USD: Out of breath above 99

Dollar momentum softened, dipping below the 99 handle. This was broadly expected, as sentiment in France and Japan improved following a politically turbulent week, with steady progress on both fronts. Given the significant weight of these two currencies in the DXY basket, the index was mechanically dragged lower. Meanwhile, the move wasn’t driven by any distinctly USD-bullish catalyst, but rather by growing resilience against bearish pressures – also partially sedated by the ongoing shutdown.

Yet the greenback faced broad-based weakness yesterday, initially driven by dovish-leaning remarks from Powell, and later reinforced by the release of the Beige Book – an anecdotal survey on the state of the US economy – which cemented the Fed’s openness to further rate cuts amid slowing economic momentum.

Meanwhile, markets seem to have largely shrug off trade tensions for now, with the upcoming meeting between the two leaders seen as intact, and hopes building for amicable negotiations. That meeting is scheduled just days before a 100% tariff on Chinese goods is set to take effect (1 November), following Trump’s 9 October decision. Scott Bessent helped here – reportedly floating yet another China truce, perhaps longer this time, if China agrees to halt its plans for strict new export controls on rare-earth elements.

The dollar may struggle to hold above the 99 handle in the next couple of weeks, now that sustained upside grows dependent more on its own fundamentals than on politically bruised peers. That said, we continue to hold that while the Fed cut rates in September and may do so again at least once more this year, the priced-in easing path, coupled with the cautious forward guidance adopted since Trump’s second term, is likely to cap any meaningful dollar downside.

On a final note, the big US banks had a stellar week, unveiling Q3 earnings that trounced analysts’ expectations. Amid a lack of fresh economic data, such news underscores underlying economic resilience – soothing trade fears.

For today, keep an eye on rate-setters, particularly the likely contrast between Waller and Bowman. Amid ongoing data silence, Bowman’s cautious – yet well-justified – tone may undercut Waller’s familiar labour market warnings, engaging no meaningful dollar price action.

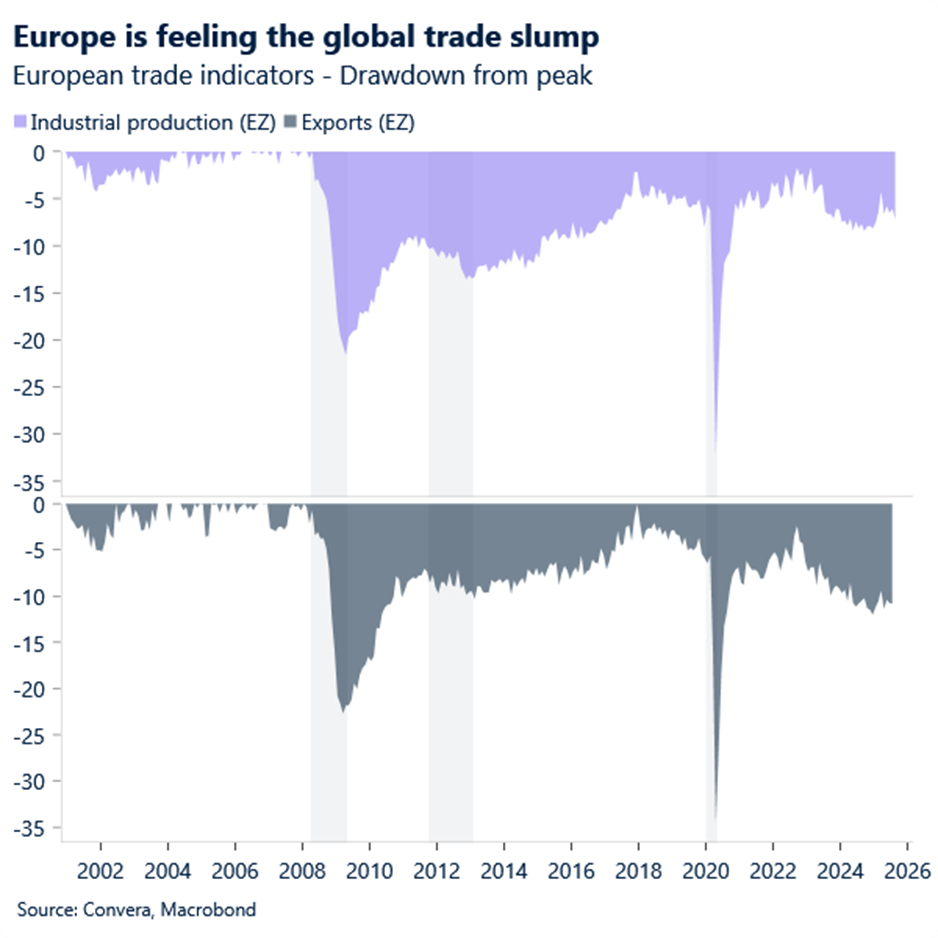

EUR: Soft data keeps piling up

The euro area continues to deliver disappointing macro prints. Eurozone industrial production fell 1.2% month-on-month in August, following a modest 0.3% rebound in July – marking the lowest level since January. This contrasts with earlier PMI data, which had suggested a more optimistic outlook for August. At this softening pace, we expect manufacturing to contribute negatively to eurozone Q3 GDP growth.

