Written by the Market Insights Team

Dollar higher but key level remains elusive

Boris Kovacevic – Global Macro Strategist

FX markets appear far more sensitive to rising tariff risks than equity investors, who seem complacent about the threats issued by President Trump. While the S&P 500 has been range-bound since mid-November, it remains up 6% since the US election, driven by an initial post-election rally. Meanwhile, European equities have outperformed slightly, rising nearly 8% over the same period.

This resilience in global stock markets is notable, especially given the escalating trade rhetoric and the significant pullback in Fed easing expectations over the past few months. However, key catalysts ahead—Wednesday’s inflation report, Powell’s congressional testimony on Tuesday, and further trade headlines—could provide the momentum needed to break equities out of their recent consolidation. The US dollar strengthened for a third consecutive session, but gains remain limited, with the 3% trading range since mid-December still intact.

As we’ve previously argued, further dollar upside depends on a sustained trade escalation and actual tariff implementation. With the Fed pause fully priced in, the dollar now requires either a stronger US macro backdrop or deteriorating risk sentiment to advance meaningfully. For now, the high noise-to-signal ratio makes shorting the Greenback a difficult case to justify.

Trump’s favorite word

Kevin Ford – FX and Macro Strategist

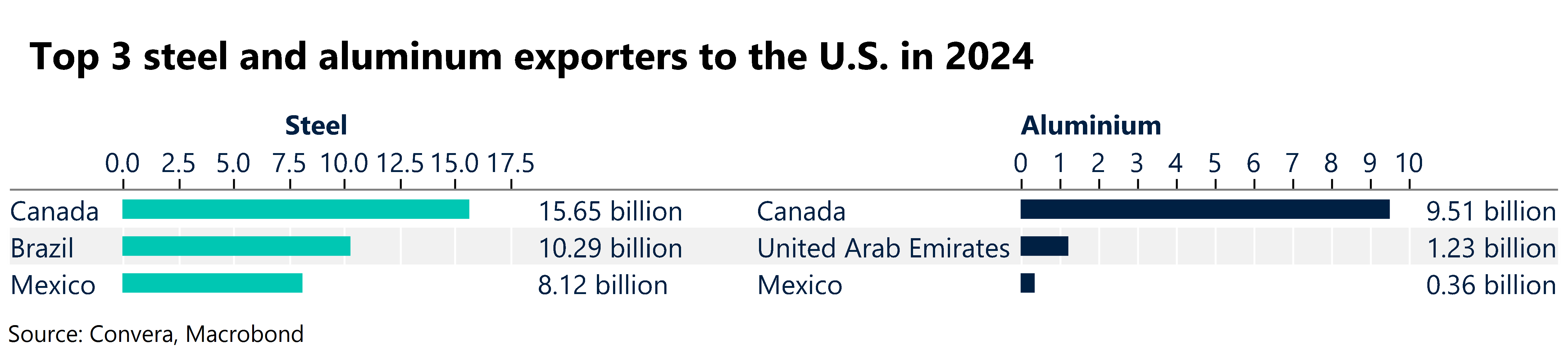

Candidate Trump called ‘tariff’ the most beautiful word in the dictionary back in 2024. This week, President Trump threatened to impose tariffs on all steel and aluminum imports to the U.S. again. Canada, as the biggest trade partner in these sectors, would be most affected. The CAD and Mexican Peso depreciated against the USD. However, the Loonie trades below its 20-day SMA (1.437) and hasn’t shown the same volatility as last week.

The problem with these tariffs is that they target intermediate inputs (goods used in the production process). While they may benefit producers of these inputs and boost employment in protected industries, they often come at a high cost to other sectors, like auto or manufacturing. If the 25% tariffs persist long-term, Ontario and Quebec would be the most affected.

Navigating the current trade uncertainty reminds us of May 2018, when then-President Trump imposed a 25% tariff on Canadian steel and a 10% tariff on aluminum, leading to a 37.8% drop in Canadian steel exports and an 18.6% decline in aluminum exports to the U.S. In retaliation, Canada slapped tariffs on $16.6 billion of U.S. goods, including steel, aluminum, maple syrup, shaving products, ketchup, and coffee. By October, the trade tension spurred negotiations for the Canada-U.S.-Mexico Agreement (CUSMA). By May 2019, both nations agreed to lift the tariffs, leading to the new CUSMA agreement, which took effect in July 2020. However, Trump briefly re-imposed a 10% tariff on Canadian aluminum in August, only to retract it in September before Canada could respond with retaliatory tariffs. Will the next four years be this bumpy? We’re not off to a great start.

