Written by Convera’s Market Insights team

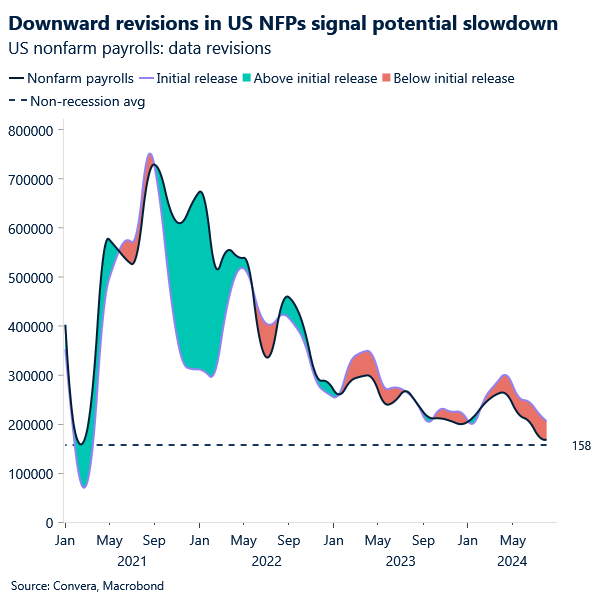

Jobs data revisions in spotlight

George Vessey – Lead FX Strategist

The US dollar index continues to trend south, hovering near its lowest level so far this year, whilst US equities ended their longest daily winning streak of 2024 as traders await a fresh catalyst to drive price action. The Bureau of Labour Statistics releases provisional benchmark revisions to the US employment report today, which could just be that trigger. We’re also keeping a close eye on the Federal Reserve (Fed) minutes from its July meeting.

Improved investor sentiment following last week’s positive economic data, coupled with bets for more than three quarter points of interest-rate cuts from the Fed this year, have boosted bullish flows. Can this positive tone be maintained, or will it be tested today? Traders are bracing for the annual benchmark revision to non-farm payrolls, which is expected to be significantly downgraded. This could prompt traders to price in more rate cuts and bid up bonds, whilst keeping the US dollar under pressure. But if it paints a particularly grim reading of the US labour market, enough to taint risk sentiment, perhaps the dollar might find support from haven demand.

Alternatively, if the revision comes in less than expected, it may result in traders pushing back on aggressive rate cuts as soon as September, hitting risk appetite and again offering the dollar some much-needed support. Either way, we could witness a knee-jerk reaction to the data sparking broader market volatility. Still, we think the any attempt by the dollar to recoup losses could be limited and a downside bias remains more compelling for now.

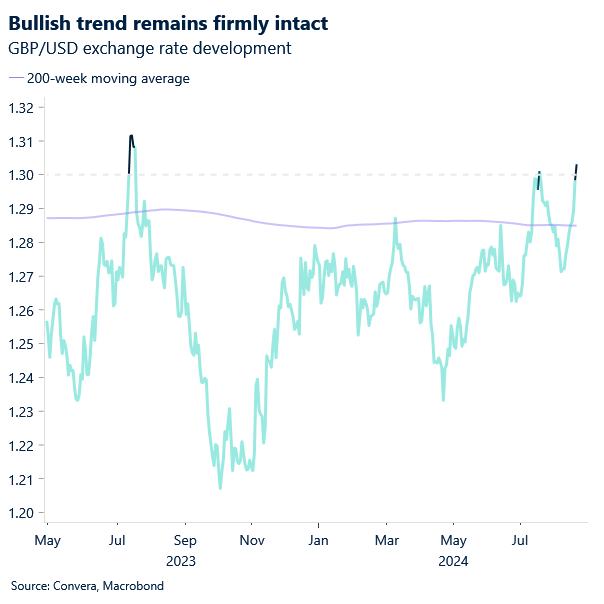

Stablising above $1.30

George Vessey – Lead FX Strategist

The British pound extended to its highest level since July 2023 against the US dollar yesterday, reclaiming its status as the best performing G10 currency in the year to date. GBP/USD has now rallied over 3% from its August low to close the day above the key $1.30 level for just the second time this year.