This does little to shift market expectations of further ECB rate cuts – the central bank has clearly shown itself to be more swayed by inflation dynamics than by a weakening macro backdrop. Still, the evidence is noted and may tip the balance should inflation show persistently softer momentum than expected.

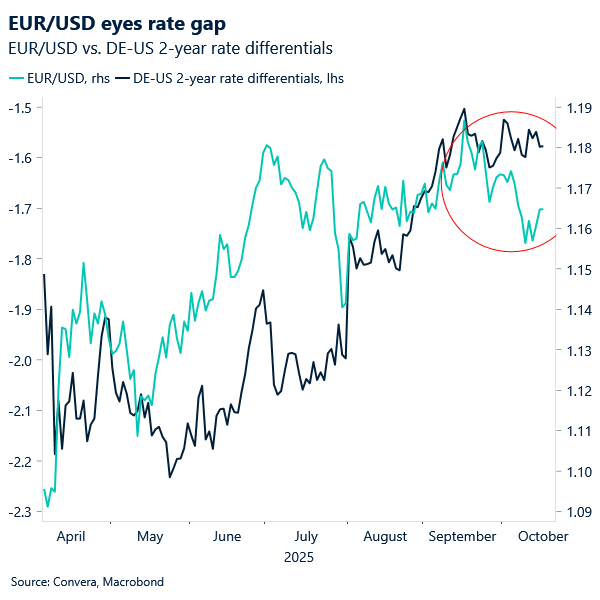

With little clear short-term USD-bullish drivers in sight, EUR/USD is likely to stay clear of the recently re-tested support at 1.1550 for now, with a gradual bias toward the 1.17 zone. That said, French Prime Minister Lecornu faces confidence votes today, which are likely to pass. We see this event as accelerating the euro’s ascent against the dollar. As noted before, on more dovish engagement by the Fed, we see EUR/USD comfortable at 1.18, suggesting that the current gap holds a strong sentiment-driven character, expected to be filled as the French political backdrop improves.

GBP: Shorts squeezed, risks remain

The UK resumed modest GDP growth in August, rising 0.1% in line with forecasts, following a rebound in manufacturing – putting the economy on course for some expansion in Q3. The data offers a welcome reprieve, even as earlier releases continue to paint a soft labour market backdrop. For the UK, these figures are viewed through the lens of the upcoming autumn budget, a structurally GBP-negative risk event, as the prospect of higher taxes on businesses and consumers casts a shadow over sentiment, growth, and sterling appeal.

Nonetheless, sterling has had a solid week against G10 peers so far. The heavy build-up in GBP short positioning over recent months tends to trigger short squeezes – even when data underwhelms, as long as it’s not catastrophically weak. On the labour front, in fact, slowing wage growth momentum – paired with more contained and broadly in-line declines in payrolled employees – suggests a less severe deterioration than feared.

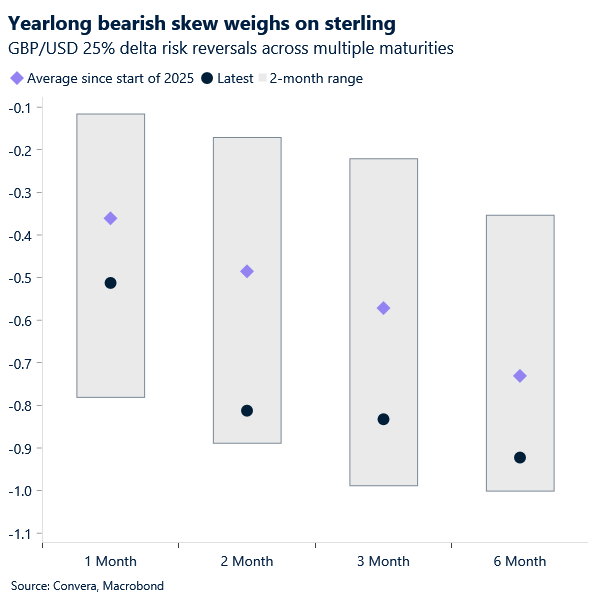

This helps explain the pound’s resilience across the board despite this week’s underwhelming data batch. Against the dollar, risk reversals – a barometer of currency sentiment – remain structurally skewed in favour of GBP puts, suggesting investors continue to seek protection against sterling weakness rather than bet on strength.

