Written by Convera’s Market Insights team

Dollar supercharged by rate divergence

George Vessey – Lead FX Strategist

A rally in the US dollar is gaining speed, as stubborn inflation sows doubts over how aggressively the Federal Reserve (Fed) will be able to cut rates this year compared to other central banks. Meanwhile, a rise in geopolitical tensions over the weekend firmed up demand for safe haven assets like the USD, but the wider market implications have largely subdued. The US dollar index (DXY), which measures the US currency against a basket of six major currencies, is up 4.6% this year and stands near its highest levels since early November.

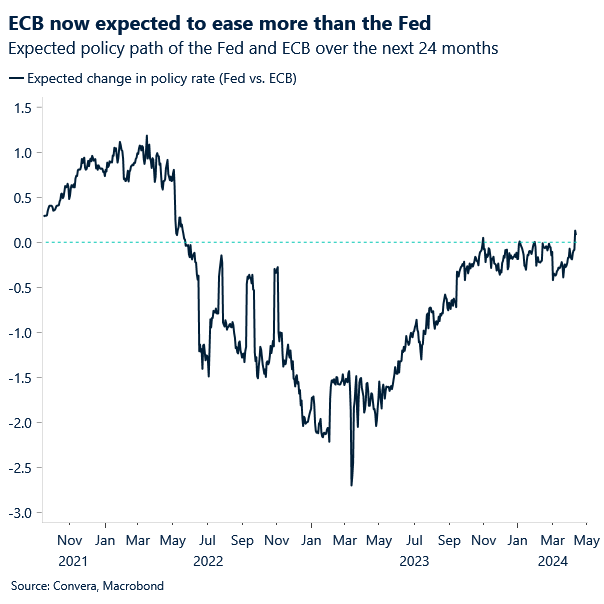

The hotter-than-expected US inflation and jobs report this month have wiped out any hopes of a Fed cut in the first half of the year. At the same time, central banks outside the US have continued laying the foundation for rate cuts at their next meetings. As we know, the Swiss National Bank started the G10 easing cycle and now the Bank of Canada and European Central Bank (ECB) have signaled that cuts are coming, most likely in June. This drives the policy divergence between the Fed and the rest of the world, strengthening the US dollar. We still think the dollar has an asymmetric reaction function to data, meaning weaker US data should spark bigger sell offs in the dollar. But given the ongoing resilience of the US economy, growing fears of US reflation and policy rate divergence widening in favour of the USD, dollar bulls remain in control for now and we cannot rule out further upside in the short-term.

Inflationary pressures are starting to mount again in the form of shipping costs, oil prices and supply chain pressures as well. This is something once again playing into the dollar’s favour. The DXY rose 1.7% last week, its biggest weekly gain since September 2022, with both EUR/USD and GBP/USD pushed lower by rates expectations moving to the dollar’s advantage. Going into this week, we see US macro data continuing to drive price action in the form of retail sales and industrial production.

Pound hits 5-month low

George Vessey – Lead FX Strategist

In the last five weeks, GBP/USD has dropped over 3% from 7-month highs near $1.29. This is mainly a US driven story, with markets now pricing in less Fed rate cuts than the Bank of England in 2024 because of hot US inflation data. The UK-US 2-year yield spread slipped to the lowest in a year and GBP/USD hit a fresh 5-month low near the $1.24 mark. Risk aversion amid rising tensions in the Middle East don’t bode well for the risk sensitive pound either as the downside bias towards $1.23 increases.

The pound slumped by more than 1% against the dollar on CPI day, exhibiting its largest daily trading range on a losing day since last July, reflecting the importance of US data and Fed policy expectations across the FX space. After breaking north of a descending trendline and key moving averages earlier in the week, the pair plunged back below its 200-day moving average, erasing recovery attempts and exposing the risk of a deeper decline towards the 100-week moving average located around $1.23. The pound remains more upbeat against other peers, however, up 1.4% against the euro this year, due to the dovish ECB outlook, but the currency pair lacks volatility and momentum in either direction, caught in a tight 1.2% range for the past three months.

UK labour market and inflation data on Tuesday and Wednesday respectively, as well as retail sales on Friday, will test sterling over the next few trading sessions. Any outcome that pulls forward UK rate-cut expectations could weigh heavy, but we do note that the UK growth outlook is improving, which should support the pound over the longer term.

