Written by Convera’s Market Insights team

Risk aversion supports low yielders and safe havens

George Vessey – Lead FX Strategist

In a continuation of last week’s market trends, there is a sea of red in Asian share markets with Japan’s Nikkei 225 Index dropping 12% on Monday. Futures on the US’s tech-heavy Nasdaq 100 point to a loss of almost 6%, while S&P 500 contracts were down 2.8%. Euro Stoxx 50 futures were down some 2.5%. The global equity sell-off is being driven by fears of a US recession after the first broad-based weakness across the US employment report on Friday. The rapid unwind of carry trades also continues, helped by the Bank of Japan hiking interest rates and as FX volatility increases.

Last week marked a potential inflection point in global data. The notable softness in manufacturing surveys – including from China and the US ISM report, whilst the world’s biggest economy had added just 114,000 jobs in July, far fewer than the 175,000 that were expected. This has sparked fears the Federal Reserve (Fed) risked falling behind the curve in combating a slowing economy. US bond yields tumbled, with the 10-year yield sinking to its lowest since December as markets aggressively shifted to pricing in a 50-basis point Fed rate cut next month and up to five Fed rate cuts in total for 2024. The key takeaway here is that markets are flirting with the idea of a US recession and although risk aversion should further benefit low yielders like the Japanese yen (up around 4% against majors today) the US dollar’s safe haven appeal means it’s holding up well against high beta currencies.

Popular positions from yen carry trades to crypto are being dumped in a rush to the exits, with volatility spiking and liquidity drying up. The upcoming week lacks real risk events apart from the ISM services PMI report and SLOOS survey in the US, meaning that the risk negative flows caused by the weakening of macro data could linger around for some time.

Pound sensitive to global sentiment

George Vessey – Lead FX Strategist

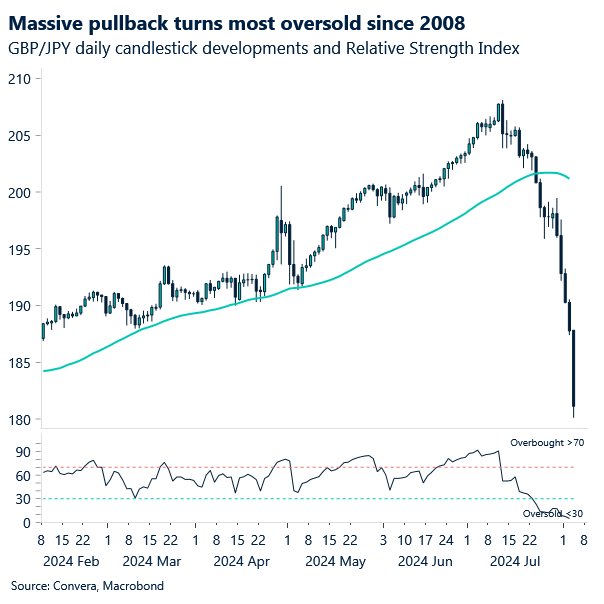

The pound’s high sensitivity to risk asset performance was in evidence last week despite a fairly hawkish first cut by the Bank of England (BoE). GBP/USD is grappling to stay afloat its $1.27 support level, whilst GBP/EUR has dipped below €1.17 for the first time since May. But it’s the Japanese yen stealing the show, with GBP/JPY down an eye-popping 13% since mid-July, 10% of which has occurred over the past week alone.

Markets were pricing a 60% probability of a BoE rate cut to 5%, and the BoE’s Monetary Policy Committee (MPC) voted 5-4 in favour to deliver it last Thursday. Although there was a hawkish tone limiting the pound’s initial losses, we did see gilt yields extend to fresh 1-year lows and markets price in more rate cuts by the BoE this year. However, it’s the global equity sell-off and unwinding of once popular carry trades that have hit sterling the hardest over the past few days, highlighted by the plunge in GBP/JPY – erasing all of its year-to-date gains in just a few weeks.

GBP/JPY has fallen well over 10% in the last couple of weeks – a huge move when compared to the last events triggering such moves over the past 8 years. We can’t rule out a pullback given the 14-day Relative Strength Index is the most oversold since 2008, but with FX volatility on the rise, the current conditions remain constructive for low yielders like the yen and destructive for high beta currencies like the pound.

Euro salvaged by US NFPs

Ruta Prieskienyte – Lead FX Strategist

The euro surged past the $1.09 threshold on Monday as weak US NFPs and higher US unemployment rate rattled the markets. Meanwhile, EUR/JPY experienced its worst monthly decline in eight years (-5.8%), while EUR/GBP declined for the fifth consecutive month in July, marking the worst streak since January 2020. Despite this poor performance, the euro rallied to a 1-month high by the end of the week, a delayed reaction to the hawkish Bank of England decision last Thursday.

Bund yields have sharply declined, with the Bund yield curve shifting down across all maturities, shedding ~20bps across the 2y-10y part of the curve. This trend is not only attributed to last week’s Eurozone macro data but also reflects a broader global trend of lower yields. Investors are starting to price in a greater probability of ECB easing this year and are becoming more aware of rising risks to the growth outlook. While the ECB’s focus remains on inflation, any shift towards recognising growth risks will likely result in euro depreciation. The market has already moved to price in an additional 10bps of easing by the end of 2024, expecting between 2-3 additional rate cuts versus 2 at the start of the week.

The economic calendar is light this week. Key agenda items will include final PMIs, Sentix Investor Confidence, German factory orders, and European retail sales. We are entering a seasonally quiet period not just for data but also for ECB speakers. Given how poor Eurozone activity indicators have been over the past two months, this quiet period might be beneficial for the euro, which has shown a strong positive correlation with a fall in realised FX volatility.

GBP/JPY down 10% in a week

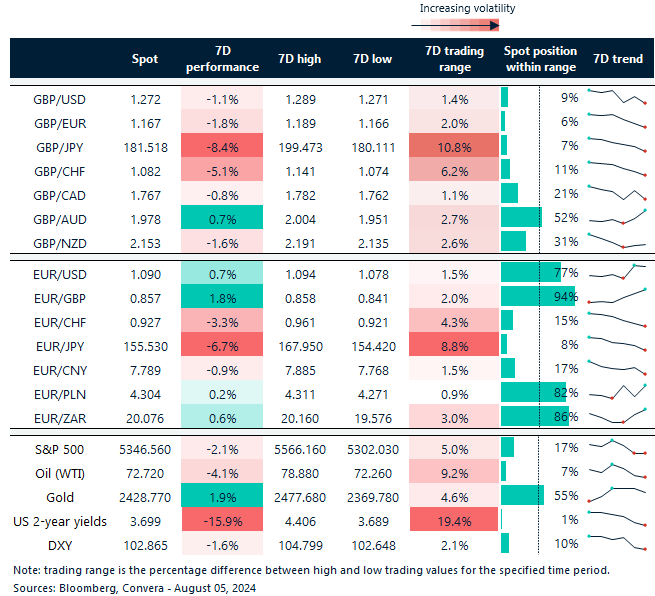

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: August 05-09

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.