Written by Convera’s Market Insights team

Euro unfazed by German debt issue

Boris Kovacevic – Global Macro Strategist

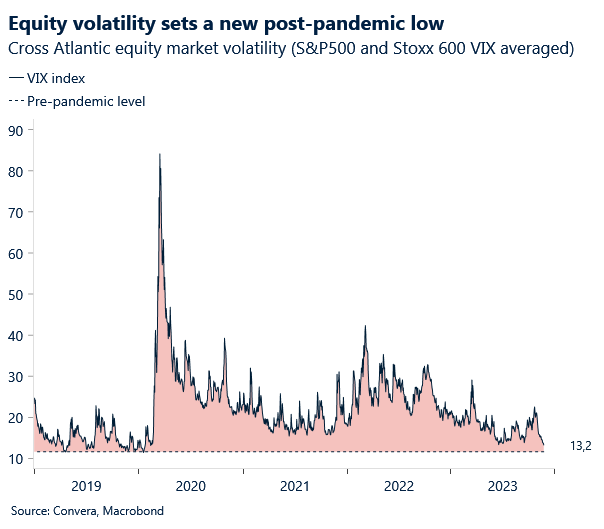

While the United States enjoyed the festivities surrounding Thanksgiving with both bond and equity markets staying closed, investors in Europe were occupied digesting political and economic news headlines. The European Central Bank remains vigilant against sounding too dovish, even as the divergence within the Governing Council grows. And while the purchasing manager indices revealed a slightly slower contraction of business activity in November, the ongoing political uncertainties surrounding the rise of populism on the continent and debt debate in Germany dampened growth optimism. European equities still pushed to 9-week highs as implied stock market volatility fell to a post-pandemic low, while the euro held above the important $1.09 mark.

European policy makers have been attempting to sway markets away from pricing in any rate cuts for 2024 in recent weeks. Especially ECB members like Isael Schnabel and Joachim Nagel have been vocal about the risks of premature easing, with the last mile of bringing inflation down to 2% being the hardest. However, other policy makers have been emphasizing the growing risks to the ECB’s economic outlook. Markets are currently pricing in a 70% of the central bank cutting its policy rate in April 2024 with risks of its inflation projections being revised down in December rising.

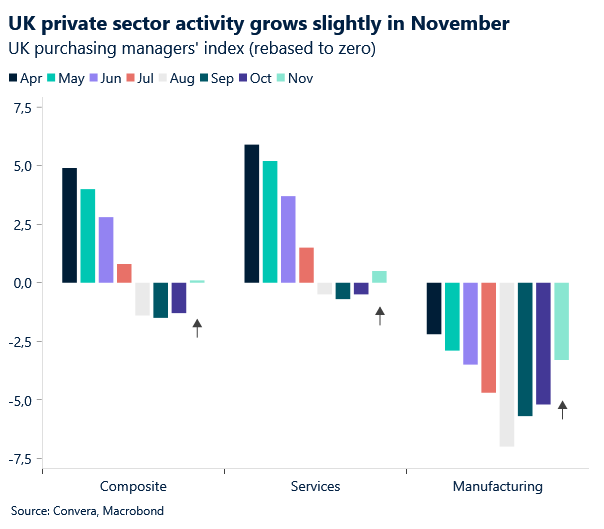

Economic activity remains negative, and we continue to wait on the bottoming of the Eurozone. The composite purchasing manager index for November did improve a bit from 46.5 to 47.1, as the German manufacturing sector contraction slowed for a fourth consecutive month. However, all indicators remain well below the 50 mark, separating contraction from expansion, offering no promises of a quick recovery. The consensus for German GDP growth for 2024 has been cut from 1% at the beginning of the year to now 0.4% as the budget chaos comes into focus.

