Global angst pushed euro below $1.08

Global investors are caught in a tug of war between strong economic data and rising yields in the United States and a weakening economy and lower interest rates in China. Europe has been in the middle of both worlds but has recently been leaning towards the east as the impact of the Chinese slowdown is starting to be felt more broadly.

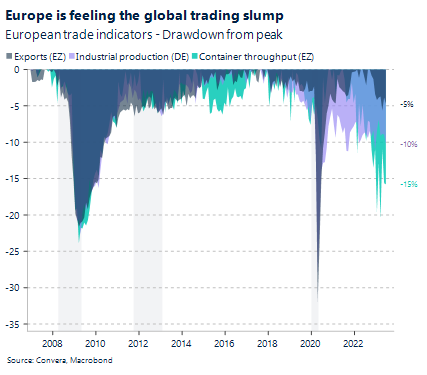

The Eurozone’s real GDP is just 4% above its pre-pandemic level, trailing China, and the US but ahead of Japan. However, the recent pull back from consumers has meant that both real retail sales and industrial production have returned back below 2020 levels, highlighting the difficulties to sustain reasonably strong growth rates. The Eurozone’s composite PMI fell from 48.6 in July to 47 in August and has now been negative for three consecutive months. While the manufacturing gauge did improve across the European member states, the fall of the services PMI more than compensated for the slight industrial recovery. The loss of momentum in August was confirmed by the German Ifo business sentiment, which disappointed expectations and fell the fourth month in a row. The slump is most visible in trade and pro cyclical indicators, with exports, industrial production, and container throughput down 5%, 10% and 15%.

European investors are going cautiously pessimistic into the new week. The disinflationary slide is expected to have continued in August with CPI coming up for Germany (Tuesday), France (Wednesday) and the Eurozone (Thursday). Last week’s release of German PPI set the stage, after producer prices fell by 6% in July, the first fall since November 2020 and the largest disinflation since 2009. The euro fell below $1.08 at the end of last week, setting a 10-week low. EUR/USD is going into the week with a slight negative bias, with the consensus seeing a US inflation rebound again.

The US macro trifecta to create volatility

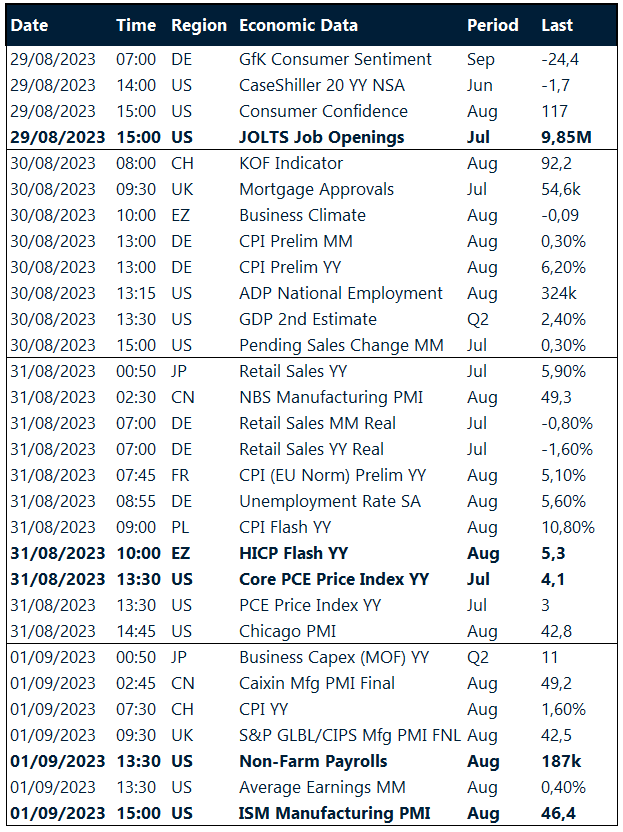

Every week featuring the release of the three most important data points in the United States, inflation (PCE) , job growth (NFP) and the purchasing manager index (PMI) is bound to be an exciting one. All three data points will be published on Thursday and Friday, creating volatility at the end of this week of acronyms. Fed chair Jerome Powell already created some tensions on markets with his remarks at Jackson Hole before the weekend, setting the stage for this week.

