Written by Convera’s Market Insights team

Fed shifts into neutral gear

Boris Kovacevic – Global Macro Strategist

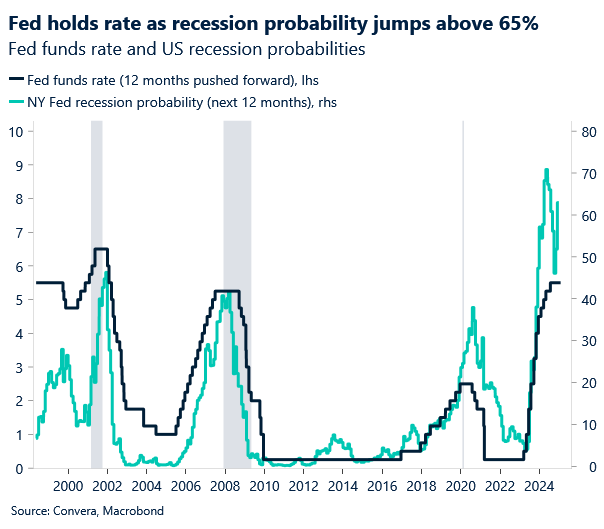

The Federal Reserve held interest rates steady at a 23-year high at 5.25% – 5.50% for the fourth consecutive time, in line with expectations. Policymakers have finally switched into a neutral stance as they removed the reference to further rate hikes from their statement. However, investors were surprised by the pushback from Fed Chair Jerome Powell against a potential rate cut in March, which he regarded as unlikely. Policymakers acknowledged the rise in consumer confidence and the recent string of stronger macro data but continue to expect a moderation of momentum. The inflation picture has improved in recent months but the goal of getting price growth to 2% on a sustainable level is still not achieved.

Investors heard the Fed loud and clear and have reduced the implied probability of the easing cycle starting March from around 50% on Monday to 36% as of now. There is still plenty of time till the next meeting on the 20th of March for markets to move back and forth on pricing. However, both the labour and inflation data will have to disappoint expectations significantly for the FOMC to consider cutting at the end of Q1. The May meeting continues to be our base case with markets pricing in a cut with near certainty 90%. Apart from the ISM manufacturing PMI today and the non-farm payrolls report tomorrow, we will be watching the annual CPI revisions on the 9th of February and the next CPI report on the 13th of February to gauge how likely the Fed is to move in March.

The knee-jerk reaction to the repricing of the Fed’s policy path has been felt across markets with the US dollar appreciating against every G10 currency and finishing the day 0.25% higher on a trade weighted basis. The DXY Index fully recovered its December losses during January, with a gain of around 2.2%. US equities felt the pain as well with the S&P 500 falling by 1.5% and recording its worst day since mid-December.

BoE to drop tightening bias?

George Vessey – Lead FX Strategist

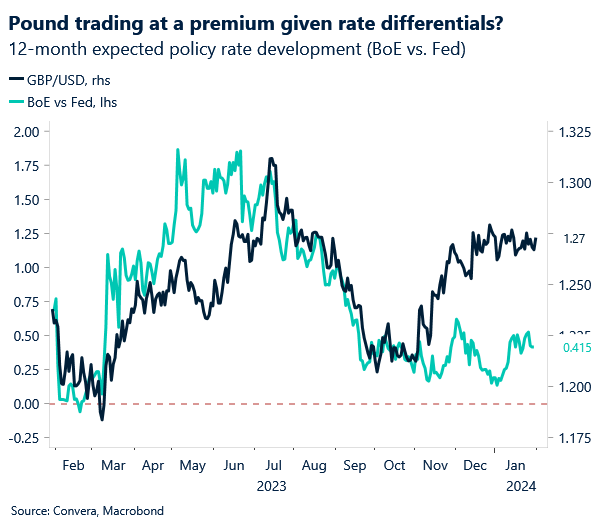

The Bank of England (BoE) has been more reserved than other central banks to endorse interest rate cuts and whilst rates are expected to remain unchanged at 5.25% today, we expect the BoE to soften its ‘bias to hike’ rhetoric. Despite the surprise uptick in inflation this month, services inflation and private-sector wage growth are tracking well below the November BoE projections. Therefore, there is a growing chance of more dovish nuances, which could weaken sterling.

