Aussie leads losses after new Trump threat

Global markets tumbled on Friday as US president Donald Trump announced new 100% tariffs on Chinese imports starting from next month.

Trump hit back after earlier moves from China that saw new port fees on US ships, an antitrust investigation into chip-maker Qualcomm and restrictions on rare earth exports.

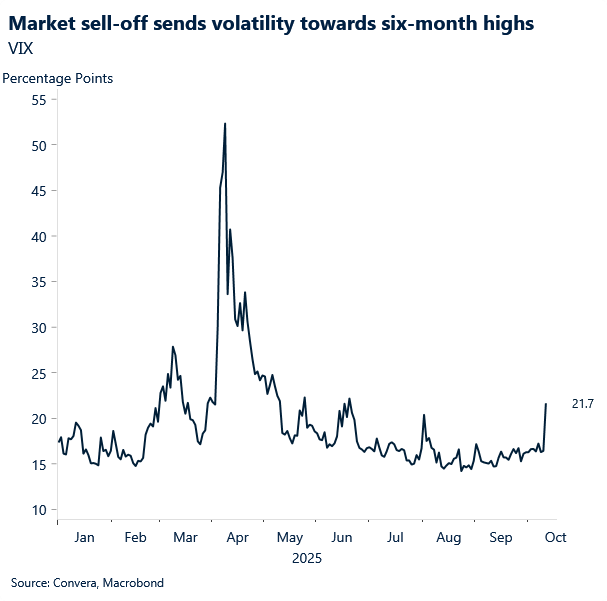

US shares were smashed lower with the S&P 500 down 2.7% and the tech-focused Nasdaq lost 3.6%. In commodity markets, gold gained 1.0% while oil dropped 4.2% as it fell to the lowest level since May.

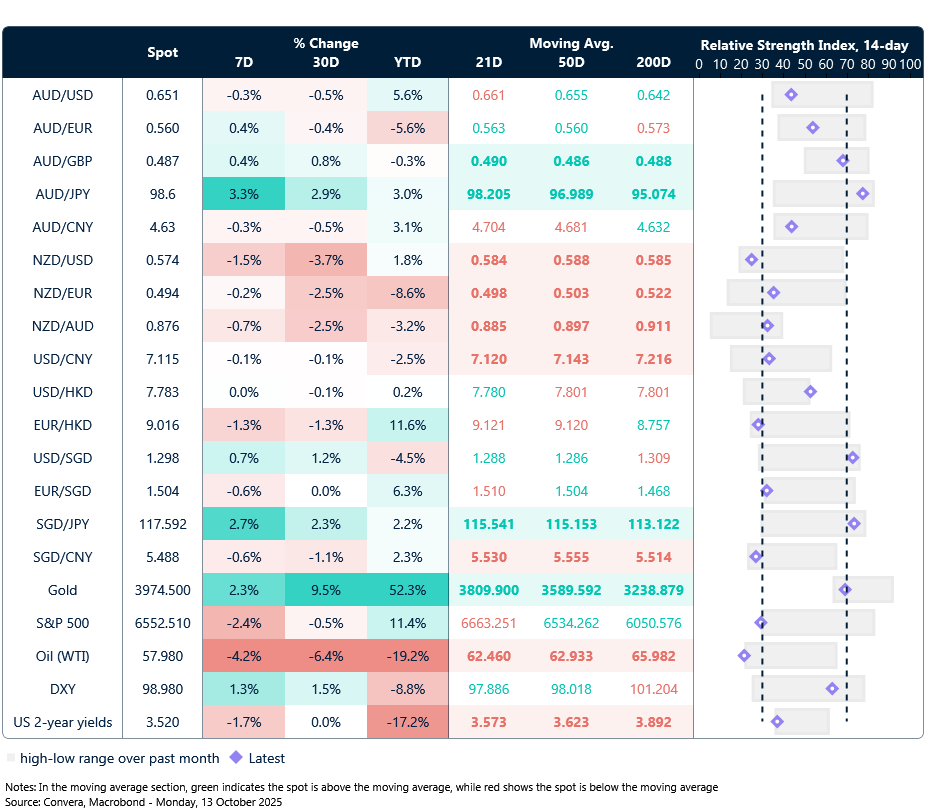

In FX, the AUD/USD led losses, down 1.3% and falling to six-week lows.

The NZD/USD lost 0.4% as it traded to new six-month lows.

In Asia, the USD/CNH gained 0.1% while the USD/SGD bucked the trend as the USD fell – the USD/USD dropped 0.2% as it reversed from the key 1.3000 level.

Takaichi pushes back on weak yen claims

Staying in Asia, Japan’s new LDP leader, Sanae Takaichi, dismissed suggestions that she supports a weaker yen, following a sharp drop in the currency after her election win.