In 2019, economists from the Federal Reserve Bank of New York, Princeton University, and Columbia University found that the 2018 U.S. tariff revenue couldn’t cover the losses suffered by import consumers. Despite overwhelming evidence against these trade policies, President Trump remains steadfast in his trade agenda.

Hard time holding above $1.0350

Boris Kovacevic – Global Macro Strategist

EUR/USD extended its losing streak to a third straight session, weighed down by dollar strength and ongoing trade concerns. The downside remained limited as European equities continued their impressive run, with the STOXX 600 closing at a fresh record high, reflecting investor confidence in the region’s economic resilience. Stronger bond yields also provided some support, as markets reassessed the European Central Bank’s policy path amid shifting inflation dynamics.

The latest Sentix investor sentiment index showed a notable improvement in euro zone morale, rising to its highest level since July, suggesting that optimism is slowly creeping back into the region despite lingering economic headwinds. ECB President Christine Lagarde maintained the central bank’s outlook, reiterating that inflation is on track to return to the 2% target this year. However, she cautioned that rising trade tensions, particularly those stemming from the U.S., could pose risks to the outlook, making the ECB’s policy path more uncertain in the months ahead.

Meanwhile, German Chancellor Olaf Scholz issued a stark warning, stating that the European Union is closely monitoring the situation and will not hesitate to retaliate if the US moves forward with tariffs on EU exports. His comments underscored growing concerns that transatlantic trade relations could deteriorate further, injecting another layer of uncertainty into the euro’s outlook. While the currency has managed to hold above key technical levels for now, escalating trade risks and diverging central bank policies could keep EUR/USD under pressure in the near term.

Pound to outperform euro again this year?

George Vessey – Lead FX & Macro Strategist

GBP/EUR is over 1% lower year-to-date but has recently recovered from 5-month lows thanks to a slightly more upbeat UK domestic backdrop but more notably because tariff risks are viewed as more debilitating for the Eurozone economy than the UK. The currency pair is bumping into resistance around its 50-day moving average at €1.20 but is trading north of its 200-day moving average which is trending higher still in a sign of sustained upside momentum.

The currency pair continues to avoid sizeable daily moves. In fact, GBP/EUR has not recorded a daily rise or fall of 1% or more for over 500 trading days. Though lacking volatility, GBP/EUR enjoyed a healthy uptrend in 2024, finishing the year almost 5% higher and recording its highest year-end close since 2016. Two contributing factors of this uptrend have been elevated European political risks and elevated UK-German short-term yield spreads, although both have stabilized lower from their recent peaks. Both macro drivers suggest GBP/EUR should be trading closer to €1.18-€1.19. Thus, we believe sterling is benefiting from its lower beta to tariff risks compared to the euro. If tariff threats against the EU come to fruition, we would not rule out GBP/EUR extending above €1.21 – a level it’s only been above for 1% of the time since Britain voted to leave the EU back in 2016.

On the macro front, the Eurozone economy stagnated at the end of 2024, and recent high-frequency indicators suggest that economic activity is likely to remain subdued in the near term. In the UK, economic activity has also deteriorated, though recent survey data points to moderate revival. Real GDP data from the UK this week should show no economic growth in the fourth quarter of 2024 though. In terms of monetary policy, markets are pricing 66bps of BoE easing by year-end versus the ECB’s 90bps. The two key risks against further GBP/EUR upside more BoE rate cuts being priced in and the tariff narrative softening. The former is already playing out somewhat, with the BoE’s Catherine Mann, who was once deemed as one of the more hawkish voices on the committee, shifting her tone and raising concerns about slowing consumption and the jobs market.

