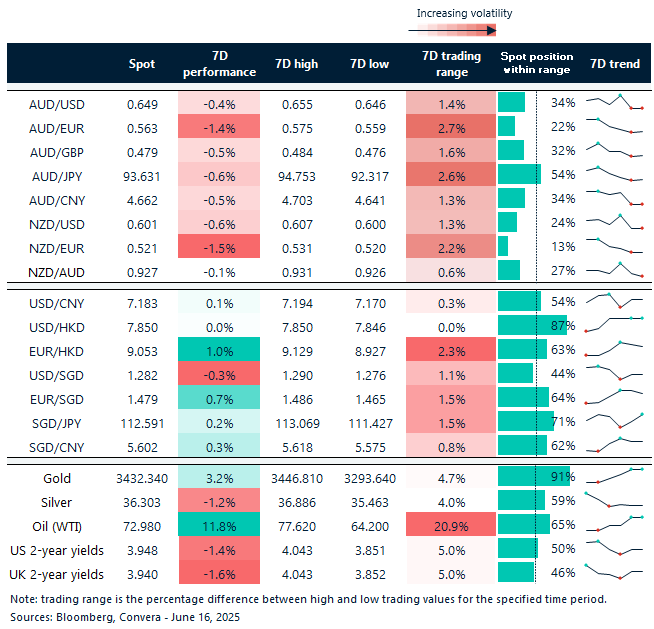

Aussie, kiwi fall from recent highs

Global markets were on edge Monday morning as hostilities in the Middle East escalated. An Israeli strike on Iran on Friday was followed by a series of counter-strikes between the two nations over the weekend.

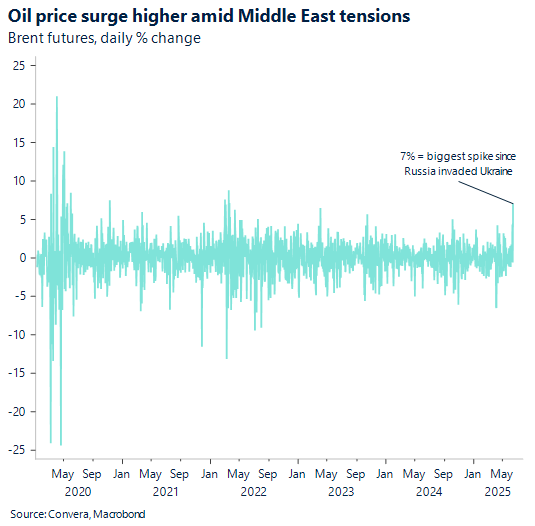

Global share markets fell, while oil prices saw their largest one-day surge since the Russian invasion of Ukraine.

In FX markets, the New Zealand dollar was hit hardest due to its sensitivity to overall risk sentiment. NZD/USD dropped 0.9% from eight-month highs.

AUD/USD lost 0.7%, retreating from seven-month highs.

In Asia, USD/SGD rebounded from 11-year lows, climbing 0.3%. USD/CNH also rose 0.3%.

