Pound tumbles as UK inflation cools

Sterling is down across the board this morning, breaking back below $1.30 against the US dollar and slipping towards €1.15 against the euro following below-forecast UK inflation data. It’s the first downward surprise since January and the biggest since July 2021. This is a blow for hawks advocating another 50-basis point Bank of England (BoE) hike in August, which had helped GBP/USD climb to 16-month highs earlier this month.

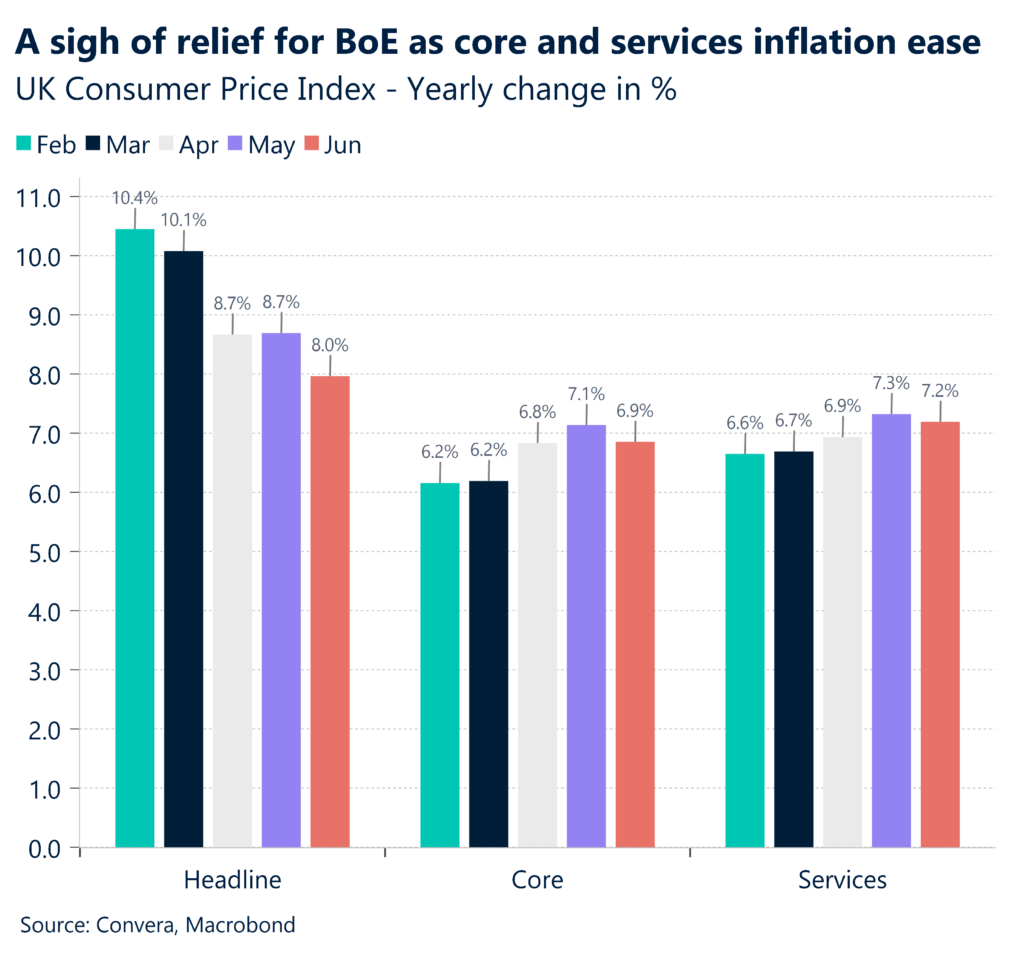

The headline UK Consumer Prices Index (CPI) was 7.9% higher than a year ago in June, a sharp drop from the 8.7% reading in May and more than the 8.2% consensus forecast. Core CPI also fell to 6.9% from 7.1% and services inflation, which the BoE is most interested in, fell to 7.2% from 7.4%. Importantly, the share of items in the UK inflation basket rising at a rate at or below 2% also climbed from 19% to 26% in a sign that soaring interest rates may be starting to curtail the worst wage-price spiral in the G7 nations. That said, over 30% of components are still rising at a rate above 10%, and both headline and core remain well above the BoE’s 2% target. Hence, we still expect the BoE to hike next month, but a smaller 25-basis point may be more likely now, with money markets pricing the probability of a 50-basis point hike at around 30% now, down from 70% yesterday, which is weighing on sterling.

