PCE didn’t rock the boat, or the dollar

Boris Kovacevic – Global Macro Strategist

Central banks in Japan, Canada and the Eurozone have all left policy rates unchanged last week and have thus rung in the monetary policy year quietly. Next up are the Federal Reserve and the Bank of England on Wednesday and Thursday. While no policy action is expected, investors will parse through the comments and press conferences to gauge the sentiment of policy makers. This week’s most likely non-eventful meetings will be the steppingstones for the upcoming rate decision.

The recent string of stronger than expected macro data and stagnant inflation rates have pushed down the probability of the Fed starting its easing cycle in March from 80 percent two weeks ago to sub 50% as of now. This has led the US dollar to appreciate for four consecutive weeks, gaining around 2.8% from its multi-month low reached at the end of 2023. The Greenback is trading higher against every single G10 currency year-to-date. The S&P 500 has risen in 12 of the last 13 trading weeks and closed Friday just below its all-time high at 4890 points.

The last data release of the week had barely any effect on this market pricing. The PCE inflation remained unchanged at 2.6% from a year ago as the core inflation rate ticked down a bit more than expected, having fallen from 3.2% in November to 2.9% in December. While the disinflationary trend has slowed, it is still well in place. This holds especially true, if we look at the 6-mont annualized PCE rates already in line with the Fed’s inflation target at 2% (headline) and 1.9% (core). Besides the FOMC meeting, investors will focus their attention on macro releases such as Consumer Confidence, JOLTS, the ISM manufacturing PMI, and the non-farm payrolls report. Fed officials will likely remain data dependent and emphasize the need to bring down inflation sustainably on Wednesday.

Will we see a technical recession in Eurozone?

Ruta Prieskienyte – FX Strategist

Last week the European Central Bank (ECB) kept its deposit facility rate at a record of 4% during its first meeting of 2024 and pledged to maintain policy rates at sufficiently restrictive levels for as long as necessary to bring inflation back to its 2% target, despite concerns about a looming recession and a gradual easing in inflationary pressures. At the press conference, President Lagarde said that she stands by her earlier comments that rate cuts could come in the summer. And while we support that time frame, risks are tilted towards earlier cuts.

The ECB Bank Lending Survey confirmed further tightening of credit standards and a decline in loan demand is expected in Q1 2024, while Eurozone’s January flash PMIs were mixed with manufacturing activity topping expectations and momentum in services disappointing. Furthermore, an unexpected worsening in both Ifo and GfK Consumer Indicators for the month of January raised alarms about the health of Germany’s growth. Households’ income expectations have fallen for 23 consecutive months according to the GfK Consumer Indicator, the worst rout recorded since the beginning of the survey in the 1990s. Business expectations continue to point to a very weak Q1 for the German economy.

This week will be filled with key data releases yet again. Tuesday’s Eurozone Q4 flash GDP will be closely watched by investors to gauge whether the bloc plunged into the first technical recession since 2020. Preliminary CPI readings for Germany and EZ due on Wednesday and Thursday respectively will be crucial in assessing whether the ECB is underestimating inflationary pressures, and the reinflation trends is here to stay. Euro starts the week off on a shaky footing, having closed lower against all G10 peers. On Friday, EUR/USD recovered from 6-week lows on the back of better-than-expected US core PCE print, but risks remain skewed to the downside given the key event tomorrow. Meanwhile, EUR/GBP closed at a 5-month low last week as ECB failed to convince the markets. British Pound could strengthen further if BoE stages a hawkish pushback during the rate decision next Thursday.

Risk of a dovish tilt on Thursday

Boris Kovacevic – Global Macro Strategist

Investors are done parsing through last week’s data to justify leaning one way or the other when it comes to the British pound. Policy easing bets have fallen globally. However, investors have pared back their cutting expectations the most for the Bank of England. The BoE is expected to cut by 30-40 basis points less this year than the Fed and ECB. Stronger than expected CPI and PMI numbers have overshadowed the weak consumer confidence and retail sales numbers.

GBP/USD has been trading around the $1.27 anchor for six weeks now, without any hint of a breakout. GBP/EUR has risen above €1.17 for the first time since September and has recorded its fifth weekly appreciation in a row. Weak data from the Eurozone and a slight dovish ECB have supported the pound. The risk is now to the downside as we don’t expect the BoE to live up to these hawkish expectations on Thursday.

Policy makers will most likely hold the benchmark rate steady at 5.25% in line with the consensus forecast. However, the likelihood of a downward revision of the central banks inflation forecast remains a risk to the pound. Both the services and manufacturing PMI’s have expanded last month, pointing to the British economy remaining somewhat stronger than initially expected. Wage growth is coming down steadily but is still high enough to justify holding rates steady through at least the first quarter.

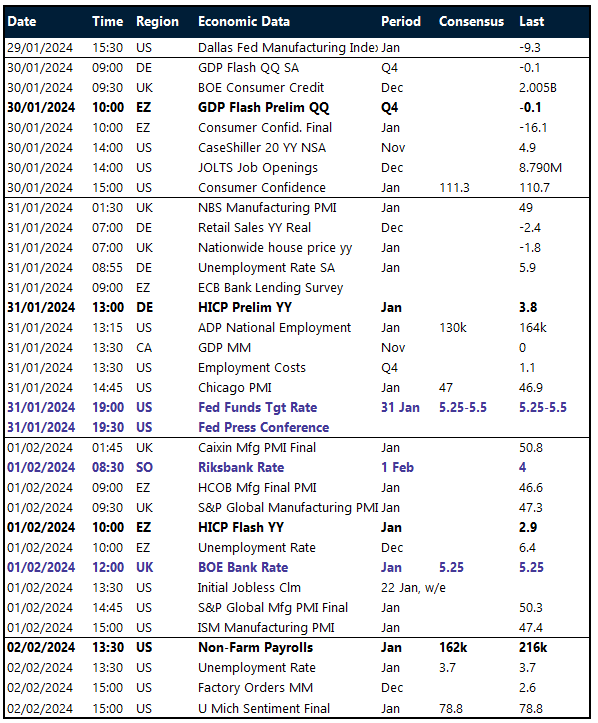

Key global risk events

Calendar: January 29 – February 02

Dovish ECB hurts euro

Table: 7-day currency trends and trading ranges

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.