USD: A healthier dollar, until the shutdown withholds the cure

The dollar opened the week on a firmer foot, building on late last week’s rebound as a re‑energised macro narrative (Fed’s hawkish tilt and Kevin Warsh’s nomination) and a much‑needed washout of overstretched short‑USD technicals restored some support for the currency. The fundamental backdrop was reinforced by yesterday’s strong ISM manufacturing PMIs. Activity expanded in January at the fastest pace since 2022, driven by gains in new orders and production. The report suggests that January’s geopolitical turmoil did little to disrupt what now looks like a clear shift in the previously stagnant manufacturing momentum through most of 2025. So certainly great news, but part of the surge can be blamed on renewed tariff tensions, which prompted firms to pile in orders now to avoid any future inflationary spike tied to it. And of course, January always brings a wave of order‑refilling after the post‑Christmas depletion of pipelines.

Also, a note on the Warsh‑fuelled bullish reaction in the dollar: the move reflects that hawkish historical memory markets still hold of Trump’s pick, but they will quickly shift toward parsing Warsh’s future communication for any deviation from that legacy. The nomination is dollar‑positive for now, but the durability of that support will depend on how his messaging evolves.

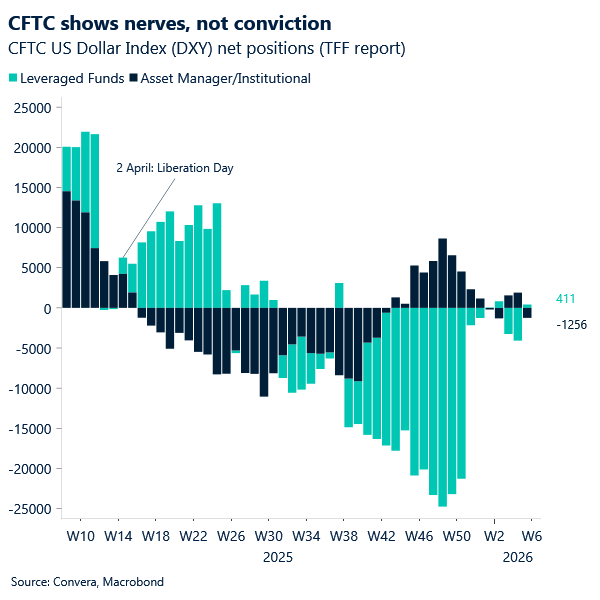

With all of this in mind, CFTC positioning from last week is instructive. The small net directional biases highlight investors’ reluctance to commit meaningfully in either direction. That said, compared with April, leveraged funds have behaved more tactically – selling the dollar aggressively during bouts of DC‑driven policy uncertainty, then rebuilding long exposure ahead of key events such as last week’s FOMC meeting. In fact, the latest snapshot (as of 27 January, the day before the Fed’s policy meeting) shows – albeit still narrow – net long USD dollar positioning, marking a clear reversal from the previous two weeks when those short bets had been piling in. In April 2025, by contrast, speculators were slower to move net short USD, only joining institutional accounts months later.

These spreads remain tight, and more data is needed to determine whether the resilient US macro story can pull both speculators and longer‑term investors toward a more sustained bullish USD stance.

That said, that will certainly not happen this week, as a second partial government shutdown is set to delay this week’s labour‑market data (with the exception of ADP tomorrow). The shutdown, although smaller in scale, is now in its third day, with Democrats continuing to demand immigration reforms as part of any funding agreement to reopen the government. The package has cleared the Senate but still requires approval from the House of Representatives before it can be sent to President Trump for signature. While a resolution appears imminent – as early as today – the absence of key data this week leaves the dollar without fresh catalysts, and today’s softer start may reflect a clear stalling as investors wait for more economic signals.

EUR: Euro stuck under the US shadow

The euro remains at the mercy of developments across the Atlantic. It bled against the dollar yesterday but was broadly flat against the rest of G10. A clear shift toward a risk‑on mood made EUR/CHF stand out, rising as CHF’s risk‑off January gains were unwound.

