Written by Convera’s Market Insights team

Yields and USD sink after PMI

George Vessey – Lead FX Strategist

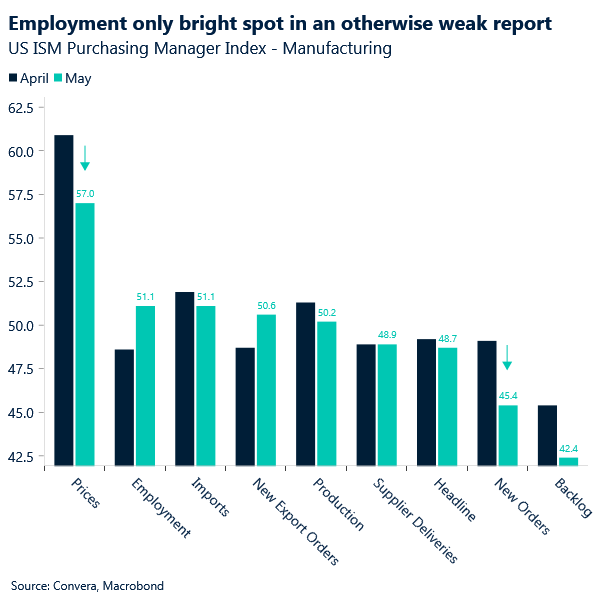

The US dollar is softer against most G10 peers with GBP/USD stretching to fresh 12-week highs above the $1.28 handle whilst EUR/USD has reclaimed the $1.09 handle for the first time since mid-March. Dollar weakness is a result of yields trending lower after the US ISM manufacturing PMI report reaffirmed several prevailing market trends: decelerating inflation, slowing growth and a tight labour market.

Investors are trying to figure out how long the narrative of US exceptionalism can last and are looking at the data for guidance. The make-or-break event for cross-asset developments will be the nonfarm payrolls report on Friday, but yesterday saw the US manufacturing PMI kick off the week for global markets with a downside surprise, which is weighing on the US currency. The headline index declined from 49.2 to 48.7 in May, dragged down by the fall of new orders and backlogs. The price sub-component declined by more than three points, pushing the US 10-year yield below 4.43%. The only bright spot seems to be the increase of the employment category, which had been in contraction for seven consecutive months.

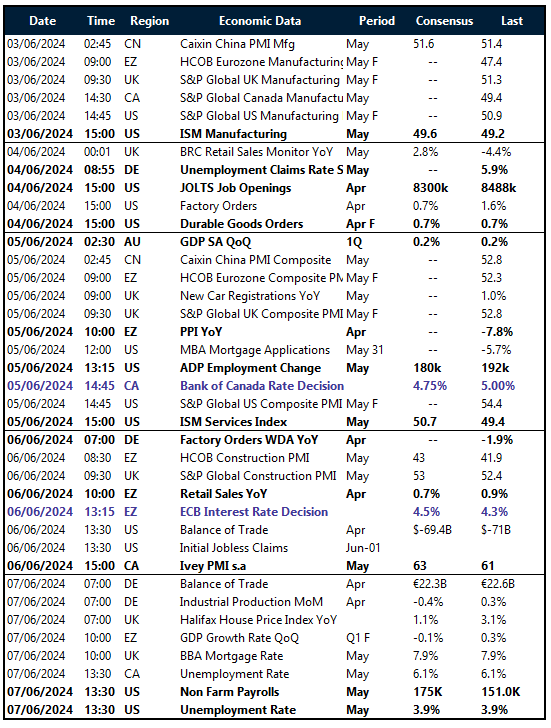

JOLTS job openings will be key today, before services PMI on Wednesday and the eagerly awaited jobs report on Friday.

A trifecta of political risk events to test euro

Boris Kovacevic – Global Macro Strategist

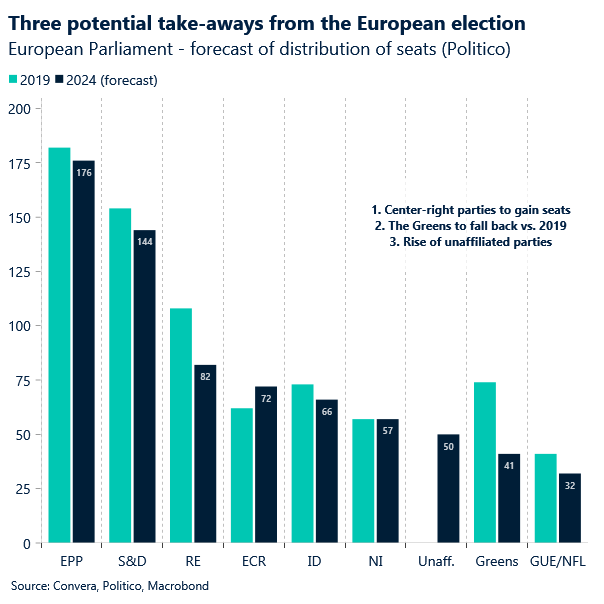

It is a big week for Europe. The continent is facing a trifecta of political risk events that have the ability to impact markets at least on the edges. The European election is coming up at the end of the week, as are the ECB’s interest rate decision and the European Union faces a deadline to inform companies of any potential tariffs on Chinese EV imports as well. The election will be watched in particular given the recent rise of populist parties in countries like the Netherlands, Germany and Austria.

Three shifts are expected to take place. (1) The European conservatives (ECR) are expected to gain the most votes compared to five years ago and to come in as the fifth biggest party. However, because they are not expected to form an alliance with the far right identity group, the soft- and hard anti EU parties will remain fragmented. (2) The Greens are expected to lose about a third of their seats in parliament, which means that the Peoples Party and Social Democrats will most likely remain the two biggest groups. (3) The rise in unaffiliated parties could mean a more fragmented ruling. If all goes as planned, continuity will prevail and volatility should be muted. However, we could see some sectorial impact on Europe’s industries.

The result: Green investments could suffer from the centre-right dominance and defence and chip related companies might benefit from a more conservative ruling.

GBP/USD highest since mid-March

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: June 3-7

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.