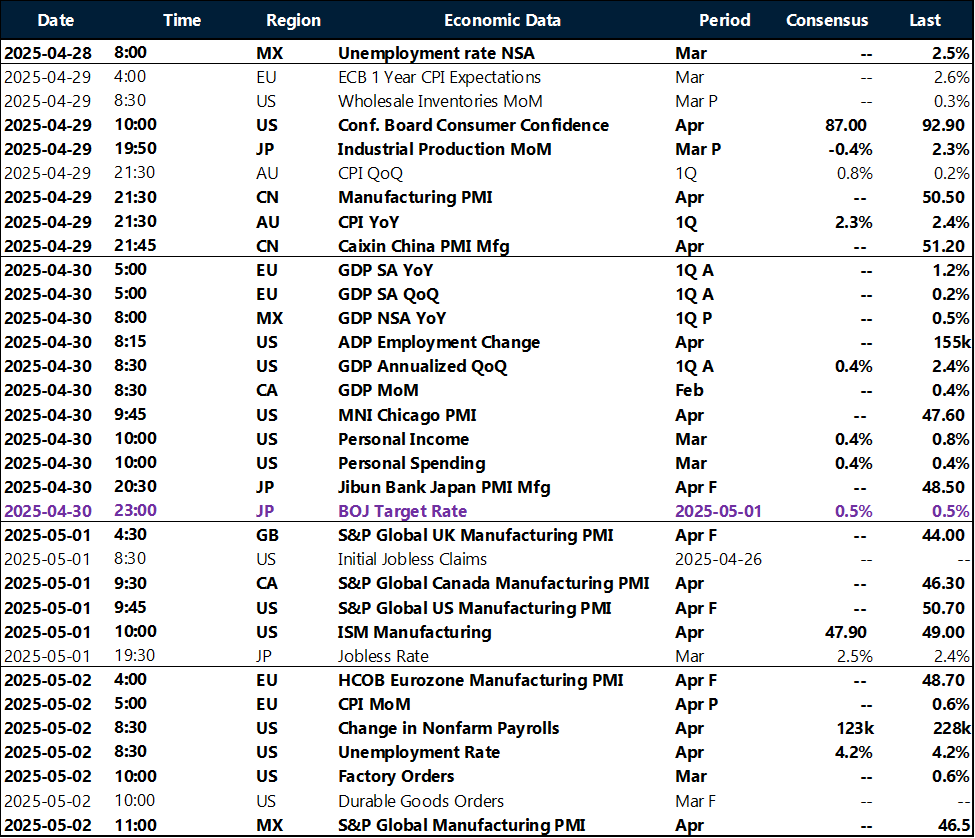

Key global risk events

Calendar: April 28- May 2

All times are in ET

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quothave a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.