Written by Convera’s Market Insights team

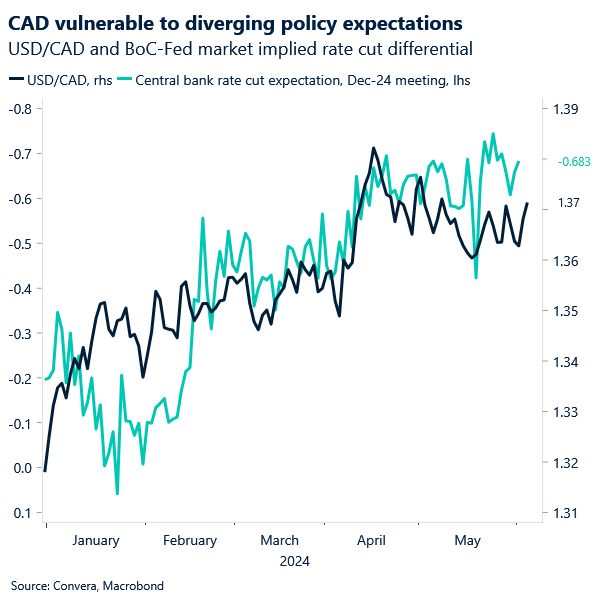

Bank of Canada cuts, swayed by disinflation

The US services sector expanded by the most in nine months, according to the Institute for Supply Management. The barometer jumped by more than four points to 53.8, indicating a clear growth rate going into the month of May. The employment sub-category contracted by less than last month but has remained below the important 50 mark for four consecutive months. The big push higher on the headline level had been driven by both production and new export orders printing above 60 readings.

The main event, while still in North America, came from the other side of the border. The Bank of Canada (BoC) cut its benchmark interest rate by 25 basis points to 4.75%. It was the first policy easing since 2020 and it took policy makers less than a year to go from hiking to cutting rates. The move came after the core inflation rate fell below the institution’s 2% target in April for the first time since inflation began moving upwards in 2021. Markets pricing in more rate cuts was also been supported by the remarks from Governor Tiff Macklem emphasizing the plausibility of continued policy easing. However, this might revitalize the housing market and prop up consumer confidence, which could indirectly add to the already rising global inflationary impulse, meaning that the pace of policy easing could be limited going forward.

USD/CAD climbed on both Tuesday and Wednesday, but the currency pair remains somewhat range bound between $1.35 and $1.38. For that reason, our attention turned to EUR/CAD rising to just shy of €1.4920 and reaching the highest level this year. The Canadian dollar especially underperformed the pound as GBP/CAD pushed to a new two-and-a-half-year peak. The North American economic calendar will put focus on US trade data and the Canadian Ivey PMI today.