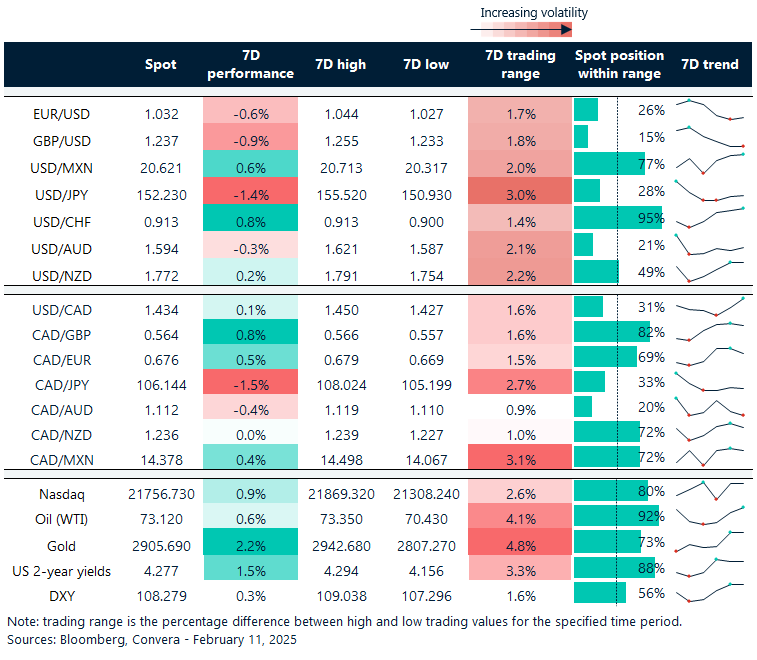

Havens gold and yen in high demand

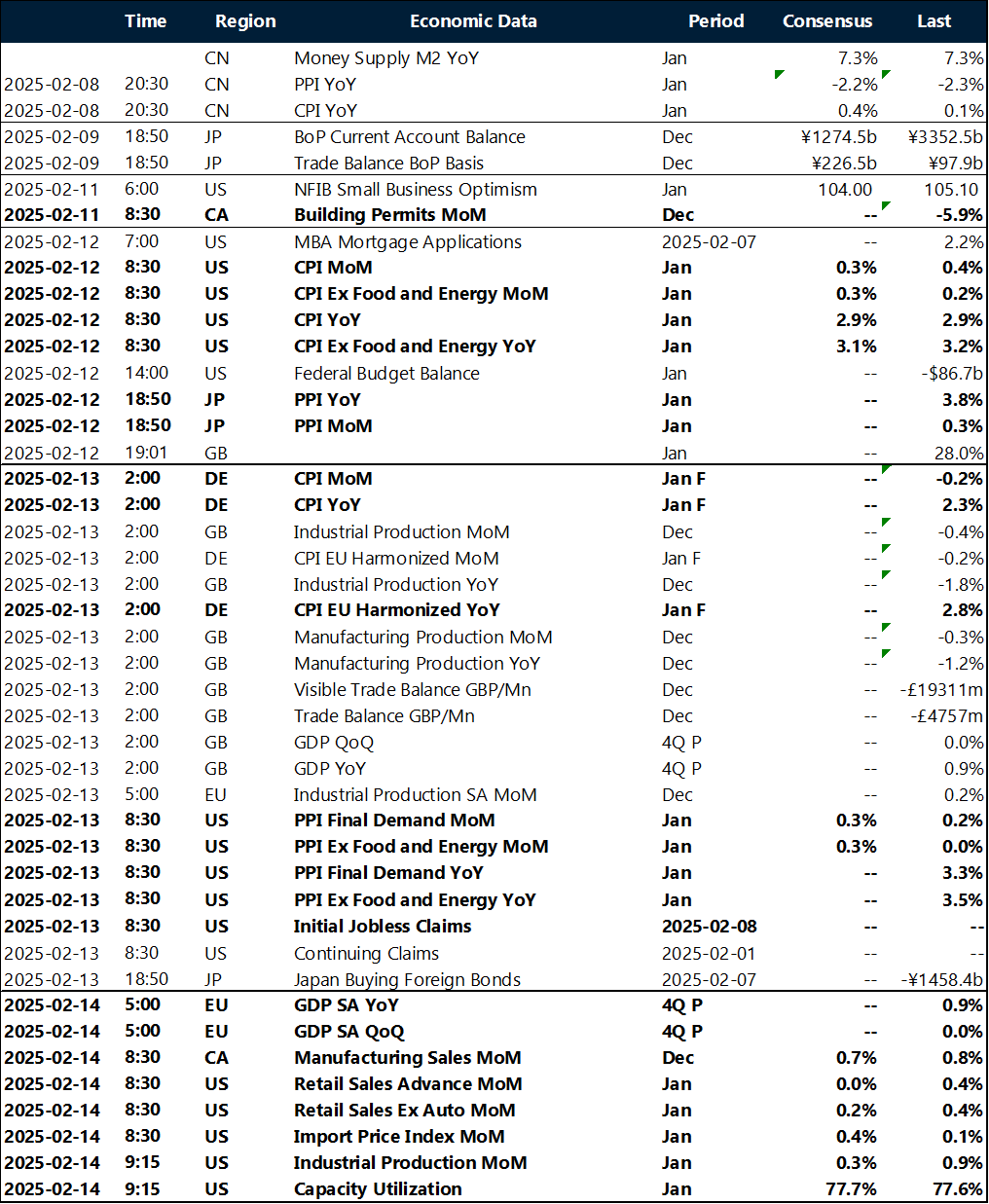

Key global risk events

Calendar: February 10-14