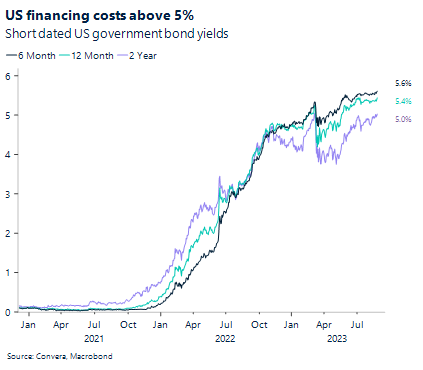

Powell emphasized the potential need to continue raising interest rates to fight inflation. The possibility of a rate pause in September has been suggested and is currently priced as the base case on financial markets, with options putting the probability of a pause at 80%. However, the president has been able to achieve two things. Expectation of a 25 basis point hike in November has, for the first time in multiple months, climbed above the 50% mark. Secondly, The first rate cut has been pushed out from June to July 2024. US 2-year government bond yields jumped above 5% following Powell’s speech and while longer dated bond yields did fall slightly on Friday, they continue to be close to 15-year highs. Against this backdrop, it is not surprising that the US Dollar Index has been able to record six consecutive weeks of increases. The gains have been mostly against the euro, yen, and yuan.

It is important to note that the Federal Reserve does expect some more disinflation in the pipeline to come from moderating housing, food, and energy prices. However, the resilience of the economy and core inflation rates has questioned the return of inflation to the 2% target. Looking at this week’s data might give us another hint at how likely that return will be. Economists are expecting the PMI for the manufacturing sector and inflation to have rebounded in August and July, respectively. The consensus sees a weakening of jobs growth to 170k, which could dampen the effect of the former two data points.

