USD: A tight Fed vote coming

As November draws to a close, markets appear to be catching their breath. Equities are finishing the month on a strong note: the S&P 500 posted a 3% gain for the week, its best Thanksgiving performance since 2012, while the Nasdaq Composite surged more than 5%. Even Bitcoin joined the rally, breaking above $90,000. With panic mode subsiding, the U.S. dollar has retreated from recent highs, reinforcing the sense that the past two weeks acted as a classic safety valve. For now, the ‘AI bubble’s fears have subsided.

The second major narrative shaping markets is the shifting outlook for the Federal Reserve. This week delivered mixed macro signals. The Fed’s latest Beige Book pointed to a softening labor market and an uneven, “K-shaped” economy, hardly a backdrop that would compel policymakers to push back against the market’s increasingly dovish expectations.

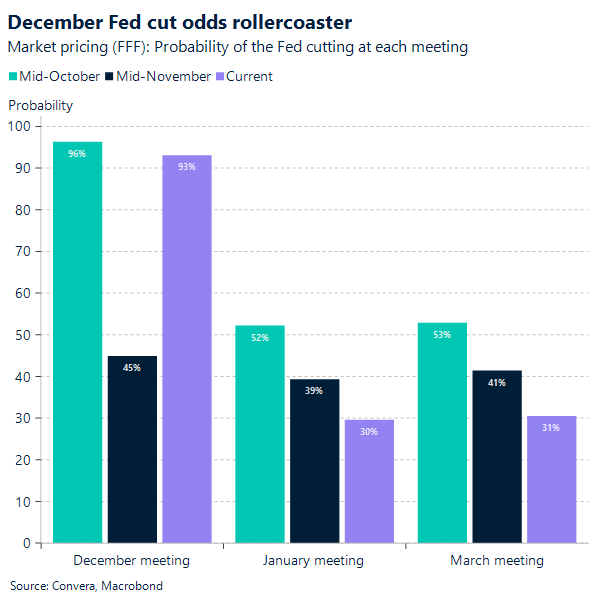

Looking ahead to December, the stage is set for a potentially dramatic meeting. Swaps markets are pricing in a 90% chance of a rate cut, but don’t expect a quiet meeting. A razor-thin vote, perhaps 7-5, could emerge as the committee wrestles with balancing a weakening labor market against stubborn inflation.

The real question: will Chair Powell validate the market’s hunt for a terminal rate below 3%? If he does, the dollar could have room to slide as rate differentials compress, potentially eroding the post-summer resilience of the U.S. dollar index and nudging it toward a more fundamental alignment. However, it’s key to note that while markets repeatedly priced in a rapid Fed policy shift this second half, the U.S. dollar still held up within its 6-month trading range.

Paradoxically, the latest data only adds to the complexity. With the government is fully operational again, and data collection is underway, last week’s jobless claims came in at 216,000, one of the lowest readings this year. In any other cycle, this would be the “desert-island indicator” screaming economic strength. Yet today, it’s largely ignored because it doesn’t fit the prevailing narrative of a deteriorating labor market that justifies rate cuts. Instead, financial media has shifted its spotlight to other stress points, such as affordability concerns, leaving this report to gather dust.

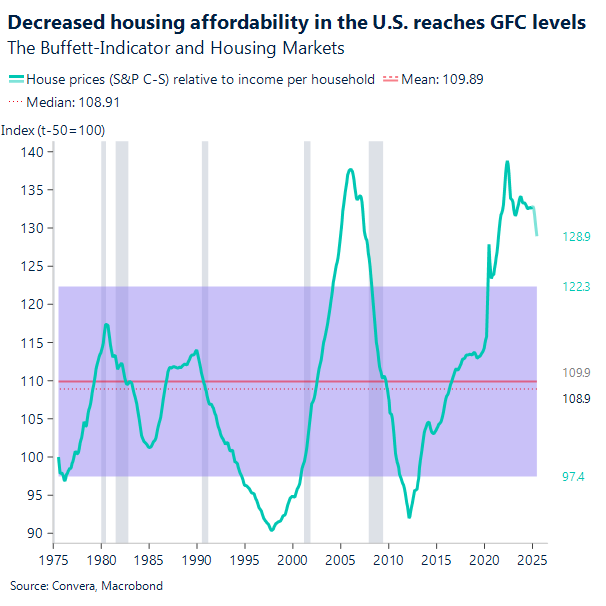

The affordability debate is loudest in housing, where the disconnect is striking. While home prices have eased slightly from record highs in major cities, the Atlanta Fed estimates home median prices have still climbed more than 30% since 2021 to nearly $400,000. To comfortably afford that, a household needs an income north of $120,000, yet the median sits at just $85,000. It paints a picture of an economy that defies easy interpretation: relatively resilient on paper if you look at jobs, punishing on the wallet if you look at homes.