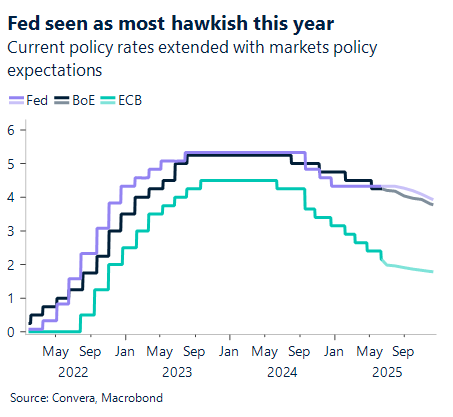

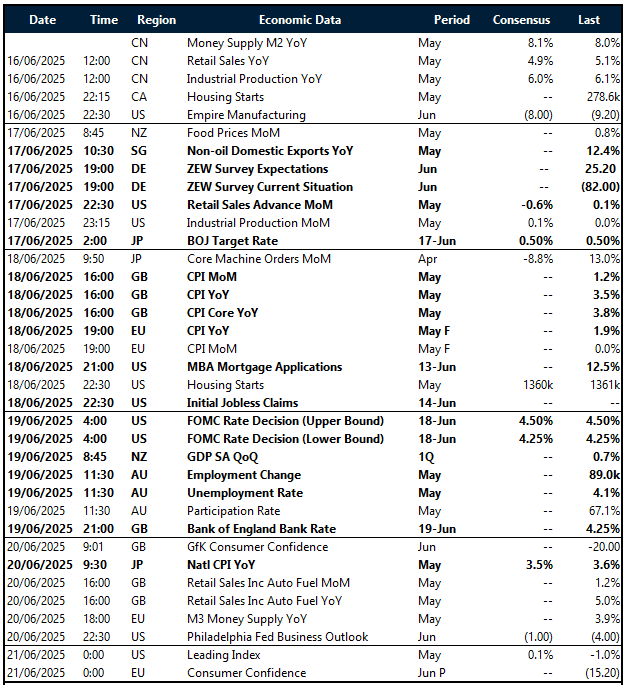

Central bank decisions take centre stage this week

The upcoming week will be pivotal for monetary policy watchers, with the Federal Open Market Committee (FOMC) meeting on Thursday. Markets expect no change to the current interest rate, with the upper bound forecast to remain at 4.5%.

Meanwhile, the Bank of England (BoE) will also announce its rate decision on Thursday, with expectations leaning toward a hold at 4.25%. These announcements will play a key role in shaping sentiment for both the US dollar and the British pound.

Additionally, the Bank of Japan (BoJ) is expected to maintain its target rate at 0.5% on Tuesday, continuing its accommodative stance.

The week is packed with high-impact data releases offering insight into global economic health.

The Empire Manufacturing Index kicks off the week on Monday, with a consensus estimate of -8.0 (up from -9.2 previously).

On Tuesday, Retail Sales Advance MoM (expected at -0.6%) and Industrial Production MoM (forecast at +0.1%) will be closely scrutinised.

Wednesday brings the UK’s May CPI report, followed by Retail Sales figures for May on Friday.

Final Eurozone CPI figures for May are due Wednesday, and preliminary June Consumer Confidence data will be released on Saturday with markets watching for improvement from the previous -15.2 reading.

In the Asia-Pacific region, key updates on employment and GDP are expected.

New Zealand’s Q1 GDP figures are due Thursday, while Australia’s May employment data, including the employment change (prior: +89K) and unemployment rate (prior: 4.1%), will be released the same day.

Kiwi slips as New Zealand manufacturing PMI declines

Turning to local developments, after four consecutive months of growth, New Zealand’s BusinessNZ Manufacturing PMI fell to 47.5 in May from 53.3 in April, signaling a return to contraction.

Weak business confidence, rising costs, and sluggish demand have stalled the sector’s recovery.

The data suggests manufacturing momentum may have faded after a promising start to the year.

Keep in mind, PMI readings above 50 indicate expansion, while figures below 50 signal contraction.

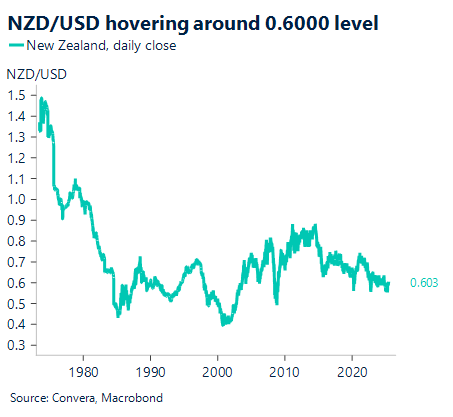

NZD/USD has retreated following last week’s risk-off move but remains roughly 10% above its September 2024 low of 0.5486.

Key support levels are at the 21-day EMA of 0.5996 and the 50-day EMA of 0.5933.

Greenback surges after Middle East strikes

Table: seven-day rolling currency trends and trading ranges

Key global risk events

Calendar: 16 – 21 May

Have a question? [email protected]

*The FX rates published are provided by Convera’s Market Insights team for research purposes only. The rates have a unique source and may not align to any live exchange rates quoted on other sites. They are not an indication of actual buy/sell rates, or a financial offer.