Risky to bet on a euro rebound

Ruta Prieskienyte – FX Strategist

The common currency starts a fresh week on the back of the worst 3-day selloff in the past 18 months, losing close 2% against the US dollar, thanks to the combination of hot US CPI and a dovish ECB tilt during the rate decision last Thursday. EUR/USD is currently trading at 5-month lows and is 3.7% down on YTD basis – the worst performance since 2022.

Last week, the ECB left its key policy rates unchanged, but expressed intention to decouple from the Fed policy trajectory signalling willingness to cut in June. Policymakers noted that borrowing costs are at levels that are making a substantial contribution to the ongoing disinflation process and said it would be appropriate to reduce the rates if the inflation outlook, the dynamics of underlying inflation and the strength of monetary policy transmission were to further increase its confidence that inflation is converging to the target. The first cut could be a hawkish one as energy price risks are growing once again. In addition, the policymakers are unlikely to succumb to market bets on a rapid-fire easing cycle, nor permit a wide gap to open relative to US rate expectations. Overall, swaps are currently pricing in the chances for a 25 bp rate cut by the ECB at 80% for its June 6 meeting and expect 84bps cumulative rate cuts by year-end.

Given this week’s lack of data from the domestic side, the euro is once again at the mercy of the US developments and will be once again tested when the US retail sales report is released later today. Given dollar’s asymmetric reaction function, EUR/USD will be wounded more so from a downside surprise in the report than it will benefit from an upward surprise. If we see a strong better-than-expected report, EUR/USD could test $1.06 and potentially even $1.05. Albeit any market moving results, we expect the pair to consolidate around the current levels and eventually return towards the $1.07 level given daily RSI is now firmly in an oversold territory. However, given euro weakness, this could take some time to realise.

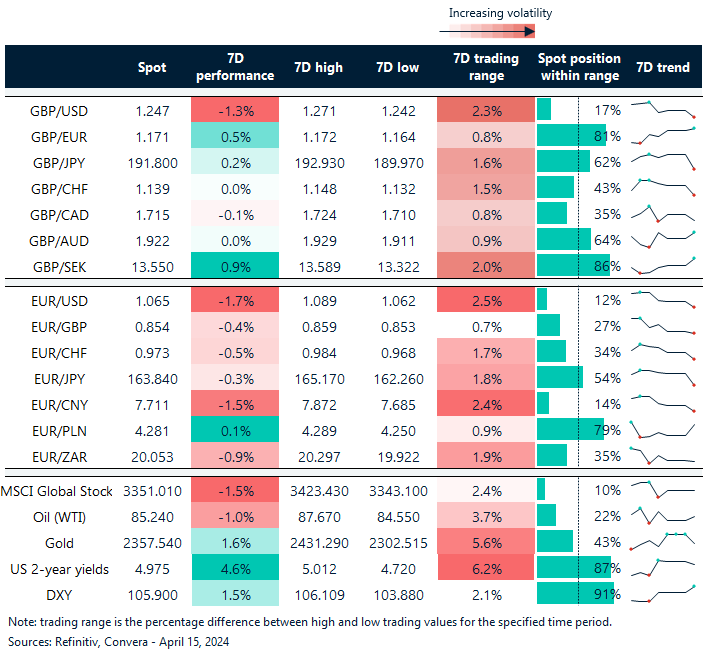

GBP and EUR down over 1% in a week

Table: 7-day currency trends and trading ranges

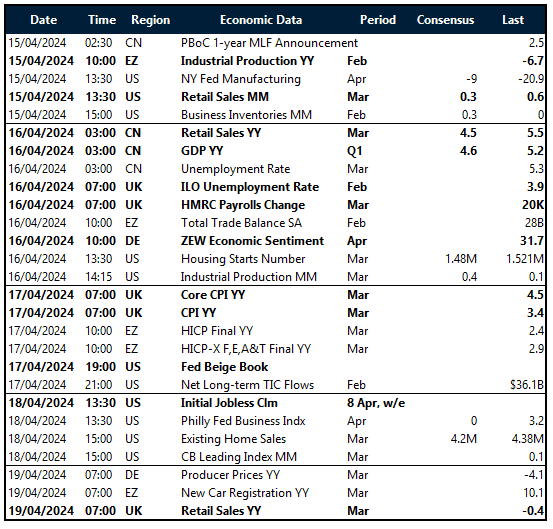

Key global risk events

Calendar: April 15-19

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.