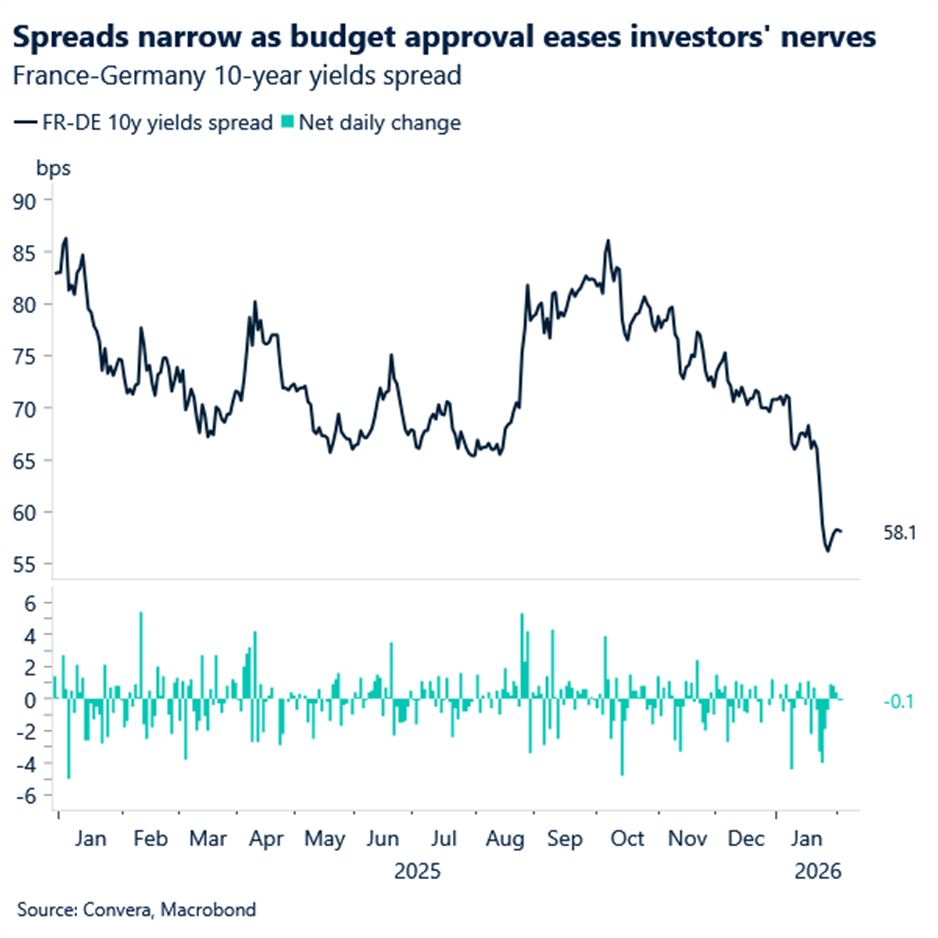

On the domestic front, we heard that the 2026 French budget has been adopted, after turbulent months of shaky politics that saw the government collapse twice in the space of a month. Prime Minister Lecornu can now take a breather, having survived two no‑confidence votes, and bringing a period of relative calm as the focus now shifts onto municipal elections in March and the presidential vote in spring 2027.

Unsurprisingly, the euro remains unresponsive to such developments, though we read the news as constructive given last year’s hit to euro sentiment on this topic.

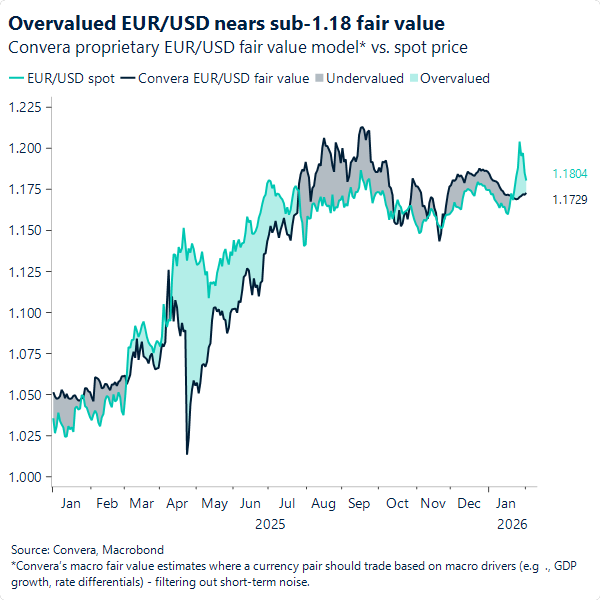

EUR/USD continued grinding lower, showing an inclination to re-enter sub- 1.18 levels, which we have repeatedly flagged as our strongly favoured view. While the lack of US data this week may delay a below-1.18 push, we expect EUR/USD to consolidate in the 1.16–1.17 zones in the next few weeks, with our short-term fair value pointing toward the lower bands of the 1.17 zone.