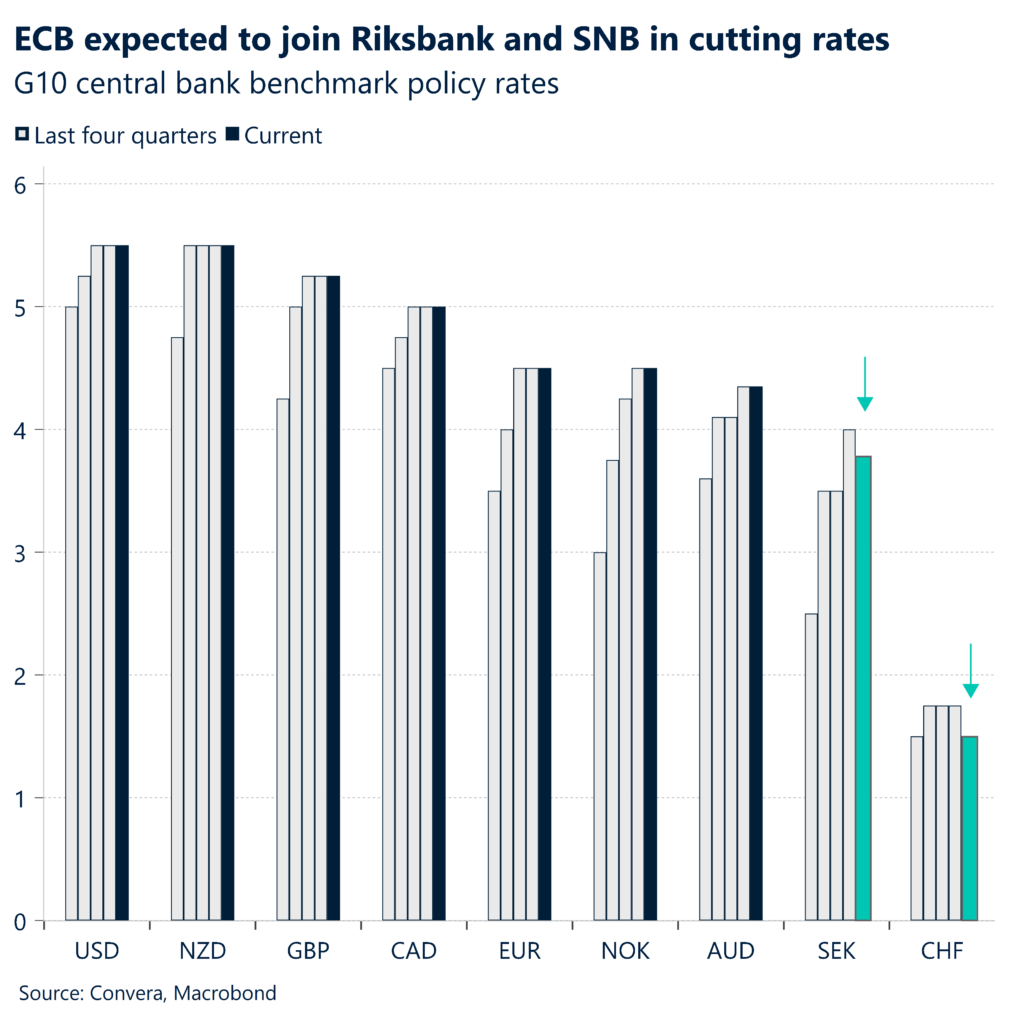

ECB rate cut expected

European stocks looked set to rise ahead of a widely-expected interest rate cut by the European Central Bank (ECB) as markets reassessed bets of policy easing this year.

The euro extended its losses from Tuesday to a second straight day just before the ECB is expected to cut interest rates for the first time in five years. The European currency is still in positive territory on a weekly basis from its gains made on Monday. Government bond yields in Europe continue to trend lower with the German 2-year yield breaching the 3% mark for the first time in two weeks. The economic week has been lacking any meaningful data from the continent with investors focusing mainly on US releases in the form of labor market data.

This has also meant that the expectations of the ECB delivering policy easing today supported European equities with the Stoxx 600 being less than 1% away from its record high reached in May.

Risk appetite buoyed, equities up over 2%

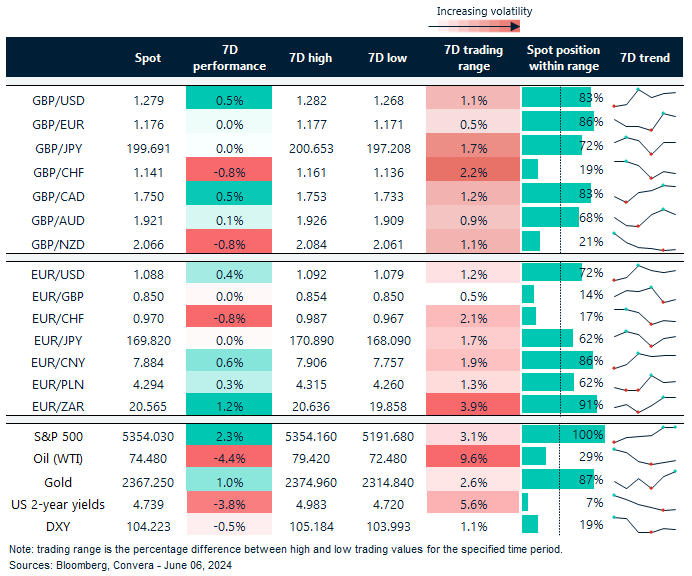

Table: 7-day currency trends and trading ranges

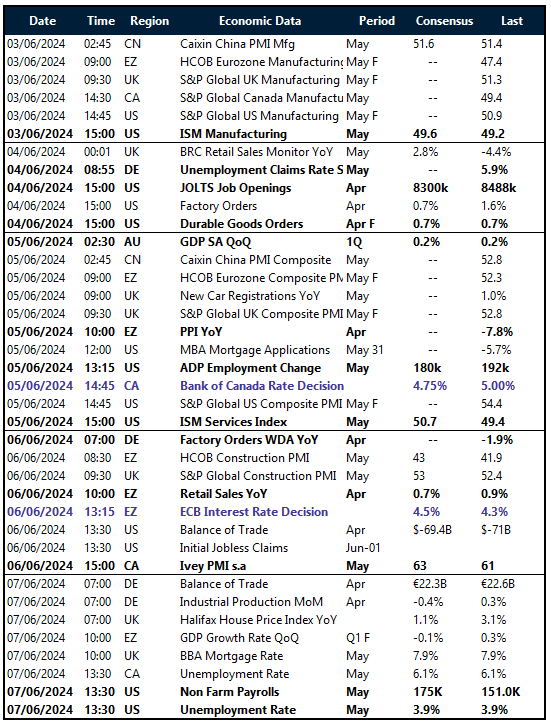

Key global risk events

Calendar: June 3-7

Have a question? [email protected] *The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, o