Written by Convera’s Market Insights team

Sticky US inflation dents rate cut expectations

George Vessey – Lead FX Strategist

Last week saw a bipolar raft of economic indicators from the US which rattled financial markets and added more puzzlement over the Federal Reserve’s (Fed) next policy move. Inflation came in hotter than expected but consumer spending, the economy’s main growth driver, took a step back. After jumping to a 3-month high, the US dollar index recoiled from the 105 level and failed to hold above its 100-week moving average in a sign of upside exhaustion.

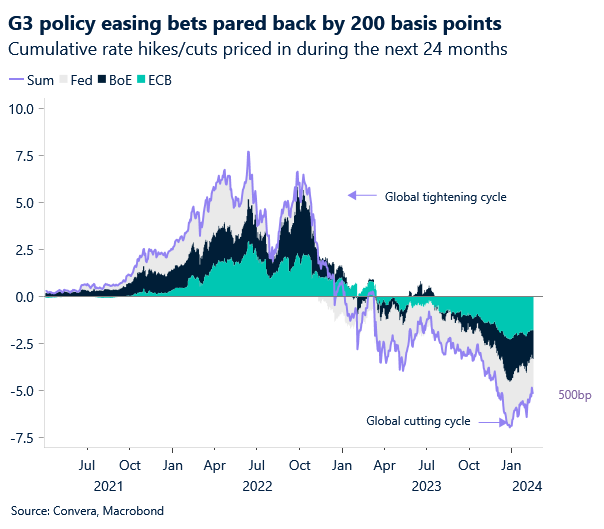

The most nerve-rattling of the data deluge was the consumer price report, which gave the impression that the encouraging disinflation trend has been stopped in its tracks. Goods prices are continuing to deflate, but service inflation, even excluding shelter, remains stubbornly resilient and validates the push back by Fed officials regarding an imminent rate cut. Financial markets have finally accepted that a March rate cut in the US is unlikely to occur. The probability of a Fed rate cut in March has fallen from near 80% at the start of the year to less than 10% today. The weaker reading on consumer spending, though, sent the Atlanta Fed Nowcast of Q1 GDP to 2.9% from 4.2% at the start of the month. Despite the US dollar climbing for a fifth week running against a basket of currencies, the upside potential appears to be waning as an economic slowdown in the US is still on the radar.

Today, US markets are closed for the Presidents’ Day holiday, so trading volumes are likely to be low. Investor focus this week will be on the minutes of the Fed meeting from last month, published on Wednesday, and flash purchasing manager index (PMIs) prints on Thursday.

UK data drives GBP volatility

George Vessey – Lead FX Strategist

The British pound was initially supported by last Tuesday’s unemployment result (at 3.8% in January versus 4.0% forecast) and stronger wage growth (at 5.8% versus 5.6% expected). However, on Wednesday, a weaker inflation result weighed on sterling followed by confirmation on Thursday the UK economy had fallen into a recession. The pound got a lift on Friday though after data showed UK retail sales grew at their fastest pace in nearly three years in January.

Expectations around the Bank of England’s (BoE) monetary policy outlook remains more hawkish than most other major central banks. Overall, the probability of interest rate cuts by the BoE have been scaled back and now less than three 25 basis points of cuts are pencilled in for 2024. This has helped cap GBP weakness, allowing GBP/EUR to reclaim the €1.17 handle despite falling sharply from near 18-month highs and suffering a third weekly decline on the trot. GBP/USD also fell for a third week running but found support at its 50-week moving average and is back above the $1.26 handle to start the week. Fundamental risks still linger due to growth differentials favouring the still-high-yielding dollar but we agree with markets that the BoE will probably keep interest rates higher than the Fed and ECB for longer and this will reward the pound over the long-term due to favouring yield differentials.

The main domestic risk event for GBP traders this week will come on Thursday when flash PMIs for February will be released. In January, both manufacturing and services saw good improvements in the UK and another raft of upbeat readings should further support sterling demand. Apart from the US dollar, the pound remains the best performing currency out of the G10, and we see no obvious reason for this to change any time soon.

Euro supported by green shoots

George Vessey – Lead FX Strategist

The euro continues to trade sideways versus the US dollar, holding above the $1.07 handle – smack in the middle of its 6-month trading range. Although cumulative rate cut bets have fallen to 118 basis points worth of ECB easing by year-end, down from 140 basis points from the beginning of last week, any euro uplift appears capped at $1.08 for now.

However, we think EUR/USD is not too far from a supporting floor as well, because despite a sixth weekly drop in seven and potentially more dollar resilience in the near term, the longer-term outlook of USD weakness should play into the hands of the common currency. We also think markets are still overestimating the size of total ECB easing, therefore expect some hawkish repricing to support European yields and thus the euro too. Against the pound, the euro clocked its best week of the year and its third weekly rise in a row despite falling to a near 18-month low at one point. The economic news from Europe was slightly more positive last week with employment growth accelerating in Q4 to 0.3% q/q and the German ZEW economic sentiment index jumping to its highest level in almost a year.

Flash industry PMIs will again be the focus this week, as traders look for more signs that the Eurozone economy has bottomed. But we also have flash Eurozone consumer confidence on Wednesday and Germany’s most prominent leading indicator – the Ifo index – on Friday, where last month saw sentiment reached its weakest level since May 2020.

Pound and euro flat on the week

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: February 19-23

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.