As noted at the start of the week, GBP/USD had stretched into overbought territory and CFTC data showed the net GBP long position rose to its highest since 2007, indicating an overcrowded bet on the pound appreciating further. Although falling inflation is good news for the UK economy, it dents the pound’s appeal due to falling rate expectations and gilt yields, which has been the main driver of the pound’s fortunes in 2023. We note that since Brexit, the pound has spent more than 50% of its time below $1.30 against the US dollar. Despite the currency pair correcting back under this key threshold and the near-term risks pointing lower, the extended weakness in the US dollar expected over the second half of the year means we cannot rule out fresh 2023 highs over the coming months.

The end of the cycle is near

The incoming macro data continues to reinforce the argument for the Federal Reserve (Fed) to increase its benchmark interest rate by 25 basis points at next week’s meeting. Money market pricing for the Fed’s decision in July was little changed after yesterday’s data releases, with investors putting the probability of a rate hike at 97%. This has supported the dollar somewhat in the recent sessions, with the trade weighted US Dollar Index having found a temporary bottom just below 100.

While the economic data so far this week has been mixed, the overall picture remains one of resilience and strength. Headline retail sales rose less than expected (0.2% m/m) but core sales compensated for that (0.6%). Industrial production fell for a second month by 0.5%, driven by weaker durable goods production. The Blue Chip economist consensus for US GDP growth for the second quarter has continuously been revised up over the last few months and is currently forecasting the US economy to grow by 1.1% in Q2. The Atlanta Fed GDP now estimate real GDP growth at 2.4%, well above any reading that would indicate a recession.

So, while leading indicators like the purchasing manager indices and the Conference Board’s Leading Indicator point to much slower growth ahead, hard data has so far outperformed expectations. However, given the large weight of inflation in the policy debate and the disinflation as of late, stronger data has not been supporting the Greenback. Investors have continued to focus more on inflation than macro data, pricing in the end of the Fed’s tightening cycle in July and pushing up EUR/USD above $1.1250 in the process.

ECB is coming around to our inflation view

The most hawkish members of the ECB’s Governing Council are coming around to the fact that economic activity and headline inflation have slowed. In a volatile macro environment, which central banks try to maneuver by being as data dependent as possible, pre-committing to any rate decision one or two months beforehand cannot be justified. This is why European policymakers have recently softened their tone and have broadly descripted the rate decision in September as being open and dependent on the incoming data.

Economists and markets continue to expect the ECB to increase its benchmark interest rates one more time after the upcoming July hike. However, a tightening in September should not be taken as a given. Dutch central bank governing Klaas Knot put the euro under pressure a bit, after saying that it looks likely that the ECB would hit its 2% inflation target in 2024 and that hikes beyond July would be possible, but not a certainty. Knot has now been the second policymaker going on record this week questioning the ECB’s latest forecasts of inflation only returning to target in 2025. This supports the thesis we have laid out following the release of the forecasts back in March. Namely, that the ECB is overestimating the disinflation that will start to accelerate in the second half of the year.

EUR/USD reached the highest level since February 2021 in yesterday’s trading, rising as high as $1.1270. Since the release of the US data and Knot’s comments, some upside pressure has come off. The currency pair is now hovering around the $1.12 mark, with the next catalyst being the final Eurozone inflation print for June and US housing data.

Pound surrenders recent gains

Table: 7-day currency trends and trading ranges

Key global risk events

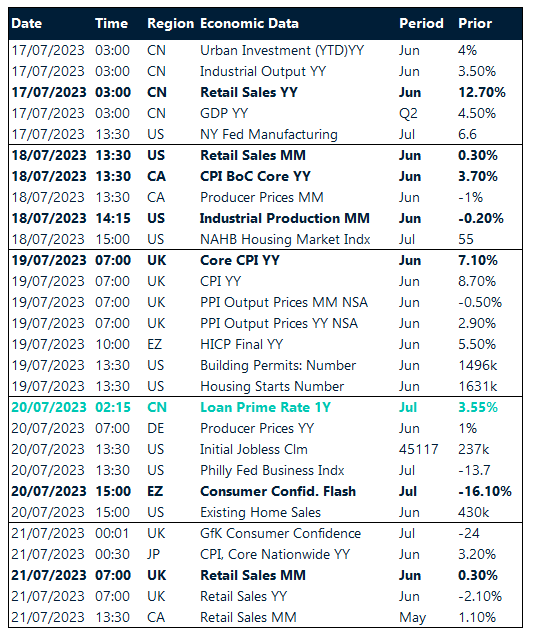

Calendar: July 17-21

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.