Written by Convera’s Market Insights team

Above-forecast UK inflation boosts pound

George Vessey – Lead FX Strategist

Sterling is climbing across the board after data released this morning showing UK inflation neared the Bank of England’s (BoE) 2% target but failed to slow as much as expected, sending the probability of a June rate cut from 50% to 15%. GBP/USD and GBP/EUR have both clocked fresh 2-month highs at $1.2760 and €1.1740 respectively.

Inflation peaked at 11.1% in October 2022, its highest for 40 years, hence there’s been substantial progress made to tame price pressures as the headline consumer price index dropped to 2.3% y/y in April – its lowest since the summer of 2021 and a big fall from the 3.2% registered in March. However, the fall in inflation didn’t match the consensus forecast of 2.1%, which is also what the BoE had expected. Prices of electricity, gas and other fuels fell by 27.1% y/y – the biggest fall since records began being kept in 1989 and a core reading of prices that excludes volatile food and energy costs fell to 3.9% from 4.2%. Services inflation, which the BoE is watching carefully for signs of domestic pressures, was expected to slow to 5.5%, but remained little changed at 5.9% after a 6% reading the month before. This is important and is the main reason why a June rate cut might be off the table.

UK inflation is narrowing in breadth, with over 40% of the items in the CPI basket now under the 2% target, but there’s still some way to go for the BoE with over 12% of items still rising at a pace of 6-8%. Moreover, because the latest figures were above forecast, particular services inflation, this is a major blow for doves advocating a BoE rate cut in June and this is why the pound has appreciated this morning.

Fed minutes in focus

George Vessey – Lead FX Strategist

The US dollar index continues to hover under the 105 handle as traders digest comments from several Federal Reserve (Fed) officials which point to a longer period of elevated interest rates. The S&P 500 trimmed its monthly rally while the Nasdaq lost about 0.4%, retreating from record levels touched in the previous session.

Yesterday, Fed Governor Waller said further increases in the policy rate are unnecessary, but interest rate cuts are probably several months away – stating several more months of good inflation figures are still needed. This followed hawkish comments from Atlanta Fed President Bostic the day before indicating only one rate cut by the Fed this year is required. Despite lingering expectations for rate cuts, investor confidence has waned a bit, with the likelihood of a September cut now at 60% and November at 73%, below 64% and 77% respectively at the beginning of the week. Market participants will scrutinise the Fed minutes released later today for further insights into the Fed’s monetary strategy.

Meanwhile, cross asset volatility remains compressed. After recording its lowest close since just before the pandemic on Friday, Wall St’s VIX volatility gauge remains comfortably subdued and Treasury market volatility has subsided to seven-week lows. Such a low volatility climate could offer the dollar some reprove due to its high yield appeal amid a popular carry trade strategy.

Near-term euro optimism fades

Ruta Prieskienyte – FX Strategist

The euro remained largely steady around the $1.0850 level, consolidating in a tight range, as investors look for fresh clues about the interest rate outlook on both sides of the Atlantic. European stocks ended the day in red while German bonds climbed for the first day in four, rising with government bonds globally, taking the 10-year yield two basis points lower to 2.51%.

Although largely ignored by the markets, the latest Eurostat report showed that hourly labor costs in the Eurozone increased by 4.9% y/y in Q1 2024, surprising to the upside, and above 3.4% y/y observed in the previous. This raises the risk that Q1 negotiated wage data due on Thursday, a closely watched metric by the ECB, may surprise to the upside. Having said that, such an outcome should have a limited fallout on near-term rates pricing or the euro as the ECB June rate cut is already fully baked in.

Across the G10 spot, EUR/NOK slid as much as 0.6% to 11.5519, its lowest intraday level since March 21, and is testing a key 200-day SMA level. The pair’s volatility has fallen to a four year low as rising European gas prices and its carry appeal lifts the Nordic currency. In fact, the krone is up 4.3% against the Greenback in May making it the best performing G-10 currency. Elsewhere, EUR/CHF remained little changed at 0.9886 after a bout of franc buying interbank flows at the London fix but continues to trade close to its 12-month high. Meanwhile, EUR/CAD rallied to the highest level in close to 6-months as lates report showed Canada’s inflation cooling further in April, laying the foundation for a BoC summer pivot.