Most members of the committee will probably want more reassurance on wage and price pressures before supporting rate cuts though. If any policymakers were to vote for a cut, this could jolt markets, increase rate cutting expectations and pressure the pound lower. Sterling currently remains the best-performing G10 currency against the US dollar this year, but its negative January performance ended a 2-month winning streak. Moreover, GBP/USD has lacked directional conviction for seven weeks running, caught in a narrow 1.4% range. Long-term daily and weekly moving averages are trending flat and the Relative Strength Index, on both daily and weekly charts, is in neutral territory. To summarise, technicals aren’t offering many directional clues. Plus, implied volatilities in GBP/USD are low, indicating large swings in the currency pair aren’t expected, even amid the key risk events of this week.

Overall, the market reaction could be muted today, and we don’t anticipate a breakout of the $1.26-$1.28 range. However, central bank meetings can catch investors off guard and disrupt market inertia. So, although we expect no change in policy by the BoE, any surprises in the vote split, statement or economic projections could inject some volatility into sterling.

Euro slips to an 8-week low

Ruta Prieskienyte – FX Strategist

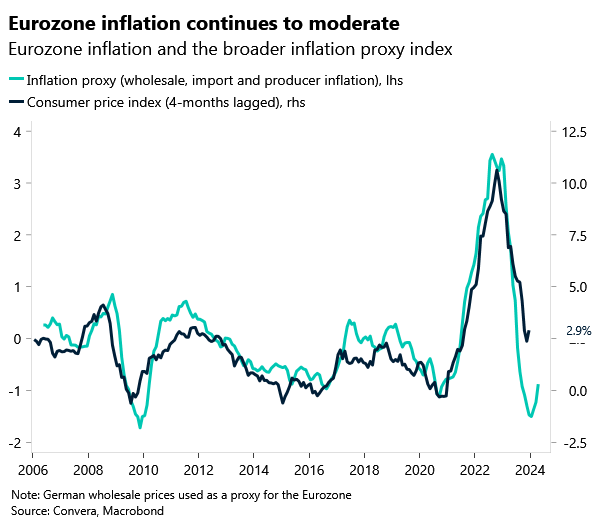

The euro had its worst January performance against the US dollar since 2015, falling by over 2%. After the Fed’s decision yesterday and better-than-expected domestic preliminary CPI data figures, EUR/USD slipped to an intraday low of $1.0793and has this morning clocked fresh 6-week lows. Meanwhile, the German 10-year Bund yield declined to the lowest point since 12th January, to 2.16%, as markets increased their bets on the possibility of earlier interest rate cuts by the ECB.

The euro had rallied earlier in the session as inflation in Europe’s largest economy cooled unexpectedly. Preliminary estimates showed that German consumer price inflation dropped to 2.9% y/y in January 2024, down from 3.7% the previous month – the lowest rate since June 2021, driven by a slowdown in energy and food inflation, despite a pickup in services. The HICP index slowed to 3.1% y/y from December’s 3.8%. While the drop in German inflation will fuel speculations about an early ECB rate cut, underneath a favourable headline inflation there are still enough price pressures to worry about. Looking under the hood, the drop in headline inflation is mainly the result of favourable energy base effects as core inflation remained almost stable (3.4% Jan vs 3.5% Dec). In addition, the favourable base effects mask a trend of monthly price increases. In fact, the monthly increase in consumer prices was actually higher than previously in the month of January; the prices for goods and food particularly accelerated. Earlier in the week, ECB policymaker Joachim Nagel, typically perceived as a hawk, mentioned that the central bank had successfully tamed the “greedy beast” of inflation, while his colleagues, de Guindos, Centeno, and Kazimir, suggested that the ECB’s next move would involve an interest rate cut.

Looking ahead, risks to the EUR/USD are skewed to the downside as markets will continue to digest the Fed’s decision. The common currency could weaken further on the back of flash Eurozone inflation later this morning if the reading were to come in below expectations. Markets continue to price close to an 80% probability of an ECB rate cut in April and around 143 basis points of cumulative rate cuts by the end of 2024.

USD and Gold are top performers

Table: 7-day currency trends and trading ranges

Key global risk events

Calendar: January 29 – February 02

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.