Written by Convera’s Market Insights team

Dollar flirting with fresh 1-year high

George Vessey – Lead FX Strategist

The US dollar index stretched to a fresh one-year high before sharply reversing course on Thursday, which was no major surprise given the dollar had climbed into overbought territory reflected by the 14-day relative strength index above 70. Still, the dollar index has risen over 6% in seven weeks, its strongest run over such a timespan since 2022. Souring risk sentiment on Friday is helping the safe haven buck advance once again though, whilst equities turn lower after Jerome Powell signaled there’s no need for the Fed to rush with rate cuts and that PCE inflation was likely to rise.

The dollar’s acceleration this week emerged after President-elect Donald Trump’s hawkish cabinet picks and the Republicans maintaining control of the House, delivering Trump a trifecta and raising the scope of pushing his agenda. Economic momentum had already shifted back in favour of the US, motivating yet another hawkish repricing of the Fed’s cutting cycle, which is dollar positive, both via tariff and fiscal-monetary policy mix channels. Though Trump’s policies and expectations for sustained US growth into 2025 should further overwhelm seasonal dollar weakness into year end, uncertainty remains high, and the key takeaway is that it is now all about the scale and speed of policy shift.

On the data front, aligned with CPI on Wednesday, PPI data signal inflationary pressures in parts of the economy, which threatens to slow the Fed’s easing path. The increase in core goods was the largest gain since February. The inflation readings support our call for the Fed’s next rate cut in December, whilst overnight swaps are pricing a 46% chance and only two cuts in the next five Fed meetings.

ECB cut 100% priced in

Boris Kovacevic – Global Macro Strategist

Five straight daily declines have led the euro to the mid $1.05 mark and the lowest level since October 2023. The ECB meeting minutes all but confirmed policy makers preference for continuing to cut interest rates as early as next month. Markets are certain of it and are pricing in a hundred percent probability of policy easing in December. Inflation is seen as a diminishing problem as growth concerns rise to the top of the agenda. Trump’s election, the prospects of tariff wars and the fallout of the German governing coalition have raised the stake for policy makers.

To make matters worse, industrial production fell by the second-most this year in September, declining by a full 2% on a monthly basis. Manufacturing production in particular has only been positive once since the beginning of 2023, looking at the annual change. The European industry is clearly suffering and lower rates going into next year will be appreciated.

It will be different for the euro, though. Headwinds continue to push the currency lower and without any clear upside catalyst, bears will likely remain in charge.

UK growth slows over summer

George Vessey – Lead FX Strategist

After rebounding from a 4-month low near $1.26 towards $1.27, the pound gave up some of its recent gains against the dollar following UK GDP data this morning. The UK economy ended the summer on a weak note with an unexpected contraction in September, leading to an expansion of just 0.1% in the third quarter.

The dominant services sector grew by 0.1%in Q3, while construction grew 0.8%, but production fell by 0.2%. The figures mark a disappointing start for the new Labour government, which had promised to boost annual growth to 2.5% and the fastest in the G7. Hanging over Britain’s economic prospects is the threat of a new wave of protectionism amidst the US election result. However, the macroeconomic impact on the UK is expected to be limited as the US had a goods trade surplus of $10.5bn with the UK in 2023. In addition, the UK accounts for just 2.1% of US goods imports. Thus, the UK could be well down the list of priorities for the new US administration.

Sterling may still struggle to recover back towards $1.30 versus the dollar any time soon though, reflecting tighter US monetary policy as a result of the inflationary impact of tariffs. Moreover, the pro-cyclicality and risk sensitivity of sterling makes it vulnerable to risk off conditions and market corrections. With equities and bitcoin losing steam at the end of the week, safe haven demand should keep the dollar supported.

