Written by Convera’s Market Insights team

Markets muted with key data eyed

Boris Kovacevic – Global Macro Strategist

Equities have struggled to gain traction over recent sessions whilst the US dollar is consolidating against major peers after hitting an almost 2-month low last week. Investors await a slew of US economic data releases today ahead of the Federal Reserve’s (Fed) monetary policy meeting next week, which could induce a bit more volatility into the relatively sedate financial markets.

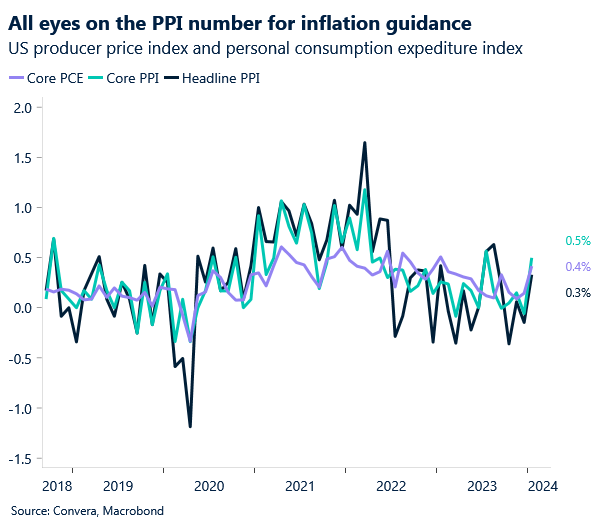

Today’s macro calendar is looking to compensate for the lack of economic releases in yesterday’s trading session with retail sales, producer price inflation and initial jobless claims coming up. US Treasury yields have risen for three consecutive days going into the releases as inflation data continues its streak of above consensus prints. The higher-than-expected CPI number from Tuesday is putting the spotlight on the producer price index, which is seen as a reasonably strong leading indicator for the Fed’s preferred inflation gauge (PCE). The PPI is expected to repeat its 0.3% monthly gain from January as retail sales are expected to post a positive print of 0.8% in February. With jobless claims expected to continue remaining suppressed at around 218 thousand, the consensus sees the macro news flow as dollar positive. However, given the positive bias, downside surprises would hurt the Greenback, especially given that today’s releases feature all three data categories the Fed and markets are currently following to gauge where the economy is headed: inflation, the labour market and consumer spending.

Recent data has so far driven marginal changes in rate expectations and although the Fed will hold rates unchanged next week, all eyes will be on the bank’s updated economic projections, which could prove more market moving.

Pound steady as traders digest UK data

George Vessey – Lead FX Strategist

Although the British pound jumped north of a tight 3-month trading against the US dollar last week, upside traction has faltered, and volatility remains subdued. Despite the pause in gains and pullback from 7-month highs though, GBP/USD remains in its longest stretch since 2014 without a decline of at least 1% on a weekly basis. Can we infer from this that the pound is looking more vulnerable to a negative surprise? Or will momentum continue to lean higher?

After falling into a technical recession in the second half of last year, the UK economy rebounded in January, registering modest GDP growth of 0.2%, whilst the rolling 3-month GDP only shows a very small contraction. Momentum is likely to remain weak in the near-term, but the economy seems to be showing enough signs of improvement, which is persuading investors that the Bank of England may have to keep interest rates higher for longer than its peers. Markets are now pricing in slightly less than three rate cuts in the UK by year-end, with a June cut around 50% priced in and an August cut fully expected. One risk for the pound is if the probability of a June rate cut increases and an additional (4th) rate cut for 2024 is priced in by markets if data supports such a path. An example of such data came earlier this week when UK labour figures showed British wages excluding bonuses grew at their slowest pace since October 2022, while the unemployment rate edged up unexpectedly, easing inflation worries. Nevertheless, wage growth remains well above the rates consistent with 2% inflation., whilst survey data has hinted at a recovery in the economy, with private-sector growth at a nine-month high in February.

Will UK interest rate expectations and the pound remain elevated? After the US data dump today, focus shifts to UK inflation data and the Fed and BoE meetings next week for more clues on prices and economic expectations.