With today’s data calendar empty, ECB President Christine Lagarde’s speech and the minutes from the recent FOMC meeting will take center stage. As Fed policymakers continue to emphasise a higher for longer rhetoric and with Lagarde expected to remain non-committal on subsequent ECB moves, momentum going into today’s session is skewed to euro downside given the near-term policy divergence between the ECB and the Fed continues to act as a headwind for the common currency. EUR/USD spot has depreciated close to 0.4% from May high ($1.0894) as the pair continued to pull back from stretched levels. The 14-period EUR/USD RSI has shifted to the lower end of 60 range, suggesting last week’s bullish momentum continues to fade.

CAD slumps as inflation cools more than expected

Ruta Prieskienyte – FX Strategist

The Canadian dollar fell against its G10 peers after domestic inflation print came in lower than expected, bringing forward the Bank of Canada’s rate cut expectations. Loonie shed an average of 0.2% against its advanced peer group on unweighted terms by Tuesday close, with largest losses against the Norwegian krone (-0.51%). Although only conceding -0.24% value on the day, CAD/GBP spot rate slumped to a 36-month low.

The annual inflation rate in Canada eased to 2.7% y/y in April, down from 2.9% y/y in the earlier month, and slightly below market expectations of 2.8% y/y. This marks the softest rate of growth in headline consumer prices since March 2021. Meanwhile, the core rate eased for a fifth straight month to 1.6%, also the lowest since 2021. The main contributors to falling CPI rate were slowing food and restaurants costs. While remaining high, inflation moderated to a softer extent for shelter, underpinned by elevated mortgage costs due to the BoC’s tight policy. Now that all inflation measures are within the BoC tolerance band, the pressure increases on the central bank to kickstart its monetary policy easing cycle from the current 24-year highs.

The broad-based CAD weakness was prompted by the markets moving into fully price in a June rate cut. The swap implied probability of the BoC rate cut in June rose to 57%, up from 43% prior to the CPI release. Despite markets jumping the gun with additional pricing for near-term easing, the risks are skewed for a delayed BoC rate cut. The central bank may wish to opt to wait until its July meeting in order to confirm that lower core inflation will be sustained as it will have two more CPI releases to consider. Country’s labour market remains resilient, and the headline and core readings of inflation are still not at its 2.0% target. If the Bank does delay, the market will unwind recent CAD weakness.

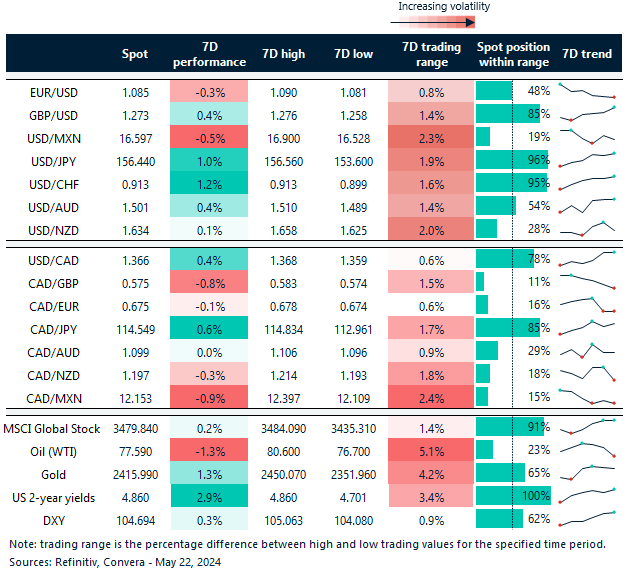

Pound at fresh highs against all peers

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: May 20-24

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.