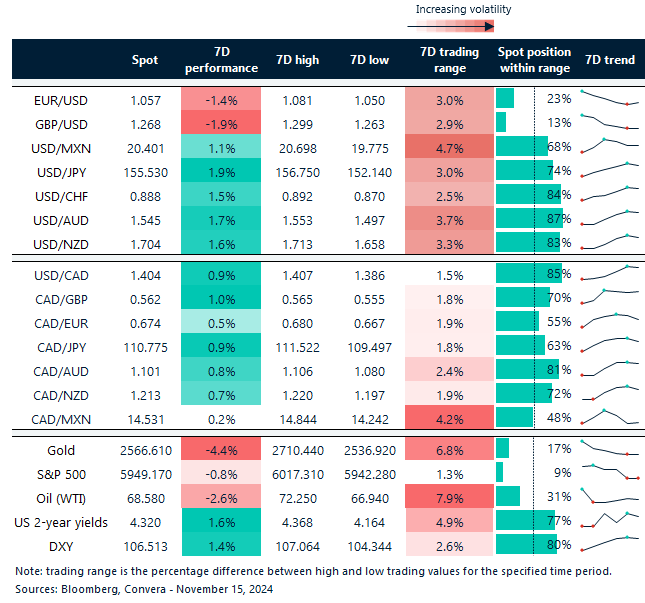

Dollar and yields in top 20% of short-term range

Table: 7-day currency trends and trading ranges

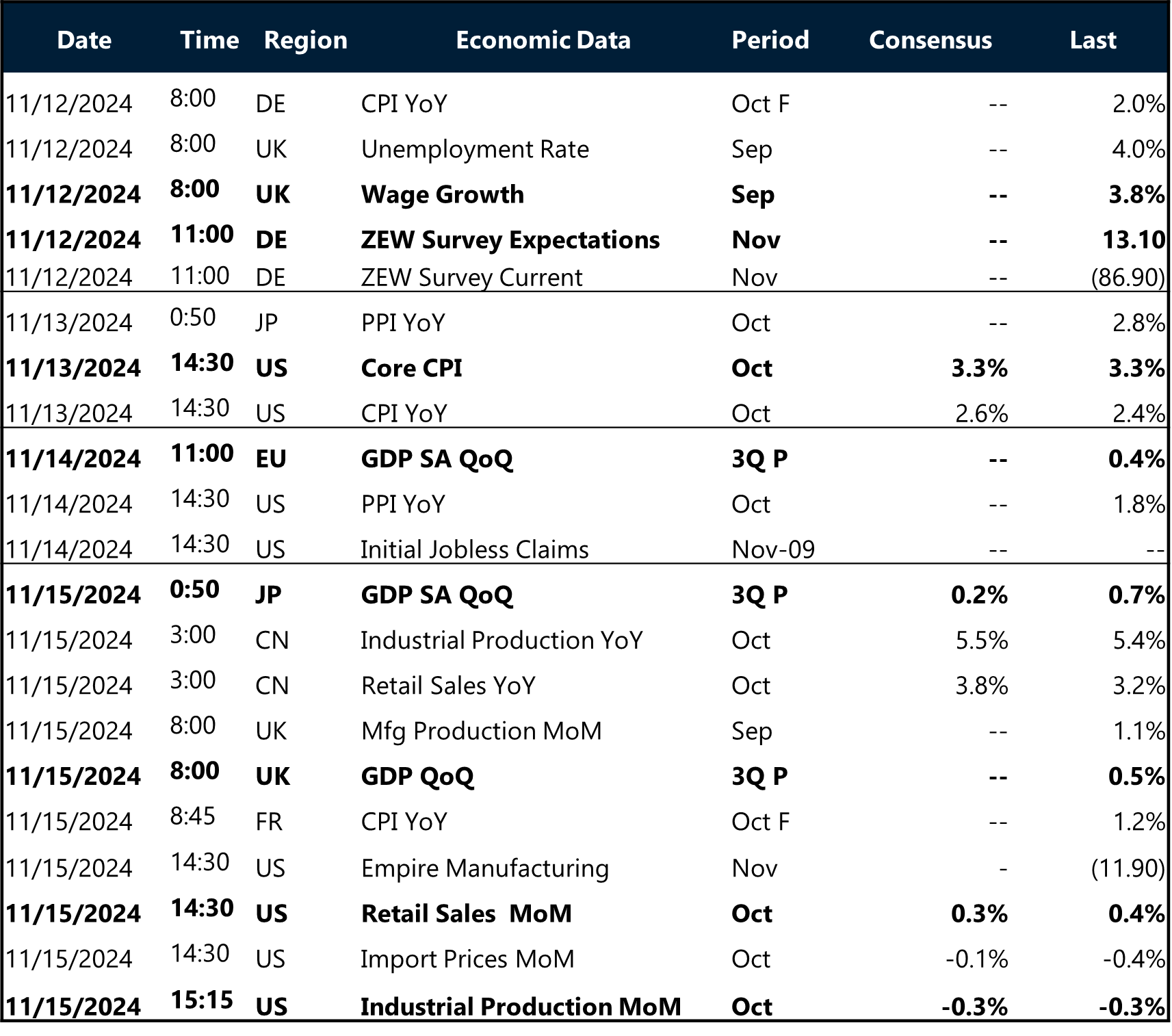

Key global risk events

Calendar: November 11-15

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.