“I have no intention of causing an excessively weak yen,” she said in a Japanese TV interview. “That said, a weaker yen has both pros and cons. For exporters, it can act as a cushion—especially with ongoing concerns about Trump’s tariffs.”

Any dips in the yen might be brief, with the 155 mark seen as a critical threshold that could prompt officials to step in with strong words.

Still, traders are watching key technical levels, with support seen around 21-day EMA of 149.53, followed by 50-day EMA of 148.41.

China trade, Singapore GDP the early focus

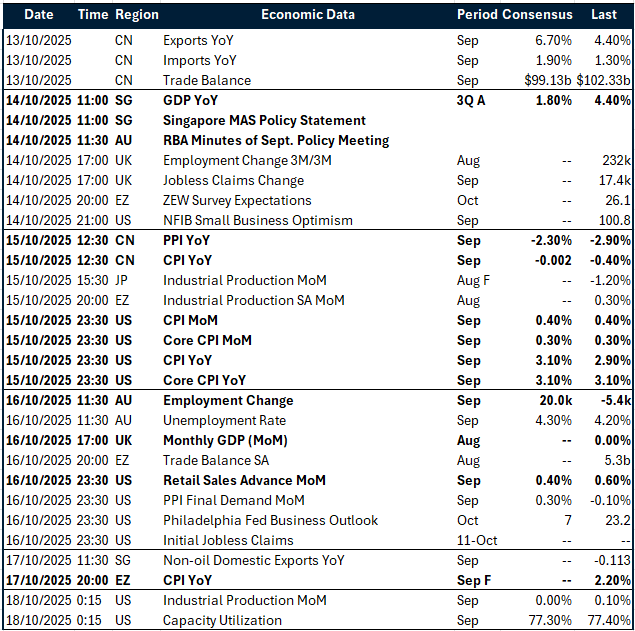

A busy data calendar awaits this week despite the US government shutdown.

The week opens in Asia with China’s September trade data, expected to show firmer exports (+6.7% YoY) but a shrinking surplus, setting the tone for global sentiment. Singapore’s Q3 GDP is forecast to slow (+1.8% YoY), alongside the MAS monetary policy announcement which is key for SGD and regional markets.

RBA minutes on Tuesday and Australia’s September jobs report (Thursday; employment +20k, jobless rate 4.3%) will be closely parsed for any dovish tilt as Australia’s labour market cools.

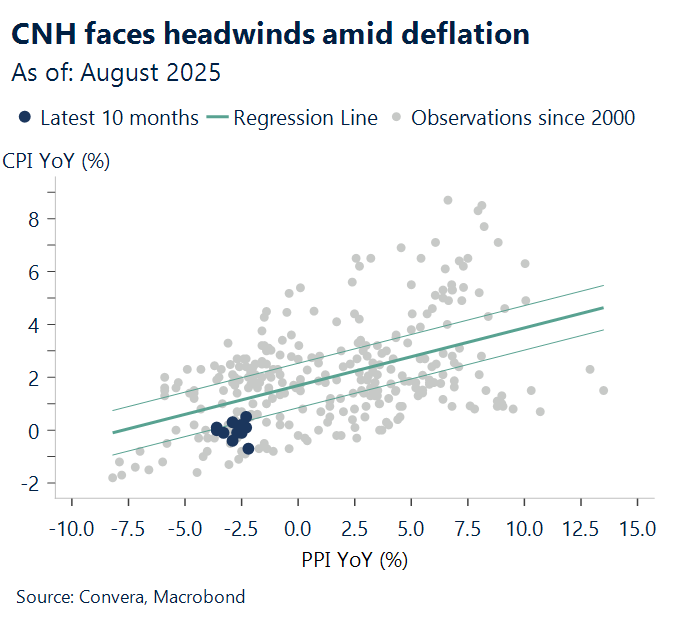

China’s CPI (Sep: -0.2% YoY) and PPI (-2.3% YoY) on Wednesday will be watched for persistent deflation risk. On Thursday, US inflation (CPI Sep: 3.1% YoY; core 3.1%) takes centre stage, anchoring Fed expectations and USD moves. Eurozone and French final CPI prints wrap up the inflation focus in that week as well.

UK labour data (Tuesday; wage growth, unemployment) and monthly GDP (Thursday) will gauge the pound’s resilience. US retail sales (Sep: +0.4% MoM), PPI (+0.3%), and sentiment surveys (NFIB on Tuesday, Philly Fed on Thursday) offer insight into consumer strength and business outlook. Eurozone industrial output and trade readings will further inform on recovery momentum.

Aussie hit hardest

Table: seven-day rolling currency trends and trading ranges

Key global risk events

Calendar: 13 – 18 October

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.