Sterling began the year burdened by a persistently recurring fiscal risk premium – one that, by its nature, reignites frequently throughout the year, especially around the spring and autumn budgets. Unlike a rate cut or hike, this risk is harder to fully “price in.” As a result, short squeezes remain a familiar feature of GBP price action, which embeds a structurally bearish bias, as seen again this week.

DXY rally softens

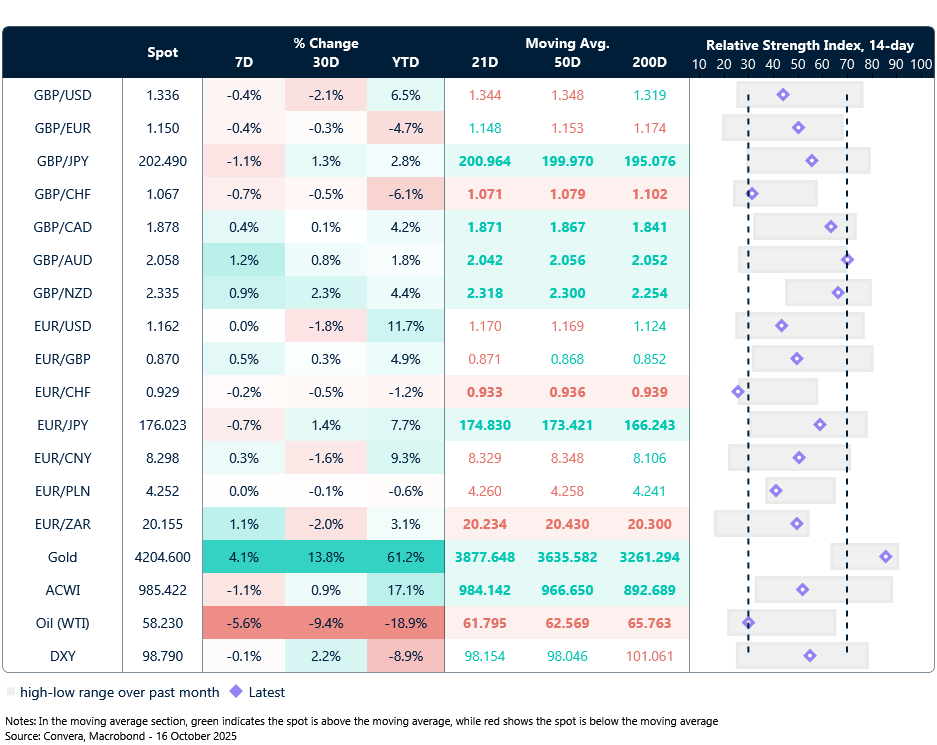

Table: Currency trends, trading ranges and technical indicators

Key global risk events

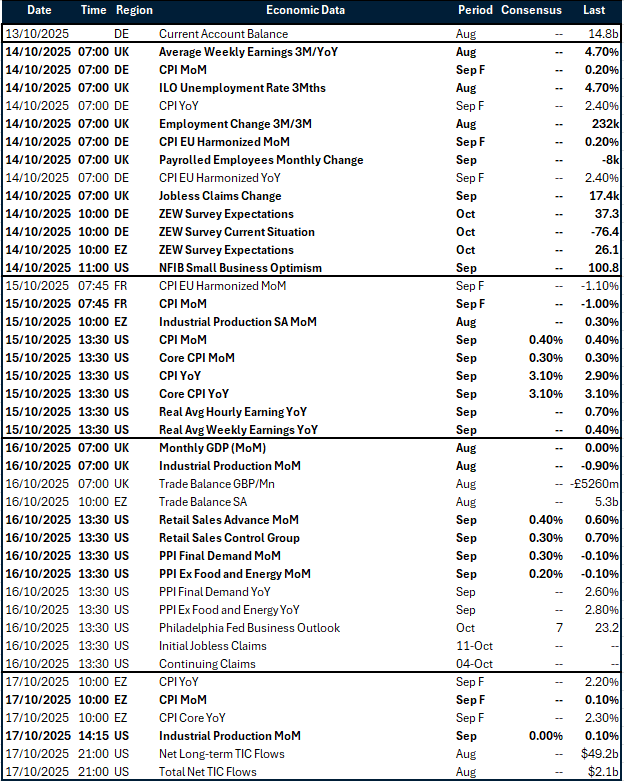

Calendar: October 13-17

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.