Sterling continues to benefit from the bearish US dollar backdrop, rate differentials and an improving economic outlook for the UK. Against the euro, the pound’s uplift has been more contained, grappling with the €1.17 handle because of flows into the euro pushing EUR/USD above the $1.11 mark. Data from Adzuna this week revealed British companies stepped up advertising for jobs for the first time this year, a sign of strength in the UK labour market. The jobs-search site also said the number of people looking for work increased, making it the most competitive market for hiring since the country was emerging from Covid-19 lockdowns in May 2021. Official reports and surveys indicate that vacancies in the economy are still decreasing though as the Bank of England closely monitors labour market data for any signs of wage and price increases due to worker shortages, which were prevalent in recent years.

Flash PMI figures released on Thursday will be the next key data points to drive GBP price action as well as speeches by global policymakers delivered during the Jackson Hole Symposium which kicks off tomorrow.

Euro climbs above $1.11

Ruta Prieskienyte – Lead FX Strategist

The Euro strengthened above $1.11, marking a fresh high for 2024, as growing anticipation of a Fed rate cut continues to pressure the dollar. The pair may continue to gain further in the short term if the prospect of cuts to the federal funds rate keeps global equity markets rising and volatility declining ahead of the Jackson Hole conference, despite momentum indicators flashing overbought. Bunds gained while European stocks declined marginally during Tuesday’s session, breaking a streak of six consecutive gains.

Sweden’s Riksbank cut its policy rate for the second time this year to 3.5% and indicated it could cut rates a further two or three times before year-end, which is one more than it had proposed in June. This refreshed forward guidance aligns more closely with current market expectations, which, at the time of writing, had 78 basis points priced into the OIS curve.

Elsewhere, ECB’s Olli Rehn was among the first Governing Council members to acknowledge the shifting balance of risks to the Eurozone outlook. At an event on Monday, the policymaker stated that the recent increase in negative growth risks in the euro area has strengthened the case for a rate cut at the next ECB monetary policy meeting in September—provided that disinflation is indeed on track. Despite Rehn’s dovish comments, the momentum is currently with EUR/USD. The common currency has gained in seven of the last eight trading sessions, and the one-month risk reversal—the price of a EUR/USD call option over an equivalent put option—is the most bullish since March 2022. Positioning in the pair now appears to be around flat, indicating that investors are waiting for the next significant development.

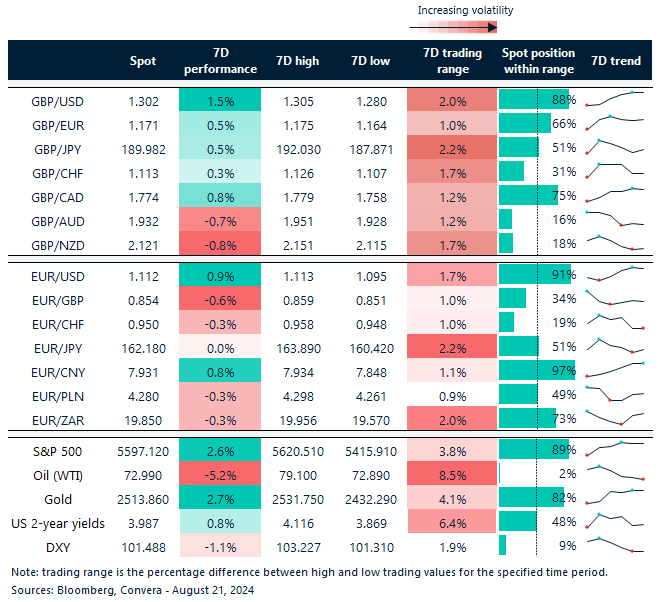

Stocks up almost 3% in a week

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: August 19-23

All times are in BST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.