CAD: ‘Drill, Baby, Drill’?

Is this Canada’s “Drill, Baby, Drill” moment? The recent announcement outlines a historic energy agreement between the Alberta and Canadian governments, aiming to transform Canada into a “world energy superpower” by leveraging not just oil and gas, but also renewables and critical minerals. The deal promises to expand export capacity via a new Indigenous co-owned bitumen pipeline, with the potential to add 1.4 million barrels-per-day to the west coast. Yet, this ambitious vision is immediately met with skepticism; critics label the framework “smoke and mirrors,” warning that the requirement for private finance is unfeasible given that the Trans Mountain expansion alone cost $34 billion. This lack of a private proponent has led BC Energy Minister Adrian Dix to state there is currently “no conversation about the feasibility” of the project, while Alberta’s Premier Smith simultaneously faces growing political pressure from opposition leader Naheed Nenshi ahead of the MOU’s aggressive April 1, 2026 deadline for key deliverables.

Crucially, the federal government has agreed to not implement the oil and gas production cap and to immediately suspend the federal Clean Electricity Regulations (CER) in Alberta. Instead, the focus is on reducing emissions intensity through the TIER system and the world’s largest Carbon Capture, Utilization, and Storage (CCUS) project. This regulatory carve-out is set to enable massive investment in AI data centres and strengthened inter-provincial electricity transmission, a package meant to balance economic prosperity with net-zero goals. Furthermore, the MOU attempts to win over key opponents by committing to “appropriate adjustments” to the Oil Tanker Moratorium Act and promising British Columbia “substantial economic and financial benefits” in an explicit effort to secure the necessary trilateral sign-off from B.C. and affected First Nations.

The most damning critique, however, lies in the political and financial cost borne by the federal government. Prime Minister Carney’s move has been met with extraordinary internal dissent, including the resignations of high-profile Liberal loyalists and former ministers, such as Steven Guilbeault. This internal turmoil, coupled with former environment ministers Catherine McKenna and Seamus O’Regan publicly speaking out against the MOU, underscores the immense political risk.

The most contentious aspect, however, lies in the financial reality hidden within the Memorandum of Understanding. As Mark Carney noted, tightening the TIER system to at least $130 per tonne represents a 600% increase in the effective industrial carbon price for Alberta, a cost critics argue is a staggering self-inflicted wound. This raises a fundamental question of competitiveness: among the top five global oil producers, including the U.S., Saudi Arabia, Russia, and China, Canada is the only one tying incremental pipeline capacity to such expensive and anti-competitive carbon capture mandates. With the “Pathways project” and the use of Canadian steel listed as strict prerequisites, many are left asking why Alberta would agree to a deal that arguably handicaps its own industry while competitors operate without such constraints.

CAD: Q3 GDP rises stronger than expected

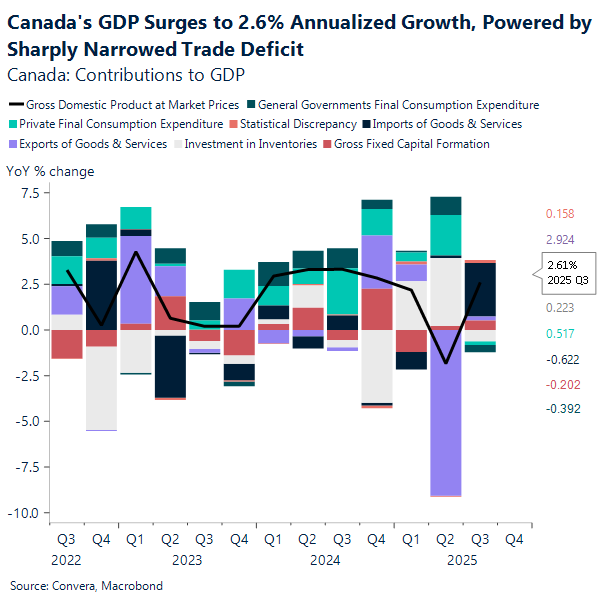

The Canadian economy delivered a stunning performance in the third quarter of 2025, crushing analyst expectations and delivering a powerful signal that the economy successfully dodged recession risk despite ongoing global trade tensions. The market was bracing for an annualized growth rate of just 0.5%, recovering weakly from a contraction of -1.8% in the prior quarter. Instead, the economy surged to 2.6% annualized growth. This massive upside surprise immediately boosted confidence, sending the Canadian Dollar (CAD) strengthening past the key $1.40 resistance level against the USD, a clear indication of reduced near-term economic anxiety.