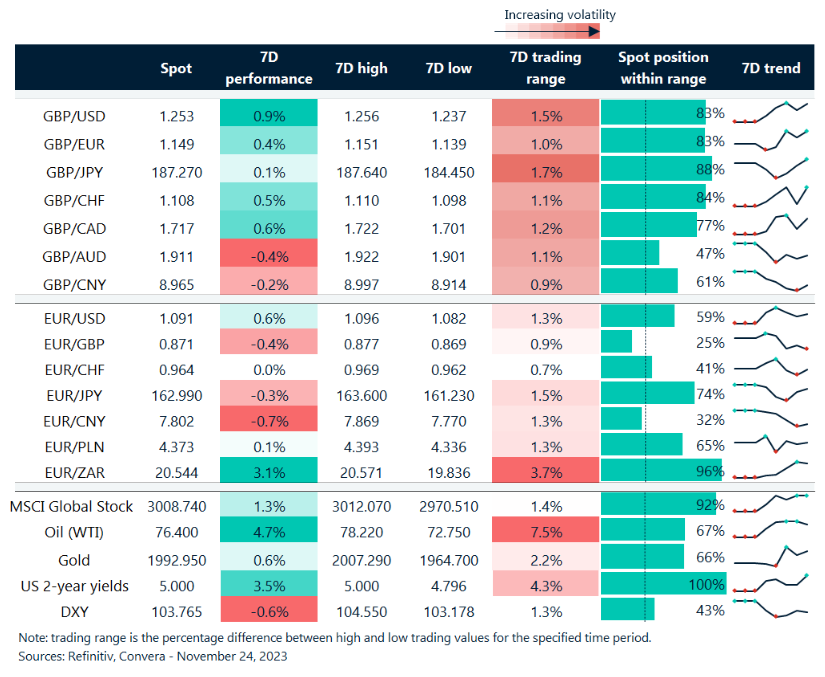

The country’s highest court in Karlsruhe ruled some parts of the government budget as unconstitutional, calling into question hundreds of billions of euros of financing. The Finance Ministry initially froze all new spending for this year as it identifies a solution to the crisis. German Finance Minister Christian Lindner then came out yesterday afternoon and suspended the debt brake for this year, which could help increase borrowing significantly and intends to present a new budget next week. German Bund yields (10Y) pushed higher to 2.62% on the prospects of more debt issuance to come. However, the euro ($1.0950) was unfazed and remained in its upward trend channel that started in October (+4.3%). As the last day of the week begins, investors will pay attention to the Ifo business climate, which is expected to come in slightly higher (87.5 vs. 86.9 previously).

UK returns to growth, contrasting the Eurozone

Boris Kovacevic – Global Macro Strategist

The UK economy likely expanded in the month of November, according to the latest purchasing manager index. The composite barometer returned into expansionary territory at 50.1, after having been negative for three consecutive months. The surprise was echoed by the improvement in consumer confidence, with the GfK’s index rising from -30 to -24. This helped the pound advance higher against both the dollar and euro with the main support coming from short-term GILTS rising for five consecutive days.

The 2-year government bond yield had been dropping ever since it reached a 15-year high at 5.75% back in July. Falling market expectations for the Bank of England and weak macro data had pushed the yield down to a multi-month low around 4.4% last week. Since then, rates have risen by 30 basis points to 4.7%, helping GBP/USD push back above $1.2530. The currency pair continues to trade near a 2-month high and is positioned almost exactly in the middle of its 2- and 3-year trading range. However, while the British currency has broken above all its daily moving averages, GBP/USD has technically entered slightly overbought territory. This can be explained by the pound being driven primarily by improving risk sentiment and rising stock markets as both the swap and expected rate differential between the US and United Kingdom have not moved in recent weeks.

The announcement of the government budget for next year has not had a significant impact on the pound so far. Fiscal policy will continue to dampen the growth outlook for 2024, despite the expected tax cuts. The Autumn statement should not have altered the Bank of England’s last projections for the economy significantly as markets continue to price in a 50% probability of the first monetary policy easing coming in June 2024. GBP/USD is expected to record its third weekly rise in four with the release of US PMI’s being the last obstacle for the pound.

US in festive mood as volatility falls

Boris Kovacevic – Global Macro Strategist

Trading volumes have been thin this week as US liquidity had been missing due to yesterday’s Thanksgiving holiday. However, given that a large number of traders in the US will only return back to the floor on Monday, price swings should be subdued. Cross-Atlantic equity volatility hit another post-pandemic low as a sign that investors have become good at turning a blind eye to recent geopolitical developments. The US dollar pushed slightly lower against the backdrop of somewhat improving European PMI’s. The Greenback (DXY) remains range bound as investors shift their attention to the US PMI numbers published later today. The consensus expects the manufacturing index to fall into recession again, after it briefly jumped into positive territory in October, for the first time in six months. The services sector is expected to have stayed above the important 50 mark for the 10th consecutive month.

Pound at the higher levels of its 7-day range

Table: 7-day currency trends and trading ranges

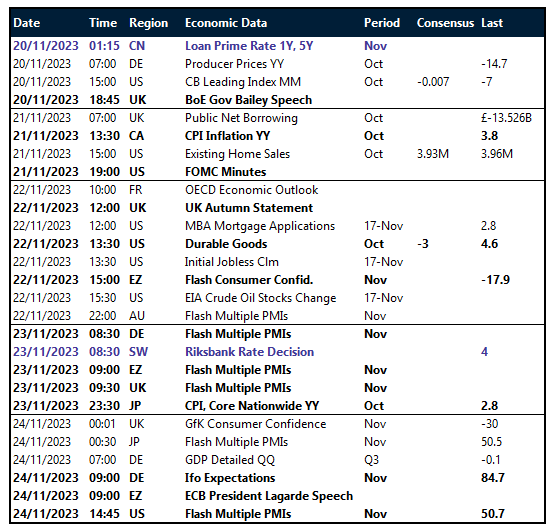

Key global risk events

Calendar: November 20-24

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.