Light UK calendar shifts focus elsewhere

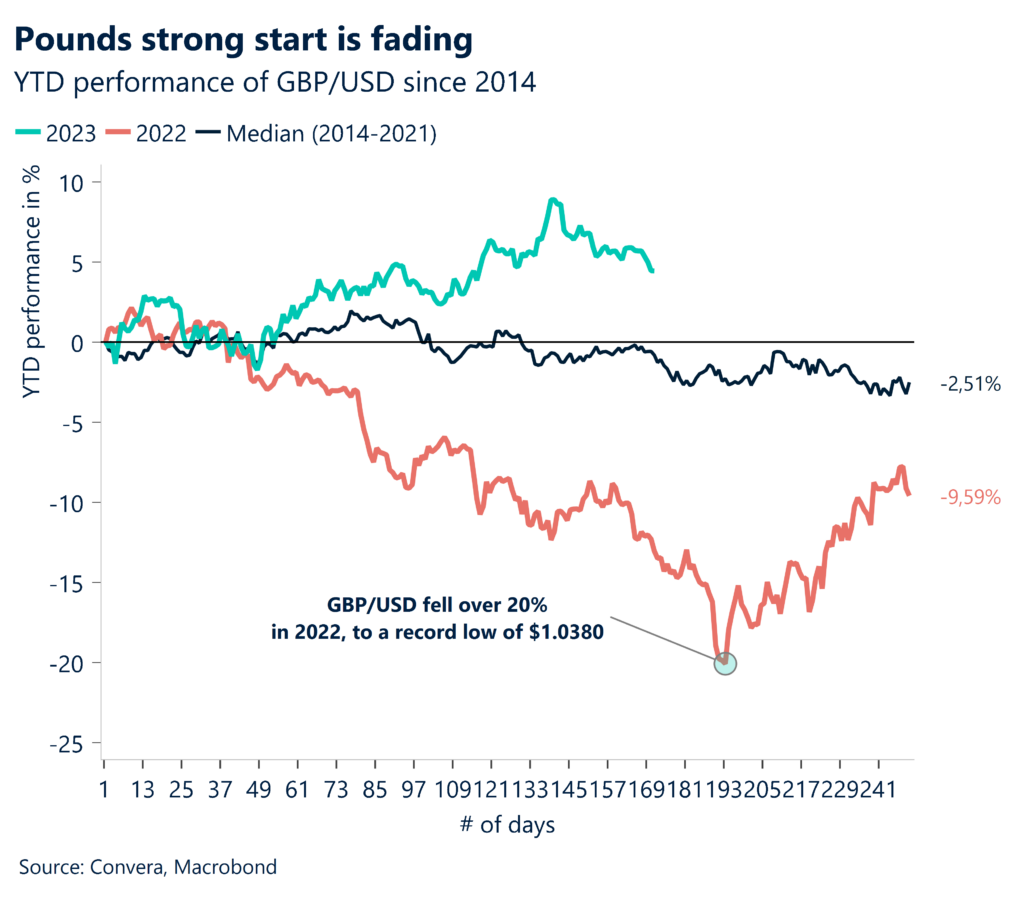

The pound has started the week modestly stronger, after having fallen in five out of the last six weeks against the dollar. Volatility at the end of last week was created by global central bankers trying to sound hawkish at the Jackson Hole Symposium. Bank of England Deputy Governor Ben Broadbent was one of them and emphasized that inflation is unlikely to slow down as fast as it emerged, and that monetary policy will need to remain in restrictive territory for some time.

This might be one reason for the bid the pound is receiving this morning, after having fallen in yesterday’s session by more than 1%. Against the backdrop of a light UK calendar following the public holiday on Monday, GBP/USD and GBP/EUR will be driven mainly by external factors. The data releases in the US and any news on the China front will drive volatility. Chinese authorities took first steps to bring investors back into equity markets, leading to a 5.5% rally in the CSI 300 Index. However, the rally faded quickly, and the stock benchmark closed just 1.2% higher.

Given the pounds procyclical nature, GBP/USD will be highly dependent on the overall risk sentiment and global stock movement. At a level of around $1.2610, the upside trend that had been intact since September 2023, has been broken.

Dollar remains bid

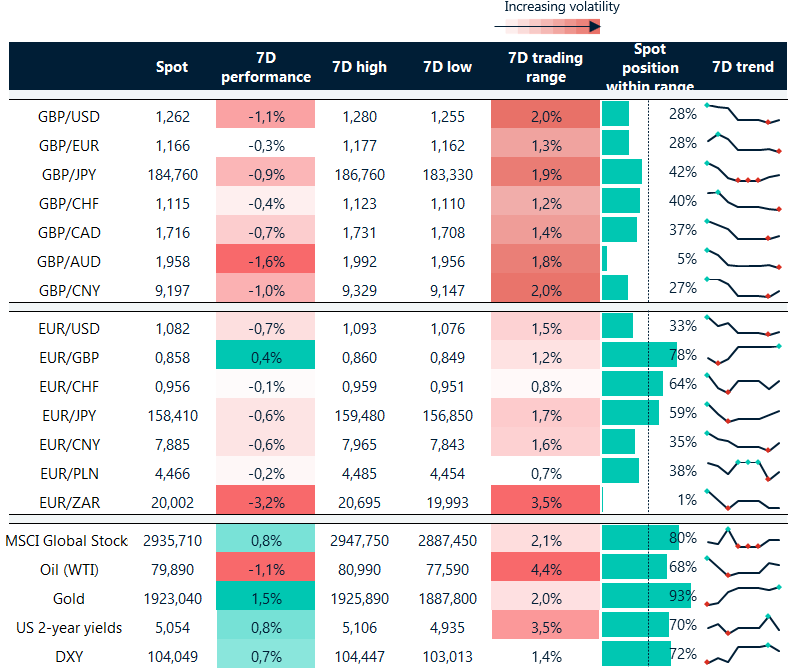

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: August 21-25

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.