The headline growth was structurally driven by a strengthening trade balance, as the overall quarterly GDP increase of 0.6% (not annualized) was largely propelled by a significant 2.2% drop in imports, the largest decline since late 2022, while exports modestly increased by 0.2%. This shift, which was aided by higher energy export prices pushing the terms of trade up 1.0%, successfully masked underlying weakness in domestic demand. Crucially, the government provided a strong injection of activity, with capital investment rising 2.9%, dominated by an 82% surge in spending on weapon systems.

Despite the strong headline figures, the report revealed softness in consumer and business capital spending. Household final consumption expenditure fell 0.1%, primarily due to fewer purchases of passenger vehicles, and government consumption also decreased 0.4%. Business capital investment remained flat, as declines in machinery and non-residential buildings offset modest gains. The main positive for housing was not new construction (which fell 0.8%) but a 9.1% increase in residential resale activity, reflected in higher ownership transfer costs. However, the income picture was healthy, with compensation of employees rising 1.1% and corporate income rebounding 2.5%, which helped push the household saving rate up slightly to 4.7%.

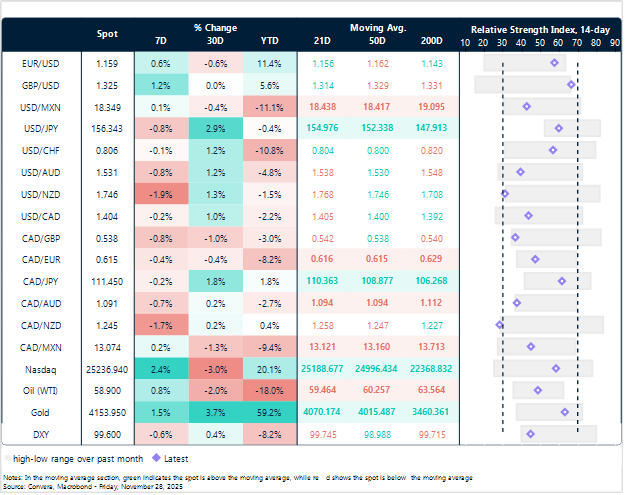

Slight rebound for the US Dollar DXY Index

Table: Currency trends, trading ranges and technical indicators

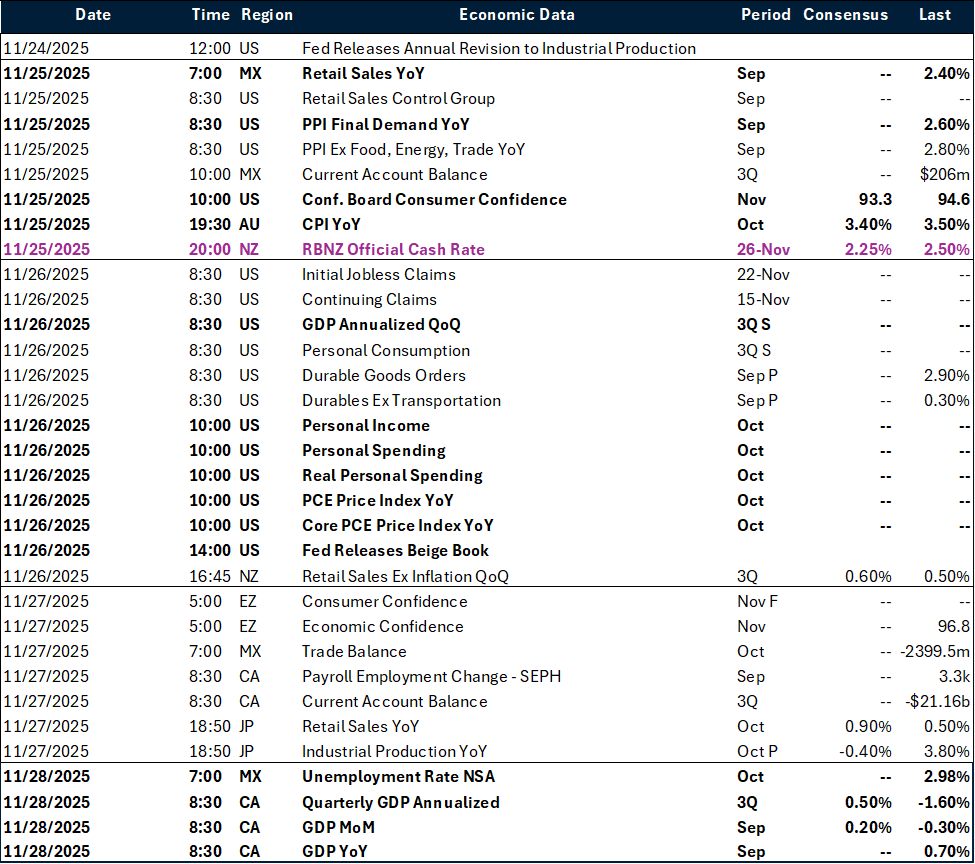

Key global risk events

Calendar: November 24-28

All times are in EST

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.