Euro keeps a bullish bias

Ruta Prieskienyte – FX Strategist

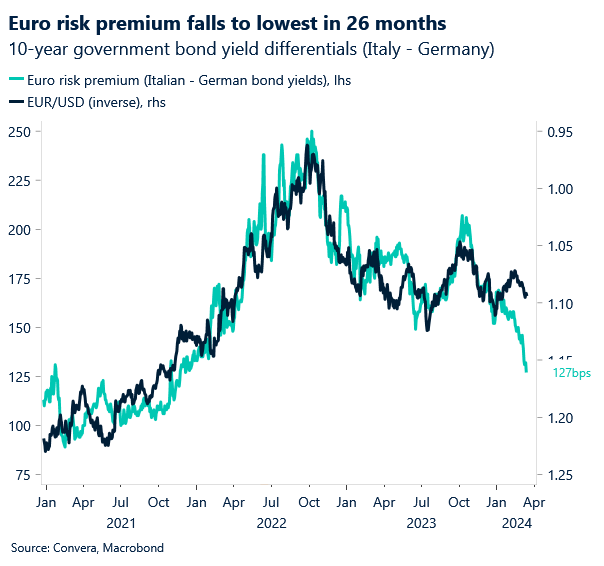

The euro advanced against its G10 peers as hotter-than-expected US inflation data failed to hurt expectations of Fed interest rate cuts in the coming months. European stocks climbed to fresh record highs while the gap between Italian and German yields, a gauge of risk premium investors ask to hold bonds of the euro area’s most indebted countries, hit a 26-month low. Appealing returns and appetite for riskier assets boosted demand for Italian government bonds, in support for EUR/USD.

Although largely ignored by the markets, the latest Eurozone industrial production print plunged by 6.7% y/y in January – the sharpest contraction in activity in 10 months, and the second largest decline since the aftermath of the COVID-19 outbreak, primarily driven by a 14.5% drop in the production of capital goods. This means that Q1 GDP is under pressure again as the Eurozone economy continues to broadly stagnate. In other developments, yesterday the ECB unveiled the outcome of its long-awaited Operational Framework Review that sets rules for how it provides liquidity to commercial banks in the coming years. Under the new framework, the ECB will give banks more incentive to lend to each other, while providing safety nets to limit the risk that lenders could run out of cash, including tweaking one of its key interest rates in September. Overall, the outcomes of the review formalised many of the current tools and were in line with market expectations.

In terms of data, investors are turning their attention to US retail sales and PPI reports due later today. EUR/USD overnight ATM options not pricing in an increase in volatility, thus we are not expecting a significant course correction to EUR/USD trajectory. Otherwise, the Eurozone calendar includes speeches by two hawkish ECB members, Elderson and Knot, who will likely continue to emphasize caution against premature ECB rate cuts.

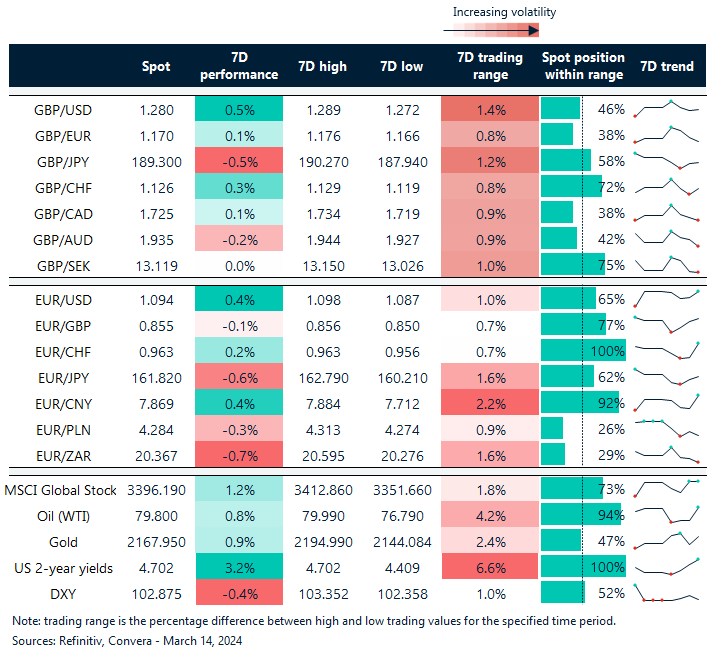

Dollar still licking wounds from last week’s losses

Table: 7-day currency trends and trading ranges

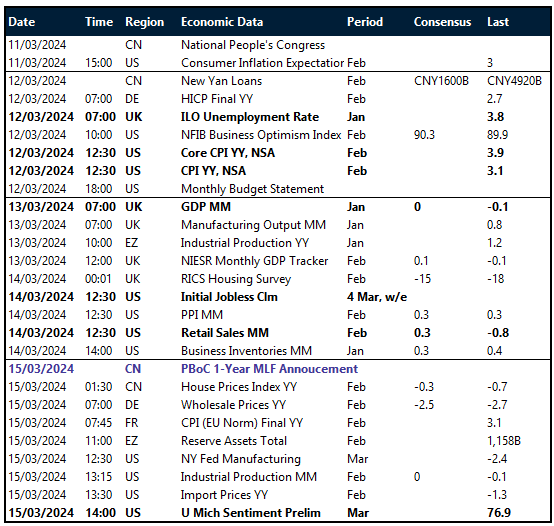

Key global risk events

Calendar: March 11-15

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.

Join us for Convera Live! A series of in-person events discussing the future of global payments.