GBP: GBP/EUR pops on technical break and BoE calm

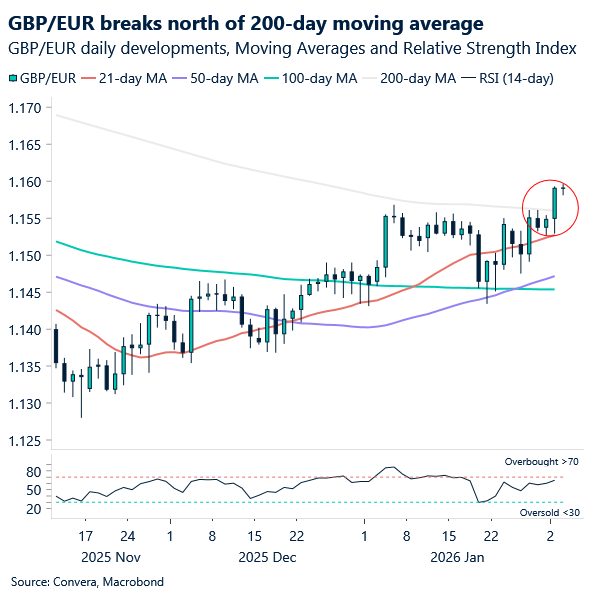

Sterling enjoyed a return to the risk‑on mood yesterday, with the currency broadly bid across G10, with the notable exception of the US dollar. GBP/EUR’s moves were particularly instructive. The currency’s pro‑cyclical nature boosted demand, and this was reinforced by a compelling technical break. The pair had repeatedly tested resistance at 1.1550 throughout December before finally pushing above it yesterday, followed by a break of the 200‑day moving average at 1.1560, which had held since sterling’s slide against the euro in December 2024. Also, as we approach the BoE’s first policy meeting of the year (Thursday), with the MPC expected to keep rates unchanged and the data picture largely steady since the last meeting in December 2025, sterling buyers likely felt more confident as near‑term bearish risks from a dovish shift at the Bank appear limited.

Overall, it remains a low‑probability scenario for more than two officials – Alan Taylor and Swati Dhingra – to dissent against holding steady, but we do see a risk of sterling being pressured lower later in the week if there is a more robust dissenting push. We favour nonetheless an above-1.1550 posture in GBP/EUR for the reminder of the week.

Meanwhile, the pause in major US data releases this week implies that any more meaningful bearish impulse for GBP/USD may be limited, with support at 1.36 – followed by the 21‑day moving average in the mid‑1.35 zone – unlikely to fade just yet.

Market snapshot

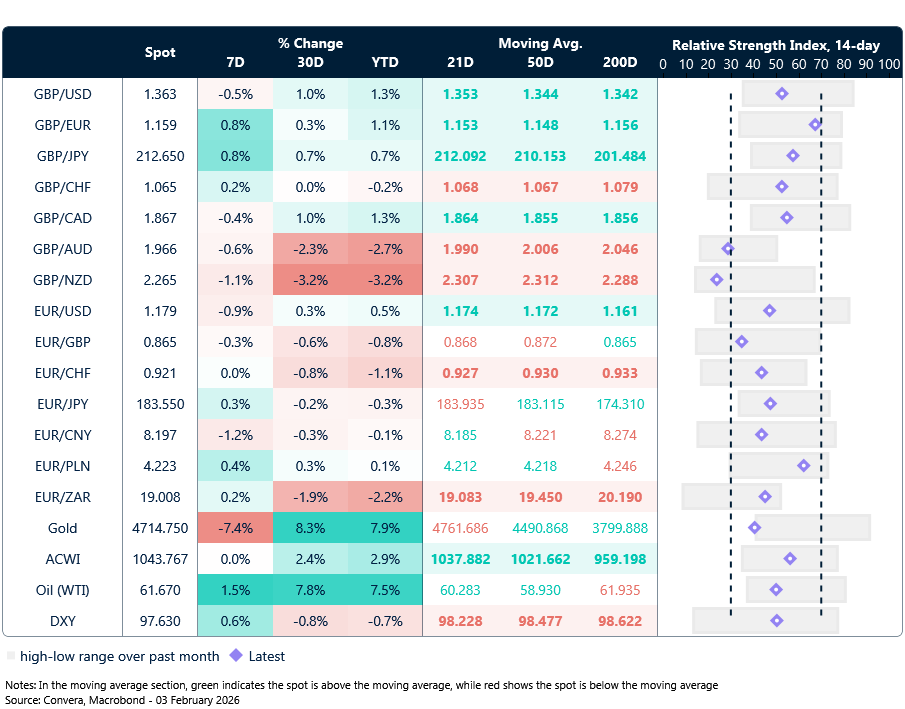

Table: Currency trends, trading ranges & technical indicators

Key global risk events

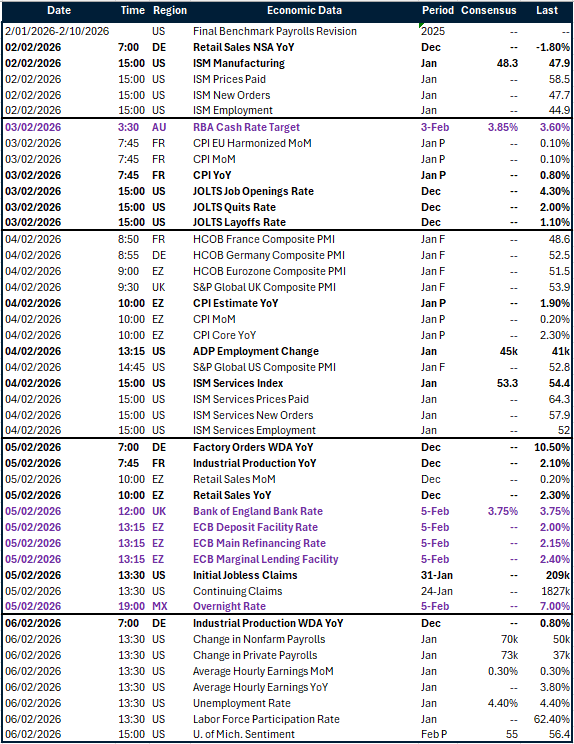

Calendar: February 2-6

All times are in GMT

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.